Earlier this week Fed Governor Jerome Powell gave an interesting speech at the Clearinghouse annual meeting, “Central Clearing in an Interdependent World”, addressing expanding central clearing for repo.

Governor Powell began by taking stock of the progress in central clearing of OTC derivatives. He was pragmatic, saying that central clearing has brought some order to the markets, but it is not perfect. There is still work to be done on stress testing, resolution, margin, and waterfall design.

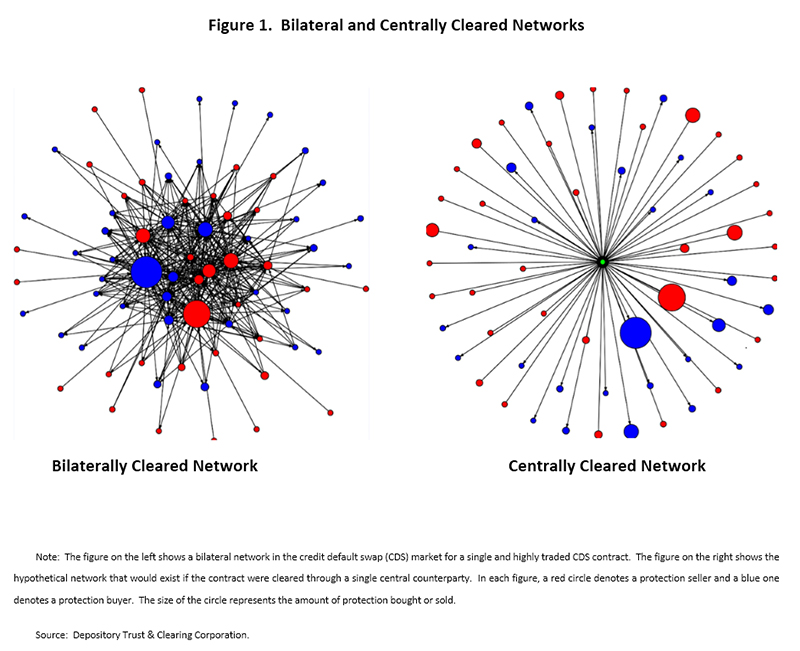

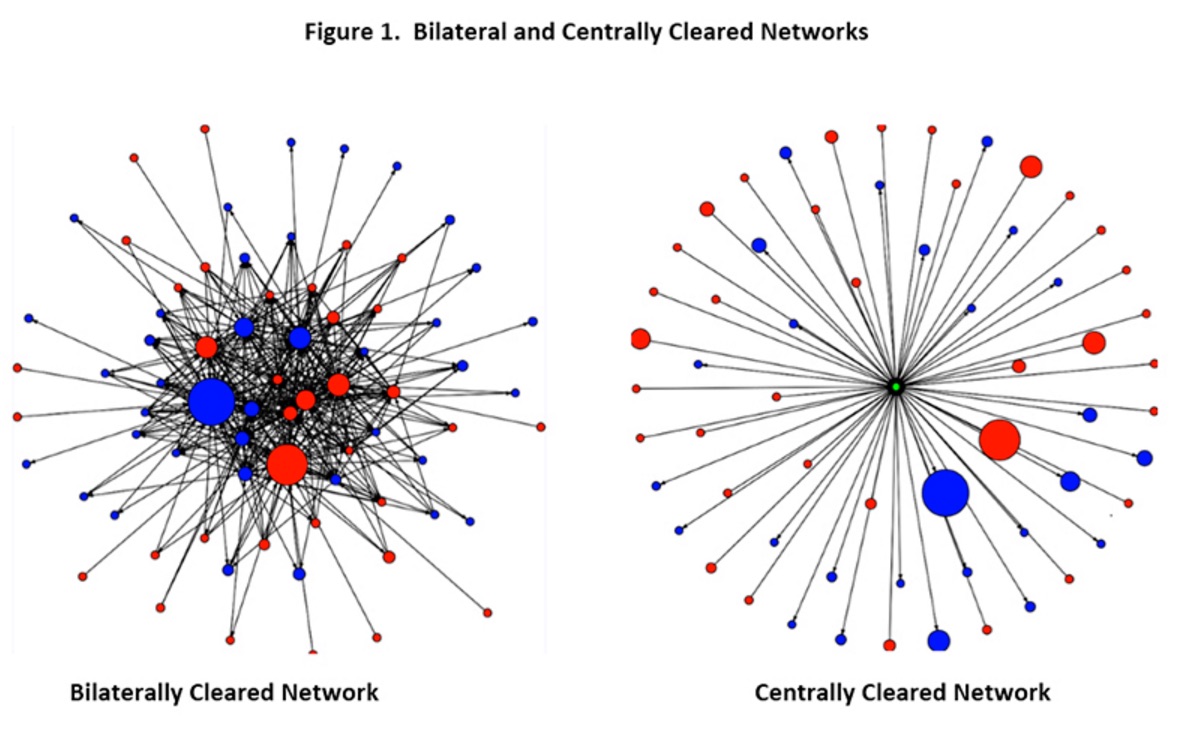

“…I am a believer in the potential benefits of central clearing under the right circumstances. But central clearing is not a panacea. Charts similar to that in Figure 1 are often used to illustrate the netting of exposures and simplification that central clearing can bring to an OTC market. The tangled and highly opaque picture of a purely bilateral market is replaced by the neat hub-and-spoke network in which a CCP is buyer to every seller, and seller to every buyer, allowing netting and greater transparency for participants and regulators alike. Of course, reality is not so elegant…There are multiple CCPs, even within product classes, and major dealers act as clearing members across a broad network of CCPs…”

