On December 8th, Finadium presented a client webinar on blockchain and collateral management technology. This was presented as a follow-up to the Finadium research reports “Can the Blockchain Work for Securities Finance, OTC Derivatives and Other Collateralized Transactions?” and “Technology Vendors in Collateral Management: A Finadium Survey.” More than 100 customers registered for the 45 minute event. Many more dialed in and followed along with the presentation posted on Securities Finance Monitor. The level of attendance certainly confirms that the subject of blockchain technology and its impacts on our industry remains high on the list of things to think and/or worry about.

Interest in blockchain was reinforced by the results of a quick poll we conducted near the end of the session.

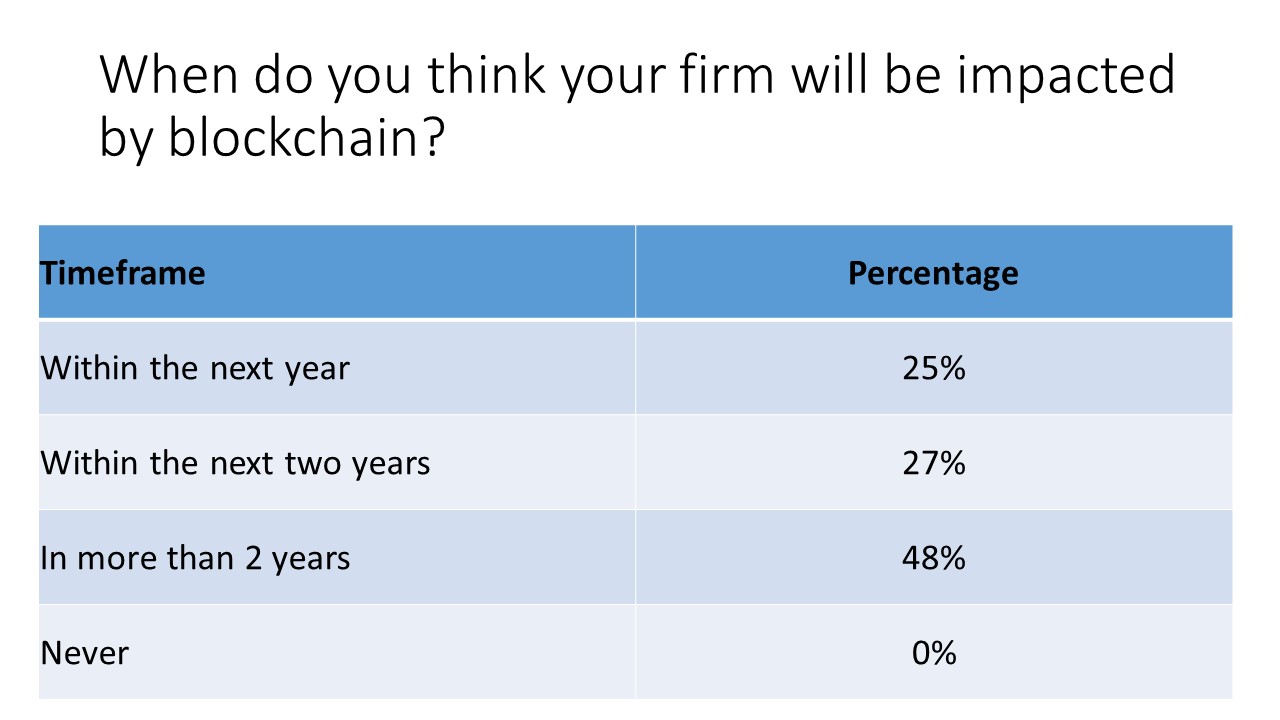

Source: Finadium webinar survey, December 8, 2015

The upshot is: attendees at our webinar see blockchain networks as real and imminent – with 100% of respondents saying they will be impacted by blockchain technology at some point, and more than 50% saying it will happen within 2 years. No one thinks it’s all just smoke and mirrors.

Our customers and attendees were well prepared with questions – more questions than we could answer in the time allotted. The questions ranged from clarifications on the nature of the technology to very specific questions about real-life applications. Some of the questions and answers are shared here with slightly more detail than the webinar format allowed us to provide “live”:

Q: Is it true that a distributed ledger allows everyone in the network to see everyone else’s balances and transactions?

A: This is a core feature of the technology, and one that regulators in particular find very attractive and interesting. Distributed ledgers have been described as “triple entry bookkeeping” – showing the starting balance, the ending balance and the transaction that that moved the balance.

In a public blockchain network, participants self-identify – using their real or alleged identity – which helps maintain some level of anonymity. You can’t hide the balances or the transactions but you can hide the real identity of the participant. In a closed network, as we expect virtually all networks to be in financial services, this runs up against regulatory and practical expectations like OFAC. This will be a very important consideration for the industry – will the participants be able to mask or encrypt their identities some purposes, while ensuring participants’ real identities are known for other purposes?

Q: Won’t the databases become gigantic?

A: Yes, they certainly could.

Q: If distributed ledgers were housed at an external vendor managing the network, why would each participant need a separate copy? Wouldn’t that be unnecessary or redundant?

A: This would be a question of how the network was technically implemented by the vendor. What differentiates a blockchain ledger from a traditional proprietary “shared” ledger is that, conceptually, no single entity owns or controls the data. In theory, the database manager has no backdoor into the data. Only valid transactions confirmed across the network can modify the data.

For illustrative purposes, Finadium has described a hypothetical Corporate Actions/Entitlements blockchain network. We received a number of questions about just how such a network would be implemented and how it would change the roles of players in the industry. Our answers are provided with the caveat that Finadium has not yet been approached to actually design such a network, so all answers are hypothetical.

Q: In your example, what would the role of the custodian, asset manager or others currently acting as agent for the customer be?

A: The key to a successful Corporate Actions network would be to eliminate the financial role of the intermediaries. We mean that agents, custodians, brokers and others who process corporate actions on behalf of the ultimate beneficiary would never take possession of the entitlement or have a financial role in the transaction. A successful network would change the role to that of a technological assistance service – providing technical support and process management, and technical access to the network. The ideal state is that the corporate issuer of the entitlement would use the network to directly allocate payouts to the end user. This would eliminate PIL and other tax complications as well as substantially reduce operational and financial risk for all parties.

Q: What about voluntaries? Could the network support those?

A: Provided the voluntary, like the mandatories, was a finite pool, there’s no reason it wouldn’t work. Usually voluntaries are pre-defined as a specific subscription based on a dollar amount or against a defined number of shares or other units.

Q: In this network, how do you ensure the right number of entitlements exist? What’s to prevent someone from claiming or paying incorrect amounts?

A: This goes to a core characteristic of the technology, which is “trust” in the unit of exchange. The network must be designed in such a way that all participants can trust that the unit of exchange is absolutely valid, cannot be counterfeited, and that possession/ownership of all units is known at all times. This would suggest that the corporate issuer (or their processing agent) of the entitlement would be the issuer of the “unit of exchange” – they would be the only entity able to add or remove units of exchange from the pool.

Finadium was pleased to present this webinar, and hope that all who attended gained value and additional insight into the subject. Clearly there is much, much more to come on blockchain, and we will continue to research and analyze the subject, and to work with our customers and the industry on a go-forward basis. Should you have comments or additional questions, please contact Finadium directly at info@finadium.com.

Here is a link to the recorded webinar and the presentation.