Financial markets were designed to support the real economy: that’s their job. Within their collateral services offering, Euronext is working to bring commodities and investment funds into the electronic collateralized trading space alongside equities and fixed income. The vision is to promote the use of a wider range of assets for margin requirement coverage and financing purposes.

In an age of global banking corporations, hi-tech trading platforms and large scale investments, it can sometimes be forgotten that financial markets exist to support the formation of companies of all sizes. This gets accomplished by providing access to growth capital and liquidity in a regulated environment to maintain market stability.

Since the financial crisis of 2008, new global regulations, designed to protect market participants, have changed the way that trading exposure in many products is mitigated through the mandatory exchange of collateral both for exchange traded and OTC business. In Europe, regulations in the form of EMIR, CRD-IV, UCITS and AIFMD have increased the requirement for clients to provide collateral to conduct business in derivatives, repo, and securities lending. They have also increased the cost of doing business for banks that traditionally acted on their clients’ behalf to provide access to cash liquidity markets. This in turn has resulted in periodic market squeezes and price dislocations in liquidity markets during reporting periods, and an ever-increasing demand for eligible collateral.

The demand for Peer to Peer solutions and new repo asset classes

It is now apparent that there is a need for firms to be able to enter collateralized trading markets directly and choose a range of counterparties, rather than being confined to bank intermediaries that are understandably passing on the cost of new capital requirements. This need to generate liquidity without the cost associated with using an intermediary is not confined to holders of the assets most widely used for repo – fixed income and equity. It has expanded to traditional holders of commodities and to holders of ETFs, which, despite growing volume in Europe over the last decade, remain relatively low in terms of the number of financing trades.

An increased demand to post collateral to CCPs and brokers for certain segments of their business is testing the limits of such firms, not all of which have readily available eligible collateral. This becomes an inherent inventory management problem. One solution to this challenge is to perform a collateral transformation, which generally takes the form of a bank lending one type of collateral for another on behalf of their client. This process enables an asset holder to convert ineligible and sometimes lower grade assets into an asset that CCPs and brokers will accept.

This is a service that banks offer today but at a cost to the client; costs that are largely driven by the use of the bank’s balance sheet and resulting capital requirements. If banks have insufficient balance sheet capacity due to their regulatory requirements, firms will be forced to purchase and sell assets in the open market (even at a loss) to generate cash or other eligible collateral for the purpose of covering margin requirements.

A broad range of market participants need to collateralise their existing holdings for other purposes. The most obvious are pension funds that require cash to post as Variation Margin for bilateral OTC derivatives agreements. Government bonds are widely used for Initial Margin, but the market standard for Variation Margin is cash. If pension funds were forced to sell assets specifically for this purpose, industry analysis suggests this could require funds to hold over EUR300 million in cash and could reduce returns by 2% annually. A low-cost collateral transformation solution can solve this problem.

A more efficient and cost-effective option is for a firm to review all of their portfolio assets and convert those assets into eligible collateral themselves. This reduces the intermediary steps of bank collateral transformation, keeps cost low for firms needing collateral, and allows asset holders to utilise what they have already rather than trying to acquire new financial instruments just to meet a counterparty’s collateral schedule.

