29 Jul 2016 – How interconnected are CSDs? The latest ECSDA overview of CSD links reveals some interesting facts and figures on existing linkages between European CSDs.

What we call a “CSD link” is an arrangement allowing a central securities depository to give its clients access to securities maintained in another CSD, without requiring the clients to be direct participants in the other CSD. Links thus facilitate cross-border securities deliveries.

Based on data collected in the first half of 2016, ECSDA has produced an overview of CSD links which sheds some light on the dense network of links which European CSDs have developed over the past few years.

What we call a “CSD link” is an arrangement allowing a central securities depository to give its clients access to securities maintained in another CSD, without requiring the clients to be direct participants in the other CSD. Links thus facilitate cross-border securities deliveries.

Based on data collected in the first half of 2016, ECSDA has produced an overview of CSD links which sheds some light on the dense network of links which European CSDs have developed over the past few years.

- Only 4 of the 41 ECSDA members have no links at all with other CSDs. Another 4 CSDs have no “outbound links” to other CSDs, but they allow foreign CSDs to access their domestic market (so-called “inbound links”). The remaining 33 CSDs have at least one link with another European CSD.

- If we set aside the three CSDs which maintain an unusually high number of links (Euroclear Bank, Clearstream Banking Luxembourg and SIX SIS), European CSDs have on average 7 links to other CSDs. The number is even higher for CSDs established in the EU (8.5 links on average).

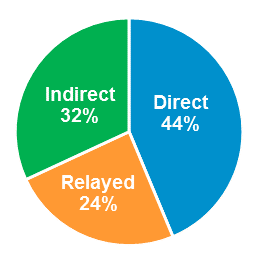

- The majority of CSD links (44%) are direct links whereby a CSD is a direct participant in another CSD. Indirect links (whereby assets are held via an intermediary acting as sub-custodian) and relayed links (whereby assets are held via a “middle” CSD) account for 32% and 24% of the total number of links respectively.

- Around 2/3 of CSD links allow for settlement on a delivery versus payment basis, meaning that not only securities but also cash transfers are possible through the link. The vast majority of links allow for the transfer of different types of securities, including equities and debt instruments.

- More than half of CSD links are used on a daily basis by market participants. 39% of the remaining links are used infrequently (e.g. on a weekly or monthly basis), and 9% have been established but are not currently used due to lack of market demand.

To find out more:

- Read the full report “Overview of CSD links in Europe”

- View the matrix of links among ECSDA members (Excel file)