Our recent survey of large mutual fund, UCITS fund and insurance company managers reveals asset manager thinking on whether securities lending fees are opaque or transparent, and which direction it is moving.

As part of Finadium’s 2013 asset manager survey, we asked whether managers thought that the fees and/or rebate rates they received as part of securities lending transactions were opaque or transparent. In order words, could asset managers tell best execution when they saw it? This has particular relevance for two reasons we can think of:

1) As asset managers work to benchmark their service providers and internal performance, what are they really benchmarking? If fees/rates are opaque and differ substantially by loans and counterparties, then agent lenders and internal lending desks should not be expected to conform to a benchmark. Rather, each loan will have its own dynamics and associated fees.

2) As regulators warm towards the idea of a Trade Repository for securities lending, should any analysis be considered statistically valid? Should any reports that come out of a Trade Repository be used for internal purposes or should they simply be noted and deleted?

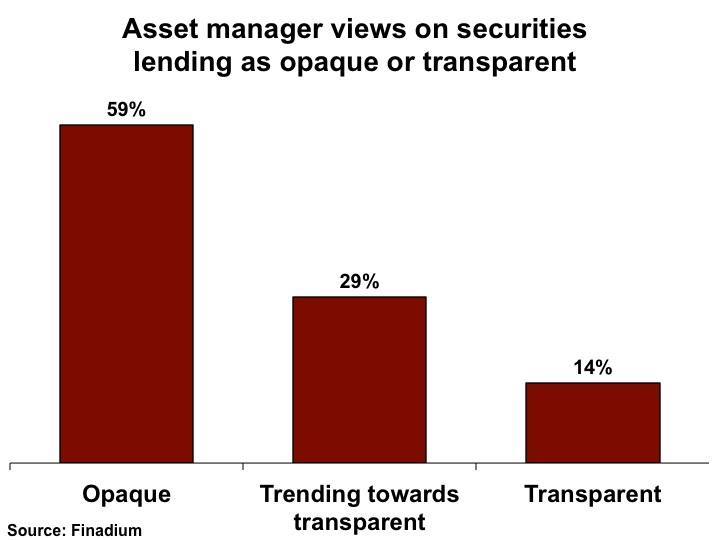

According to the 39 executives we heard from across 31 large asset management firm, 59% thought that the securities lending market was opaque and not heading anywhere. Another 29% thought the market was trending towards transparency, and the remaining 14% thought that is was already transparent for all general purposes.

(Click to enlarge)

Ideas to consider:

This result suggests to us, consistent with our experience as consultants, that benchmark information needs context behind it in order to be most relevant. Data by itself is useful, but the tendency of an asset manager/beneficial owner to look at a report, not have context and so put the report in a drawer means that the information doesn’t hit home. Putting the report in the context of the manager’s lending parameters, agent lender behavior and market trends makes the information resonate in an otherwise opaque market.

This information also suggests that regulatory reports from any new Trade Repositories will not be taken seriously by large asset managers without much more additional context than a “ticker” type of securities lending data feed will provide. We wrote up our thoughts on securities lending data feeds in our April 12, 2012 article, “Intraday Securities Lending Data and a Securities Lending Ticker,” and most asset managers agree that securities loans remain unstandardized. Any standardized database including a Trade Repository will need to be extremely selective about what data are used to comprise its metrics and reports if these will be for public consumption.

We find that the opinions of large asset managers, pension plans and sovereign wealth funds can tell a lot about the direction of the securities lending industry, and by extension related financial markets. We will release the full results of our 2013 asset manager survey in early August.