By Chris Benedict, Director, DataLend. Lower oil prices due to a glut of supply and a strong dollar are an early Christmas gift to consumers but a big lump of coal to shareholders of many energy companies. Oil has dropped by a whopping 35% from its June highs of $102 per barrel, and the stock prices of many energy companies have followed suit. The worst hit were the shale oil firms, offshore drillers and oil companies with high debt-to-equity ratios. As the longs sold, the shorts pounced on the opportunity and the share prices of some companies dropped to five-year lows. Unsurprisingly, utilization and fees to borrow have spiked in these names as their share prices tanked. In this article we’ll take a look at some companies that have been the worst hit and are among the most actively traded in the securities finance market.

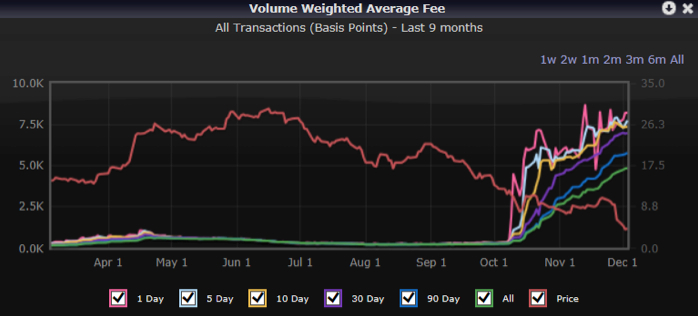

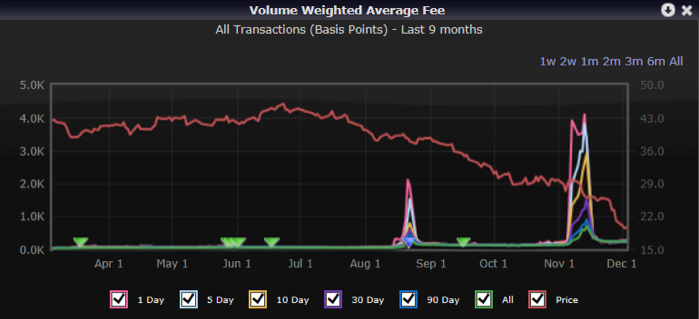

Goodrich Petroleum (GDP) is one such security. A $30 per share shale oil stock in June, this company is now limping below $4 per share as of this writing. Volume-weighted average fees have skyrocketed from a warm 300 basis points (bps) in early fall to a red-hot 8000 bps more recently. Utilization in GDP has jumped from 67% in June to around 96%. Goodrich’s corporate debt is also under significant selling pressure, and the 8.875% 3/15/2019 issue commands around 313 bps in fees to borrow and is currently 100% utilized. Even at its current low share price, the shorts seem to think that there may be more room to the downside in this name.

GDP volume-weighted average fees to borrow versus share price

Source: DataLend

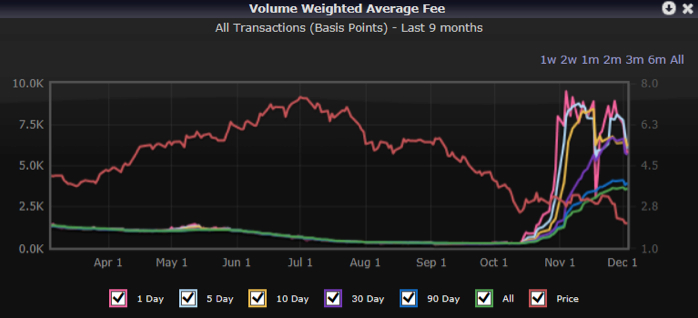

Halcon Resources (HK), another shale oil firm, is also undergoing intense selling pressure. This firm has seen active trading in the securities finance market all year, but only recently have fees to borrow spiked. Shorts were paying around 1400 bps in fees back in the spring of 2014, but as share prices rose into the summer, fees sagged to a low of less than 200 bps by September. That all changed in October as oil sold off, and fees to borrow this name skyrocketed to a high of 9515 bps on November 4. Fees have cooled a bit since then, but it still costs more than 5000 bps to borrow this name as the stock attempts to cling to $2 per share. Utilization is also very high at 95%.

Interestingly, Halcon’s corporate debt isn’t following the trend of the equity. Although its bond prices have also taken a nose dive, fees to borrow the 8.875% 15/05/2021 senior notes trade at only 11 bps. So too do the 9.25% 15/02/2022 notes.

HK volume weighted average fees to borrow versus share price

Source: DataLend

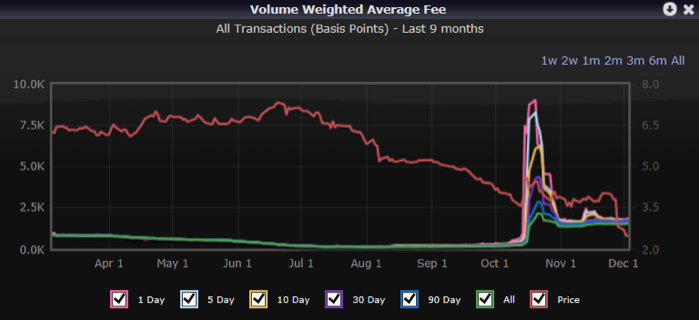

Sandridge Energy (SD), a horizontal drilling company, exhibited similar trading patterns, but with a few exceptions. Like Goodrich and Halcon, share prices began a gradual descent in the summer, but as oil began to sell off, the stock price actually got a temporary boost in mid October, right around the time that fees to borrow shot up from around 500 bps to an incendiary high of 9040 bps on October 21. The stock cooled almost as quickly as it heated up, and fees dropped back down to around 1500 bps the following week. Fees remain in a range of 1500 to 1800 bps as of this writing, and the stock is 93% utilized.

