The European Securities and Markets Authority (ESMA), the EU’s financial markets regulator and supervisor, published its Trends, Risks and Vulnerabilities (TRV) Report. Overall, risks in ESMA’s remit remain high, and investors should be prepared for further market corrections.

Verena Ross, ESMA’s chair, said in a statement: “Financial markets remained remarkably stable in 2H22, despite the general volatile environment. Although economic sentiment has become more positive in early 2023, there is no room for complacency. ESMA is keeping the overall risk assessment across its remit at the highest level. The confluence of high risks across the ESMA remit and fragile market liquidity may test the resilience of the financial system against possible future shocks.”

The second half of 2022 was dominated by the slowdown of economic activity, high inflation, global tightening of financial conditions, the geopolitical environment and the materialization of peripheral risks linked to leverage and liquidity, together with growing concerns over business practices in the crypto space. These remain the defining drivers of risk in EU financial markets at the current juncture.

Main findings:

Overall risk assessment: Contagion and operational risks are considered very high, as are liquidity and market risks. Credit risk stays high and is expected to rise, reflecting the growing concerns over public and corporate indebtedness. Risks remain very high in securities markets and for asset management. Risks to infrastructures and to consumers both remain high, though now with a worsening outlook, while environmental risks remain elevated.

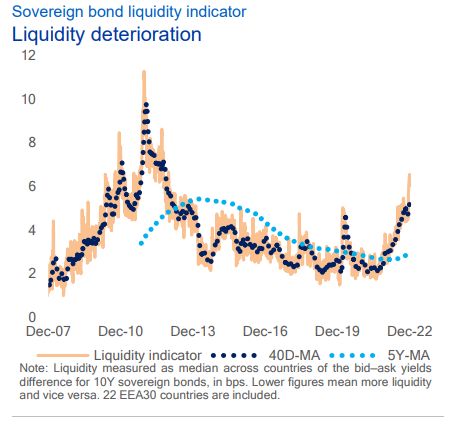

Market environment: The tightening of financial conditions globally has weighed on economic activity, while inflation remains very high. Volatility in energy markets stayed elevated despite a general decline in prices. Structural vulnerabilities expose markets and participants to the risk that shocks to markets could be amplified by liquidity supply and demand imbalances.

Securities markets: Equity prices were volatile in 2H22 with markets partially recovering 3Q22 losses based on news flow around relatively stable inflation and positive corporate earnings.

Asset management: The EU fund sector has seen outflows and low performance across most fund types in 2H22, as assets under management experienced their sharpest decline since the Global Financial Crisis. Maturity mismatches in Commercial Real Estate Funds persist, and the impact of the UK Gilt market turmoil on leveraged Liability-Driven Investment Funds in 2H22 confirmed existing concerns over fund liquidity risk management and excessive leverage, as well as contagion risks given strong systemic interconnections.

Consumers: Investor sentiment remains weak, against the backdrop of economic uncertainty. Inflation acts as a drag on real investment returns and contributes to falling household savings.

Infrastructures and services: Central clearing volumes grew further, as margins collected by EU CCPs for interest rate and commodity derivatives rose with rises in prices and volatility in underlying instruments, while some migration from ETD to OTC energy derivatives was observed.

Market-based finance: Capital market financing decreased sharply in 2022, turning negative for the first time since the Covid-19 related market stress in early 2020. The drop in activity is linked to high investor uncertainty, tighter credit standards for firms, high corporate debt levels and a rapid increase in the overall cost of external financing in the euro area. Looking ahead, market and liquidity risk in fixed income markets remains very high.

Sustainable finance: Net-zero pledges have come under growing scrutiny, with the energy crisis jeopardizing decarbonization objectives. More broadly, the focus on greenwashing has increased while investors increasingly appear to differentiate between products based on their sustainability credentials, as reflected in steady net flows into SFDR Article 9 funds. Despite this, ESG markets continued to grow, with this trend showing resilience to broader market developments.

Crypto-assets and financial innovation: Cryptoasset valuations have now fallen by almost 70% year-on-year, driven by macroeconomic factors and several high-level collapses in 2022. The recent failure of FTX, formerly one of the largest centralized crypto exchanges, triggered some large market corrections across cryptoassets. Contagion within the crypto sector has been substantial, reflected in further price drops of key crypto instruments and knock-on bankruptcies among service providers. Given low exposures by EU market participants, material spill-over effects of the crypto turmoil into the EU finance sector and the real economy have not been registered so far.