The Office of Financial Research’s annual report to Congress assesses financial stability.

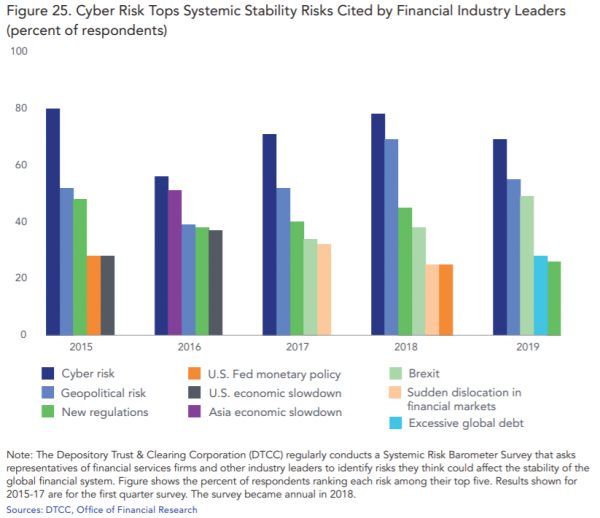

For several years, respondents to a survey of industry leaders have ranked cyber risk as the top risk facing the financial system. Geopolitical risk almost always has ranked second. Brexit risk has come in third or fourth in recent years.

Financial services executives are not alone in rating cyber risks above all others as a threat to financial stability. The OFR has ranked it as a major concern since its inception. Policymakers rank it that way, too. Federal Reserve Chair Jerome Powell has described it as the largest risk now challenging the Fed, financial institutions, and financial markets. Cyber risk looms so large because the critical infrastructure for the economy and the financial system is computer-driven and networked. Networks are growing and changing, making the transmission of risk more complex.

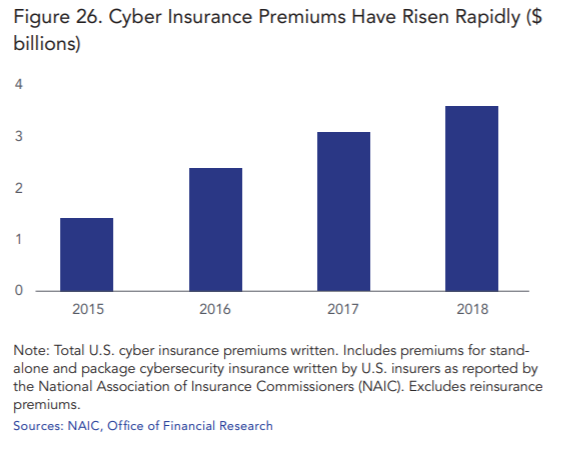

Aside from a review of some of the most serious breaches throughout the year, the OFR noted another source of cybersecurity risk for the financial sector is through insurers’ exposure to claims. Premiums on cyber insurance policies written have been rising. At the same time, the insurance industry is concerned that it lacks a good sense of its potential exposure to claims in a major cybersecurity event. The industry also lacks good data to support its pricing and underwriting policies, which itself is a vulnerability.

Here are the key takeaways from the 2019 assessment:

- Solvency and leverage risk is generally low. Bank capital ratios remain higher than

- before the 2007-09 financial crisis and exceed U.S. regulatory minimums. Life insurance

companies’ capital ratios also exceed minimums set by state regulators. - Macroeconomic risk is elevated. The US economy continues to perform well.

However, fading momentum in some key US and global indicators could pose risk

to the outlook. Uncertainty about outcomes of trade negotiations and the United

Kingdom’s exit from the European Union could also contribute risk to the outlook. - Market risk remains elevated. Fundamental asset price appreciation reflects strong

economic performance and expectations for continued growth. Indicators also highlight, however, that valuations for important asset types, including stocks, corporate

debt, and some types of real estate, are above historic levels. - Credit risk remains moderate on balance. Increased borrowing by nonfinancial businesses is consistent with a strong outlook for the U.S. economy. In addition, household

credit risk is low and somewhat improved from a year ago. Several metrics also suggest,

however, that nonfinancial corporate debt and leverage may be elevated. Weaker creditor protections, combined with lower subordinated debt cushions, could result in creditors recovering less money on leveraged loans in the next downturn. - Funding and liquidity risk is moderate. Risk from market illiquidity is moderate, but

can change quickly with market sentiment. Some recent periods of higher market volatility saw trading liquidity temporarily weaken. Also, there was a spike in repo rates in

September 2019 associated with reduced market liquidity. This event was short-lived. - Contagion risk remains moderate. For the largest banks and insurers, contagion risk

is generally little changed since 2016. However, this risk rose around the end of 2018,

when market stress spiked. Connectivity among financial firms is a key driver of changes

in contagion risk. As market risk receded, so did risk of contagion. - Other risks continue to grow in importance. Cybersecurity risk remains a concern.

Several major cybersecurity events in the financial sector highlighted this risk, including how technology firms contribute to it. Brexit poses operational risk associated

with potential disruptions to supply chains and financial contracts. Failure to prepare

adequately for the end of LIBOR is another threat to financial stability. As with Brexit,

the transition from LIBOR requires renegotiating many contracts, creating risk. Digital

financial assets such as cryptocurrencies continue to potentially transform financial

markets, but their risk to financial stability is lower than a year ago because of their

reduced market capitalization.