Chinese margin requirements were eased to prop up the equities market. But all this does is transfer the risk to the lenders. In this case, one of the lenders is the Chinese Securities Finance Corp., which can now source liquidity from the People’s Bank of China. Is this responsible lender of last resort behavior or moral hazard on steroids?

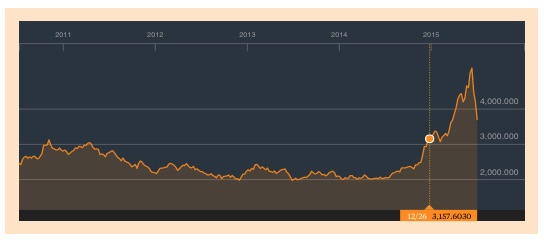

We don’t often look at the Chinese stock market, but recent developments have struck a chord. The performance of the market has been nothing short of spectacular, both in terms of the incredible rally and the violent correction that seems to be in mid-stream.

{kind=link}

Source: http://www.bloomberg.com/quote/SHCOMP:IND

Margin lending has been a driver of the market. Last January 19th, we saw an interesting article in the FT: “Explainer: Margin finance in China” by Gabriel Wildau (sorry behind the pay wall). Looking at the basics, Wildau wrote:

“…Before 2010, margin financing was not officially authorised in mainland Chinese stock markets, although it occurred informally on a small scale. The China Securities Regulatory Commission launched a pilot programme for margin financing in March 2010. It became a standard programme in October 2011…”

Clients needed to have an account in place for 18 months before using margin loans. Minimum account value is Rmb 500,000 (currently a little over $80,000). Margin lending was set with a 50% haircut.

“…But in 2013 the CSRC lowered the account-opening requirement to six months and said it was cancelling “window guidance” on the minimum value of account holdings. Brokers interpreted this change to mean they were now permitted to set their own requirements. Actual limits ranged from Rmb2m to zero…”

Subsequent guidance from regulators “…reiterated the minimum Rmb 500,000 threshold.The initial margin requirement is 50 per cent of the margin portfolio in the form of cash or securities…” But does everyone follow the rules, especially the large shadow bank segment? (As an aside, if you set a Google search to report on “shadow banking” references, we have noticed that for a while now the vast majority are articles on Chinese shadow banking…)

Another FT article, published July 2nd “Chinese relaxation of lending rules fails to support flagging stocks” written by the same journalist (sorry, also behind the pay wall), said that regulators have now authorized the Chinese Securities Finance Corp, who provides liquidity to securities companies, fund managers, institutional shareholders of listed companies, and other market participants, to ease up on margin lending rules. The response to the tumble in the Chinese market has been to change the rules to make it easier for investors to hold onto their leverage. If securities finance is an out of the money put sold to cash borrower, it sounds like the strike price just got a lot less out of the money. It is already very painful for the investors. Is this going to end well for the lenders? Doesn’t seem like it.

“….CSRC on Wednesday said brokerages were now free to set their own rules for demanding more collateral from clients when stocks bought with borrowed money fall in value. Previous rules required clients to add assets to their accounts when their collateral ratio dropped below 130 per cent, or else liquidate their positions…”

“…“The new CSRC rules to stop forced liquidation have hit the nail on the head and will calm the market for now,” Hao Hong, research director at Bocom International, wrote in a note…”

Chinese margin loans had a 6 month maximum term. It seems that the loans had to be fully repaid periodically – a good discipline to have. That has been eased too.

The Chinese Securities Finance Corp also had a capital increase, going to 100 billion Rmb (US$16 billion) from 24 billion Rmb. To put this in perspective, the recent fall in Chinese stock prices wiped out $2 trillion. But the CSF is only one source of margin loans. According to a July 7th article in the FT, “Explainer: What is Chinese Securities Finance Corporation?” also written by Gabriel Wildau (yup, paywall again):

“…Today brokerages mainly finance their margin loans by issuing stock and bonds and borrowing on the interbank money market. But CSF also makes funds available to brokerages to facilitate margin loans to brokerage clients, much like a central bank lends funds to commercial banks. CSF is also involved in securities lending to facilitate short selling…”

We can’t help to be reminded of the transmission of systemic risk facilitated by securities financing during the Financial Crisis and wonder if that flavor of inter-connectedness is present in China now?

This is what really caught our attention: It looks like the Chinese regulators are concerned about forced liquidations (read: fire sales). But in the process, have given Chinese securities dealers a lot more flexibility to decide when to call margin and when to let it slide. Is the Chinese market one of those “reversion to mean” places where holding off will allow fair value to come back? Where is the fair value when there is this kind of bubble? The result is the risk going from speculator to lender and ultimately making the banking system (including the web of shadow banks so prominent in China) a lot more risky.