A recent report from the European Central Bank (ECB) highlighted that linkages with the non-bank financial intermediation (NBFI) sector expose banks to liquidity, market and credit risks, with liquidity risk seeming to be the main concern at present, and that a small group of systemically important banks is key to ensuring the smooth operation of parts of the NBFI sector.

Banks are connected to NBFI sector entities via loans, securities and derivatives exposures, as well as funding dependencies. Linkages with the NBFI sector expose banks to liquidity, market and credit risks. Funding from NBFI entities would appear to be the most likely and strongest spillover channel, given that NBFI entities maintain their liquidity buffers primarily as deposits and very short-term repo transactions with banks.

At the same time, direct credit exposures are smaller and are often related to NBFI entities associated with banking groups. Links with NBFI entities are highly concentrated in a small group of systemically important banks, whose sizeable capital and liquidity buffers are essential to mitigate spillover risks.

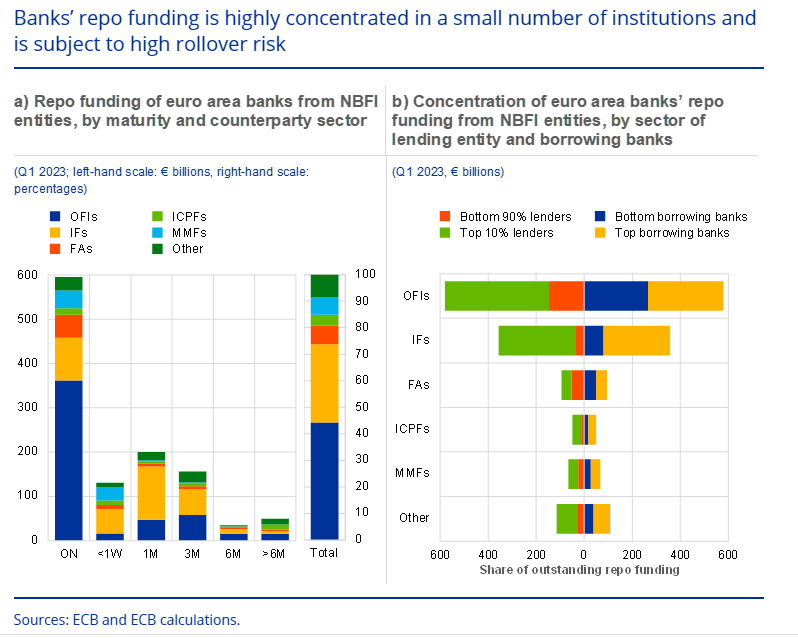

NBFI entities play a major role as providers of repo funding to banks. In the last quarter of 2022, almost half of all repo funding to banks came from these entities. The share of euro area bank repo funding from non-banks has fluctuated between 41% and 54% since 2015. Investment funds and other financial institutions are the largest group of NBFI entities providing repo funding to banks, with French, German and Dutch banks being the main recipients.

The bulk of the NBFI sector’s repo funding to banks has a very short maturity. Around half the repo funding provided by NBFI entities consists of overnight transactions, while almost 80% of volumes have a maturity of one month or less. This suggests that banks may face significant rollover risk.

The bulk of the NBFI sector’s repo funding to banks has a very short maturity. Around half the repo funding provided by NBFI entities consists of overnight transactions, while almost 80% of volumes have a maturity of one month or less. This suggests that banks may face significant rollover risk.

As is the case for unsecured deposits, repo transactions often serve as a liquidity buffer for NBFI entities, in particular for investment funds and other financial institutions, including broker-dealers (Chart B.2, panel b). Banks might therefore need to replace the funding obtained in the repo market very rapidly if the NBFI sector were to be hit by large, abrupt outflows.

Banks’ funding from NBFI entities is highly concentrated, on both the borrower and the lender side. Large banks account for about 80% of euro area banks’ total repo borrowing from NBFI entities. These banks play a central role in the market, as they are virtually the only recipient of repo liquidity from investment funds, insurers, pension funds and money market funds. Most of the repo volume is also concentrated in a small number of lenders. The top 10% of lenders by size provide 88% of total funding. These figures suggest that concentration risk is elevated, as there is a small number of banks which heavily rely on repo funding, which is provided by a small number of NBFI entities.