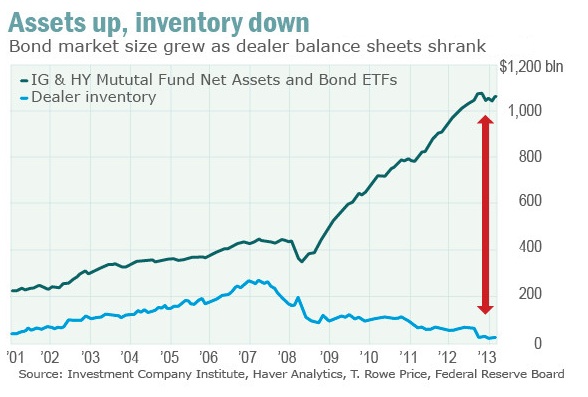

The fall in corporate bond liquidity has been well documented. Dealer inventory and market liquidity has plummeted in spite of enormous issuance. All that paper seems to be getting put away by real money accounts. Yields are too low to make a lot of sense for leveraged players – not enough carry to care much. Prop desks, who might have traded a lot of this paper as part of their positions, have disappeared – victims of the Volcker Rule, Basel III and reduced risk appetite. The must read on the topic is Ben Eisen’s “Mile Wide, inch deep, Bond market liquidity dries up” in Marketwatch.

The fear among investors is that (if and) when interest rates rise, there won’t be anyone willing to provide liquidity to sellers. That scenario feels like flying through an air pocket – the bottom dropping out flash crash style. The sudden unanticipated turbulence subsides when prices are attractive to liquidity providers – but they won’t be your traditional broker/dealers, more likely hedge funds with a “hit my bid, if you dare” attitude.

Is that market rout coming soon? A May 13th article in Moneywatch “Corporate bond rally is next to bust, some fear, It’s ‘better to leave early than to stay too late,’ say UBS strategists” certainly thinks so. From that article:

“…On Monday, Swiss banking giant UBS advised investors to trim holdings of investment grade and high-yield corporate bonds to get ahead of what it expects to be a pullback over the next six months or more. Last week, economist Nouriel Roubini described what he believes to be the beginning of a bubble in the credit markets. And high-profile bond investor Jeffrey Gundlach has been declaring for months that credit looks way too expensive…”

So, what is to be done? One solution was to avoid the capital / risk constrained dealers altogether. BlackRock put together the Aladdin Trading Network (ATN), an effort to link buy-side firms together for trading. The idea fizzled about a year ago and the business was folded into the MarketAxess portal. Not much has been heard since. Some in the market have said that BlackRock’s Aladdin Trading Network went nowhere because participants did not trust a competing buy-side firm to run the platform. We suspect the issues were rooted in a lack of consistent liquidity.

BlackRock just yesterday announced an alliance that integrates their Aladdin technology (not ATN but their front-to-back asset management engine) with Tradeweb’s systems, allowing for a more streamlined way to execute trades with the sell-side. It sounds like they create a better mouse trap by aggregating data. From the May 14th FT article “BlackRock signals bond trading shake-up” (sorry, behind the paywall):

“…Rather than set up an alternative trading system that would compete directly with banks, BlackRock is seen to be trying to aggregate fixed income liquidity from existing dealer-supported platforms for its existing clients…”

TMC Bonds and Codestreet have announced yet another approach. A May 13th article in The Trade News “US bond dark pool promises to bring new liquidity to the buy-side” by John Bakie describes a “dark pool” approach for sell-side firms. Called the Codestreet Dealer Pool, the system does everything it can to reduce information leakage. A “traditional” dark pool serves the clients of a single firm and information stays within (until the information is pretty much stale). On the other end of the spectrum are inter-dealer brokers (IDB), who are paid to drum up interest in a security from as many players as possible, spraying valuable information along the way. Codestreet seems to be a hybrid, something of an IDB multi-dealer approach but without spilling information to everyone in sight. They do this by using algorithms to figure out who likely buyers and sellers are.

Quoting James Wangsness, president of TMC Bonds,

“…Market participants are reluctant to make big trades in fixed income because they risk information leakage and the price moving away from them,” he said…”

“…If a tier one bank goes to an interdealer broker (IDB) to shift a position, the IDB will call around and leak sensitive information. Market participants keep orders small to not reveal too much their positions…”

“…“We’ve developed an algo with is able to bring together these disparate pools of liquidity, but instead of pushing prices out to a central marketplace, it looks at various aspects such as price, available inventory or order size and creates a score,” Wangsness explained. “Once it has a score, it can match two parties it identifies as having a chance to made a deal happen and then brings them into a private negotiation…”

“…Once the counterparties are in negotiation, if no deal can be agreed then no information is released to the market. Furthermore, the negotiation process is split to limit information leakage at every stage. Counterparties first negotiate their price, and only once that has been agreed do they consider the size of the trade, meaning neither party does needs to reveal the full scope of their order…”

So there is some intelligence behind matching prospective buyers and sellers. But it still raises lots of questions. How can there be a price negotiation without knowing how much size is to be traded? Markets clear based on, among other things, price and size. Will dealers really trust a black box approach toward pointing trades to certain dealers? Where is the information coming from to establish a prospective match?

And what about the underlying problem: banks simply don’t have the desire to dedicate capital to large inventories and can’t take the paper onto a back book anymore. We are wondering how Codestreet will engineer market depth where there was little before. The information piece is important, but is it really the primary bottleneck? Will protecting the broker/dealers from information leakage encourage the capital commitment those larger trades entail? Will the role of providing liquidity on corporate paper shift to the shadow banks — in which case any system that doesn’t include those players might suffer. We can see how Codestreet might ultimately displace inter-dealer brokers with a better mousetrap (and think that could be a pretty good marketing pitch), but we are skeptical it will create spontaneous liquidity.

1 Comment. Leave new

This is all about lack of trust between participants. I can understand it but it has got to a point where things will need to change.

The comments from exchanges (LSE for one this week) where volumes have recovered dramatically this year is illustrating that IPO’s and Rights Issues may now be a far better way for corporates to raise money and is happening. The lack of movement to a more transparent market model in bonds and frustration of regulators to see change embraced will only drive this move forward to the detriment of new issues in bond markets.

The Buyside investment strategy has changed and is now driven by a more buy and hold scenario and unless the banks, buysides, exchanges and regulators all push for open markets with dark pools running in the background nothing will change. Maybe they should look at Government Bond markets first and drive the most liquid markets onto an exchange/COB to get people used to the idea as we know that change to a market that has not really moved on from Big Bang is a very difficult thing to do.