The European Central Bank (ECB) published the results of its annual supervisory review and evaluation process (SREP), which showed that banks have banks have solid capital and liquidity positions, and have increased profitability.

- Internal governance, risk management and capital planning remain key areas for supervisory action in light of deteriorating risk outlook

- Overall average SREP score broadly unchanged; Pillar 2 requirements for CET1 capital set at 1.2% on average, compared with 1.1% in 2023

- Overall CET1 capital requirements and guidance increased from 10.7% to 11.1%, reflecting impact of macroprudential policies

- Supervisory priorities adjusted to focus on building resilience to short-term risk outlook, strengthening governance and climate and environmental risk management, and making further progress in digital transformation and operational resilience

The SREP is a core activity of European banking supervisors, enabling them to assess the risks banks face and how well banks are managing them. Based on the results of the SREP, the ECB specifies capital requirements and issues qualitative measures to remediate deficiencies for each bank. The SREP outcome also feeds into the ECB’s supervisory priorities for the next three years.

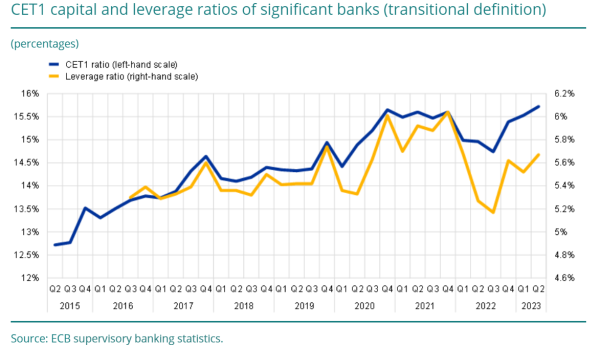

The euro area banking sector continued to be strong and resilient in 2023. On average, banks maintained solid capital and liquidity positions, well above regulatory requirements. Banks’ profitability returned to levels not seen in over a decade, strengthening their ability to withstand external shocks, as the results of the 2023 EU-wide stress test showed.

In a speech, Andrea Enria, chair of the ECB’s Supervisory Board, said that significant banks “generally have robust capital and liquidity positions.”

“This year’s stress test, characterised by the harshest adverse scenario since the inception of European banking supervision, buttresses our view on the resilience of the sector as a whole. Significant banks reported around €70 billion of unrealised losses on securities at book value. This amount is contained compared with that reported by banks in the United States, where valuation losses played a key role in the spring 2023 turmoil involving regional banks. Furthermore, available analysis shows that unrealised losses in the banks we supervise would also remain manageable under adverse scenarios of further interest rate hikes,” he said.

The weak macroeconomic outlook, however, and tighter financing conditions remain a source of risk for European banks. The rapid increase in interest rates has helped boost banks’ overall profitability, but this effect will diminish as they pass higher interest rates on to depositors. At the same time, higher rates have contributed to credit, valuation and liquidity risks. The March 2023 market turmoil highlighted just how important it is for the banking sector to manage interest rate risk effectively.

In this context, the average SREP score remained broadly stable at 2.6 (in a range of 1 to 4), with 70% of banks scoring the same as in 2022, 14% scoring worse and 15% scoring better.

The ECB stepped up efforts to ensure banks took overdue action to address outstanding findings and measures imposed on them. It issued qualitative measures, a key component of its supervisory toolkit, primarily to address deficiencies related to internal governance, credit risk management and capital planning. Banks need to keep paying particular attention to internal governance, as three out of four have received measures to address deficiencies in that area. There was a substantial rise in measures issued to address liquidity risk and interest rate risk in the banking book, triggered by the changing macro-financial landscape.

During the 2023 cycle, supervisors worked to gain a better understanding of the factors underlying weak business models. They noted that recurring structural weaknesses are attributable to poor strategic planning and insufficient diversification, further exacerbated by shortcomings in internal governance.

After this assessment, the bank-specific Pillar 2 requirement (P2R) for Common Equity Tier 1 (CET1) capital slightly increased on average from 1.1% to around 1.2% of risk-weighted assets (RWAs). The P2R includes add-ons for risky leveraged finance for eight banks, and add-ons for non-performing exposures for 20 banks.

The overall requirements and non-binding Pillar 2 guidance in terms of CET1 capital increased on average to 11.1%, compared with 10.7% in 2023. This was driven mainly by several countries re-introducing or increasing their countercyclical capital buffers and, to a lesser extent, by changes in risk profiles and in add-ons for non-performing exposures. The overall requirements and Pillar 2 guidance in terms of total capital increased slightly to 15.5% of RWAs, from 15.1% in the 2022 SREP cycle.

The ECB, for the first time, applied a leverage ratio Pillar 2 requirement to six banks with a particularly high risk of excessive leverage. This bank-specific mandatory requirement amounted on average to 10 basis points and is in addition to the minimum 3% leverage ratio binding requirement for all banks. The ECB also applied a leverage ratio Pillar 2 guidance to seven banks.

In addition, the ECB imposed quantitative liquidity measures on three banks, requiring minimum survival periods and a currency-specific liquidity buffer.

In this context, the ECB has slightly refocused its supervisory priorities for the next three years. To strengthen banks’ resilience to immediate macro-financial and geopolitical shocks (Priority 1), the ECB will ask banks to address shortcomings in their asset and liability frameworks and credit and counterparty credit risk management. Banks must also accelerate the effective remediation of shortcomings in internal governance and the management of climate-related and environmental risks (Priority 2). Furthermore, they must make further progress in their digital transformation and in building robust operational resilience frameworks (Priority 3).