{kind=link}

Source: http://www.federalreserve.gov/newsevents/speech/powell20151117a.htm#f5

Specifically talking about repo, Governor Powell said:

“…One area where market participants are actively searching for new business models is the repo market, where there are currently several private initiatives for greater central clearing. Expanded repo clearing could potentially bring a range of benefits, including greater opportunities for netting and related reductions in balance sheet costs for dealers affiliated with a bank holding company. The evolution of repo markets and central clearing can serve to illustrate both the potential benefits and the complexities that arise as the market seeks new infrastructure models…”

Fire sales and repo continue to be on the Fed’s radar. The near-elimination of the unwind/re-wind by the clearers has meant that cash lenders are exposed for longer. In a dealer default scenario, the result will be cash lenders ending up with collateral they need to liquidate quickly, creating potential fire sales. Powel argued that central clearing would mitigate fire sales.

“…CCPs have rule-based processes to dispose of the portfolio of a defaulted member. CCPs can transfer positions to solvent broker-dealers, or hedge positions and auction them off over time…”

A CCP liquidating securities would be transparent to the market, although it is also a guarantee that markets will collapse in anticipation of the sales. If CCPs opt to hedge the exposure and ride out the storm, there must be a robust source for liquidity and enough capital to absorb markets continued deterioration and/or the hedges not working perfectly (which is more likely for illiquid paper). Mutualizing the risk by moving the positions (and hedges) to surviving clearing members diffuses the problem, but it does have the potential to make the problem systemic.

As an aside, we have never understood why regulators have not told cash lenders in tri-party repo that if they can’t invest in the collateral outright, that they should not take it as collateral. It presents a big systems issue, but it would eliminate the pressure to liquidate paper instantly.

Powell noted that repo CCPs would allow for greater transparency and a reduction in operational risk.

“…CCPs are in position to aggregate trade information from all clearing members, and thus to monitor and manage counterparty and market-risk exposure better than individual members…”

Data collection would be a lot easier in a repo CCP, but there is still a lot of leakage that needs to be accounted for. Understanding what the data tells regulators is no easy job, full of all the problems of “big data”. As far as reducing operational risk, remember a CCP is one gigantic “single point of failure”. Just sayin’.

Powell made an interesting observation on repo netting opportunities. It sounds like he was skeptical of netting in CCPs being a panacea to dealers looking to expand their footprint after recent market contractions. He noted that one-way clients don’t help much for netting. However, we would note, that if those client flows were centrally cleared, the story might change.

Also on netting, Governor Powell discussed adding RICs or hedge funds to central clearing schemes. But the reluctance and/or outright inability to be part of risk mutualization puts that at risk. We know that some of the ideas bouncing around (FICC, for example) as well as existing CCPs that allow non-dealers (Eurex) also eliminate mutualization… but there is also a lot of reluctance.

“…Further gains in netting could arise if clearing expanded to the bilateral market or if some of the larger end users in the tri-party market, for example money market mutual funds or hedge funds, were able to gain access to the CCP. This could pose its own complications, however, as some of these institutions may be unwilling or legally unable to engage in the risk mutualization that exists in most clearing models…”

What makes repo CCPs a challenge? Governor Powell hit the nail on the head:

“…In repo trading, unlike in swaps, the full notional principal amount is exchanged at the beginning and end of the trade. As a result, the liquidity requirements for repo clearing will be quite high…”

Don’t get us wrong. We think that more SFT CCPs are coming and they will be an overall positive for the market. But like we wrote in our post “Derivatives, Securities Financing and the Law of Conservation: Transforming Counterparty Risk into Liquidity Risk”, November 3, 2015, “regulation doesn’t eliminate risk; it simply moves it into a different form”.

1 Comment. Leave new

It is time for the Fed to take a leadership role in getting the industry to begin the collaborative effort to develop a structural solution to lessening the risk of the two bank tri-party clearing model. The Fed always waits for the “street” to develop the innovation that evolves the market infrastruture to the next level but in the case of repo CCPs the Fed needs to get more aggressive in guiding the street to the next level as they are the lender of last resort. While Dodd-Frank buffers the Fed from lending to bail-out a failing institution but section 13(3) of the Act is still an active part of what allows the Fed to provide liquidity in a crisis. I think Gov Powell’s speech is a game changer in an effort that needs broad support.