Like Halcon, Sandridge’s corporate debt also diverges from the trading patterns of its equity in the securities finance market. Fees to borrow the 7.5% 02/15/2023 debt are just 11 bps, and the security is only 3% utilized, despite having taken a nosedive in notional value. Other Sandridge corporate debt trades at higher utilization (from 23% to 31%, depending on the bond), but all seem to be trading GC like the 7.5% 02/15/2023 issue.

SD volume weighted average fees to borrow versus share price

Source: DataLend

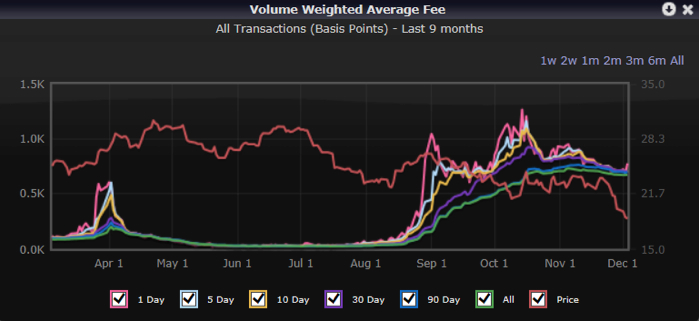

The share price of oil and gas exploration company Exco Resources (XCO) has weathered the storm a bit better than some of its competitors, but it is still a hot stock in the securities finance market. Fees to borrow shares have been warm all year in a 300 to 600 bps range, but like other companies it went very hot in October, hitting highs of 3400 bps. Fees to borrow have dropped somewhat to a currently hot 2168 bps. Utilization has also dropped a little from its high of 97% in late October to 90% today. This is another name where shorts may believe there is more room to fall.

XCO volume weighted average fees to borrow versus share price

Source: DataLend

The share price of oil and natural gas company Ultra Petroleum (UPL) hasn’t taken quite as bad of a nosedive as some of its competitors, but it is still off almost 40% from its April highs. Fees to borrow this company were slightly warm back in the summer, anywhere from 25 to 60 bps, but then shot up to a high of 1266 bps on October 14. Since then fees have dropped a bit to a currently hot 777 bps while the stock remains 87% utilized. It seems that the shorts aren’t done with Ultra yet.

UPL volume weighted average fees to borrow versus share price

Source: DataLend

Even large cap names have been impacted by the oil sell off. Offshore driller Transocean (RIG) is one such company, down a staggering 58% from its June highs. Fees to borrow RIG were barely warm for most of the year at around 40 bps, but that changed in early November when they shot up to a high of 3917 bps. The share price continued to sag, and fees soon followed suit, dropping back down to around 270 bps as of this writing. Transocean is currently 80% utilized. Shorts appear to be backing away from this name a little for now.

Transocean’s fixed income appears to trade in a fairly wide range in the securities finance market these days. The 6.500 11/15/2020 issue currently trades at a volume-weighted average fee of 176 bps and is 94% utilized. Similarly, the 3.800 10/15/2022 Transocean corporate bond commands 164 bps in fees to borrow and is 91% utilized. Conversely, the 4.950 11/15/2015 issue has a volume-weighted average fee of only 13 bps and is only 1% utilized. Likewise, the 7.350 12/15/2041 issue is 3% utilized and trades at a GC 11 bps.

Like the equity, Transocean bonds have been under selling pressure since November.

RIG volume weighted average fees to borrow versus share price

Source: DataLend

Despite the carnage in the above-referenced names, there are some oil and gas companies with high debt-to-equity ratios that have sold off in the cash markets but seem to have mostly escaped the notice of short sellers. These names include PetroQuest Energy (PQ), which has seen its share prices collapse from a high of $7.59 to $3.66 per share; it is only 14% utilized and currently trades at GC levels of 11 bps in the securities finance market. Memorial Resource Development (MRD), down 30% from its September highs, is another name that is mostly being ignored in the securities finance market right now. MRD’s utilization is a low 4%, and fees to borrow are a GC 11 bps.

Jones Energy (JONE) sold off from a June high of $20.50 to around $10.20 per share today. It has recently been trending warmer, but fees to borrow are still relatively low at 40 bps. Utilization in Jones Energy has increased to 62%, so it seems as if short sellers may be taking note of this name. Seadrill (SDRL) is another name that has gotten clobbered in the cash markets (down 67% from its June highs) but hasn’t been trading particularly hot in the securities finance market. Fees to borrow have been in a warm range, around 40-70 bps, for most of the fall. But SDRL is highly utilized at 88%.

Oil magnate Murray Edwards, chairman of Canadian Natural Resources, recently opined that oil prices could drop to as low as $30 per barrel. It seems highly unlikely that would happen anytime soon, but with a glut in supply and a strong dollar, oil could drop even lower than its current prices. If that is the case, the already low-priced drillers and shale oil companies could see continued interest from the securities finance marketplace.