In a recent staff working paper, researchers from the Federal Reserve examined the financial stability risks and benefits of issuing a central bank digital currency (CBDC) under different design options.

Among the observations, researchers noted that nonbanks may find it more expensive to raise secured wholesale funding should investors find that CBDC offers a more attractive safe investment, inducing nonbanks to turn to other, potentially more fragile, sources of wholesale funding.

The implications of this shift may not be prohibitively high during normal times. Yet, it can have an adverse effect on financial stability if institutions enter a crisis with a higher share of runnable liabilities.

They also wrote that a permanent shift of funds from deposits to CBDC may require banks to rely on riskier or more expensive wholesale funding markets to a greater extent than they currently do. A greater reliance on wholesale funding relative to deposits could increase the cost of funds to banks.

In turn, banks may increase their lending rates, affecting credit availability across the economy. As a result, the introduction of a CBDC might restrict banks‘ ability to extend credit, resulting in either a reduction in overall credit or in disintermediation of the banking sector.

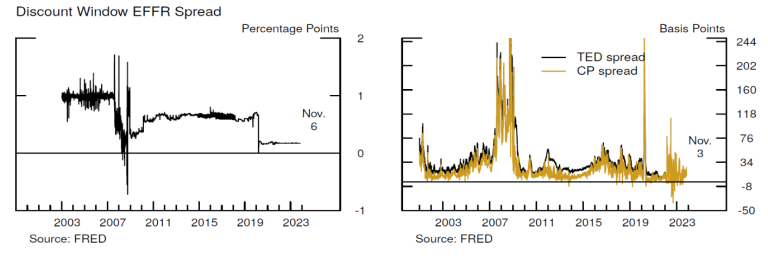

“Banks that experience a loss of their deposits to CBDC during crisis have a set of options to substitute for lost funding. For example, they could resort to the discount window or turn to secured or unsecured wholesale funding markets,” according to the paper.

Researchers consider three scenarios:

Researchers consider three scenarios:

- In the first scenario, banks borrow from the discount window at an extra cost of about 50 basis points, which is the conditional mean during crisis periods in the last two decades.

- In the second scenario, banks make up for their lost deposits with various types of wholesale funding, with an average additional cost of about 100 basis points.

- In the third scenario, banks substitute lost deposit funding with unsecured wholesale funding, reaching an additional cost of funding of about 250 basis points, which is the upper end of the historical realization during the 2007-2009 financial crisis.