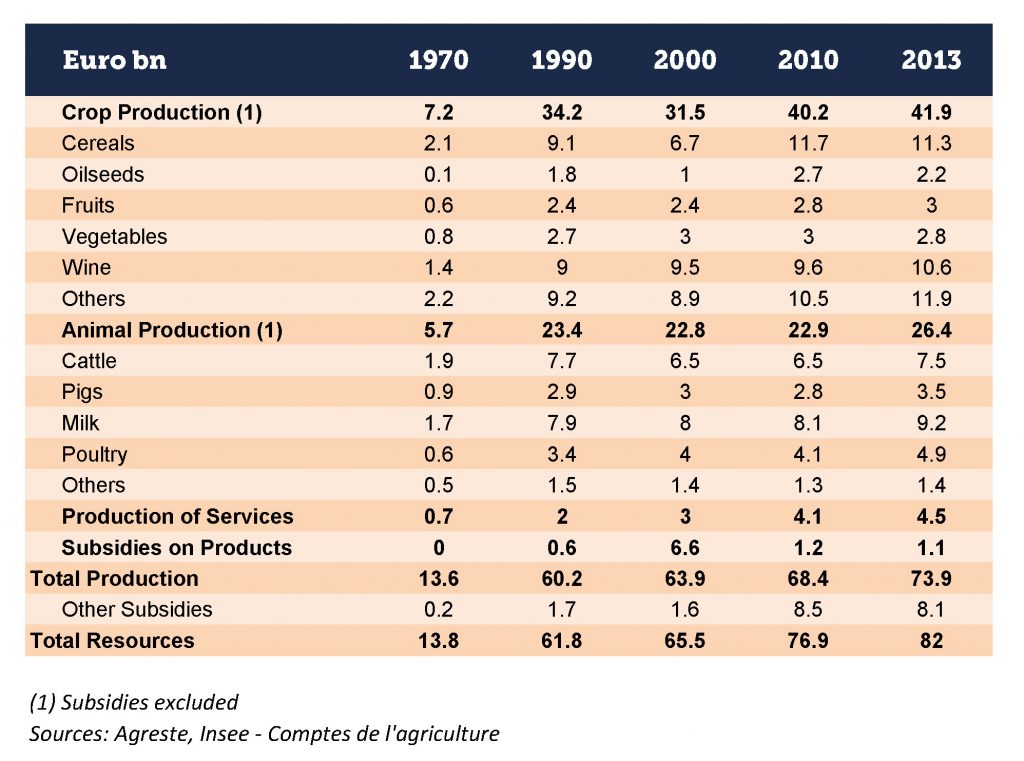

Similarly, agricultural commodities holders, including cooperatives that are currently borrowing cash from banks, could turn their assets into cash with an increased number of counterparties as options. This is a EUR80 billion industry in France alone and is fundamental to the workings of the real economy (see Exhibit 1). This can both lower borrowing costs for the cash lender and introduce a more robust risk framework for the bank lender that is able to monitor the electronic warrant within their inventory holdings. The assets could be in the form of commodities warrants or a commodities ETF. Either way, the digitisation and standardisation process would make these assets convertible into collateral, then into cash as a repo product. This would also allow commodities holders to make their financing process more efficient than using an outdated paper based model.

Exhibit 1: Agricultural production France: a EUR80 billion industry

Creating digitised commodities warrants alongside equities and fixed income works

In the third quarter of 2017, Euronext Collateral Services will bring to market an offering that allows holders of commodities such as agricultural products and precious metals to create electronic warrants, which can be used as collateral for repo trades to generate liquidity. Our Peer to Peer collateral trading platform will support commodities warrants and investment funds (initially ETFs) alongside equities and fixed income.

Taking agricultural commodities as an example, the process of creating an electronic warrant to represent a physical holding requires the creation of a network of approved locations (silos, warehouses, bank vaults, etc.) and the introduction of an inventory management platform to record holdings and transfers of ownership (to reflect outright buys and sales or loans). Euronext has put this structure in place as part of Euronext Collateral Services to support a range of assets that extend beyond those traded on the Euronext exchange, in response to feedback from the commodities community.

Once the warrant is created and represented by a standard identifier, it can be traded alongside standard repo and stock loan assets. This can lower costs and help increase returns by not forcing the sale of assets to raise cash for Variation Margin; or by allowing asset holders to avoid relatively high bank borrowing in place of a standardized repo agreement that is known and accepted by the market.

The same concept can also be applied to securities lending, currently a bilateral market with uneven levels of product standardisation. Digitising a basket of equities, or even single equity names, can enhance financing opportunities and enable short selling with the deliverable asset known, identified, and made available. The transparency this market provides to asset holders, cash investors, and any securities borrower fulfills a wide range of compliance and regulatory obligations, including best execution under MiFID II, and derivatives and securities finance reporting obligations.

Most importantly, Euronext Collateral Services is enabling asset holders in the real world to access the collateral markets for the benefit of economies and companies that need to finance assets. This is Euronext’s business mission, which will continue to drive our focus in the collateralised trading space. The more that assets can be efficiently and cost-effectively mobilised for collateral purposes, the more liquidity will be available for direct investment and economic growth.

Dennis Mullany is Head of Collateral Services at Euronext, responsible for the development of Euronext’s new collateral services. Dennis has extensive capital markets experience encompassing investment banking, central clearing and exchange traded business gained during roles with BAML and CME Clearing Europe.

Dennis Mullany is Head of Collateral Services at Euronext, responsible for the development of Euronext’s new collateral services. Dennis has extensive capital markets experience encompassing investment banking, central clearing and exchange traded business gained during roles with BAML and CME Clearing Europe.