The European Central Bank (ECB) published its final report on “Sound practices in counterparty credit risk governance and management”, following a public consultation which ended in July 2023.

The report presents the findings of the targeted review performed in the second half of 2022 on how banks govern and manage counterparty credit risk (CCR). It highlights sound practices observed in the market and points to areas where improvement is needed. The sound practices described in the report go beyond mere compliance with regulatory requirements and institutions are expected to consider them when designing their approach to CCR management.

The ECB noted that over the past ten to fifteen years, the low interest rate environment fostered search-for-yield strategies and incentivized some banks to increase the volume of capital market services they provided to more risky and less transparent counterparties, often non-bank financial intermediations (NBFIs) and less regulated or unregulated entities such as hedge funds and family offices.

Following the collapse of Archegos Capital Management, the ECB, like other supervisors of major jurisdictions, reviewed the risk management practices of a sample of banks that were particularly active in providing prime brokerage services, a specific capital markets activity with high CCR exposure, and in August 2022 published its supervisory expectations for prime brokerage services (PBS).

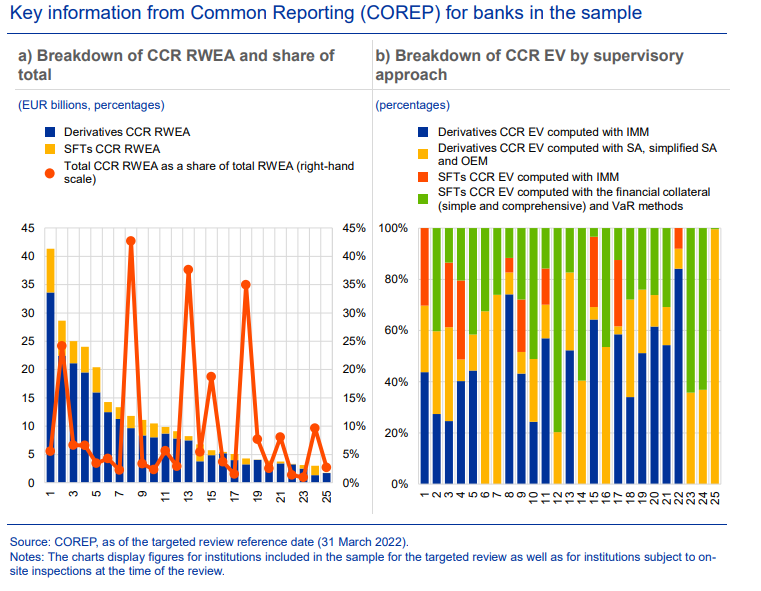

In the last quarter of 2022, the ECB concluded a targeted horizontal review of governance and risk management of CCR at 23 institutions that were materially active in derivatives and securities financing transactions (SFTs) with non-banking counterparties. The review was also an occasion to assess how some banks were meeting the expectations on PBS, which are reflected – albeit in more general terms – in the sound practices presented.

Material shortcomings

The targeted review confirmed the progress already made by institutions and identified a number of good industry practices. However, it also exposed several material shortcomings compared with sound practices, even accounting for differences in terms of scale, complexity of the business, products offered and nature of the counterparties.

More specifically:

- Customer due diligence procedures, both at onboarding and on an ongoing basis, should be improved when dealing with non-banking counterparties and have a substantial impact on credit decisions and contractual conditions. This includes taking a more conservative approach towards setting credit terms for clients failing to provide information transparently. First and second lines of defense (1LoD and 2LoD) should monitor those counterparties to ensure they provide transparent information on whether sufficient shock-absorbing capacity and adequate policies, procedures and controls are in place.

- Institutions with material or complex CCR exposures should explicitly specify their willingness to accept this risk in their risk appetite statement, rather than capturing it implicitly in credit risk, as CCR might present additional complexities compared with general credit risk.

- The stress testing framework should address not only counterparties’ creditworthiness, but also their vulnerability to specific exposure tail events, where such vulnerabilities can be magnified by combinations of wrong-way risk (WWR), high leverage, maturity mismatch and non-linearities resulting from exposure to crowded trades. The framework should aim to identify counterparties whose solvency or liquidity position might come under pressure in certain market scenarios, and to detect concentrations in exposures to margin shocks, a significant build-up in credit exposures or vulnerabilities to rapid deleveraging, among other potential vulnerabilities. The frequency of stress tests should reflect a rapidly changing risk environment. Stress testing results should have an impact on decision-making, including proactive risk mitigation strategies.

- There is still room for improvement in how, on a firm-wide basis, CCR is mitigated, monitored and managed when a counterparty is in trouble or defaults. In many cases, static margins have not yet been replaced with more risk-sensitive arrangements. Early warning indicators specific to derivatives and SFTs, such as discipline in margin payments, are not always considered when compiling watchlists