The financial services industry’s reliance on tri-party as a utility for facilitating operationally intensive transactions has grown in both geography and product diversity. This in turn increases the need for awareness about tri-party operations and market trends. The global tri-party market size is US$6.15 trillion, up from US$4.65 trillion in 2017, according to Finadium’s new tri-party survey.

This Finadium report is a due diligence inquiry into the size, scope and functioning of tri-party providers covering ASX, BNY Mellon, Clearstream, Euroclear, J.P. Morgan and SIX. The report presents results of a proprietary survey conducted by Finadium in January 2021. The topics covered were market size, product diversity, collateral held, operations, how fees are assessed, and questions on trends including: the growth of blockchain; the impact of China; and demand for the pledge model and UMR-related services.

The report is useful reading for any participant in financial markets that utilize a collateralized trading product. While this was traditionally limited to repo and securities lending, the mandate of tri-party has expanded to include collateralization of other products that benefit from outsourcing back office processes. Cash and collateral providers including money funds and dealers, technology vendors, regulators and tri-party providers themselves may find the report useful for assessing the dynamics of tri-party operations in the context of a changing financial markets environment.

Tri-party and the pledge model

Asset managers, insurance companies and other buy-side firms have been an important part of the tri-party growth story. That information is played out in this year’s survey, with every TPA citing some segment of buy-side as an important one for driving tri-party growth in the last year. The sub-markets of growth are not uniform across TPAs however: some say that insurance companies have been paramount; some say central banks; while others note the crucial role of agent lenders reinvesting cash collateral or engaging in non-cash transactions for their beneficial owner clients in securities lending.

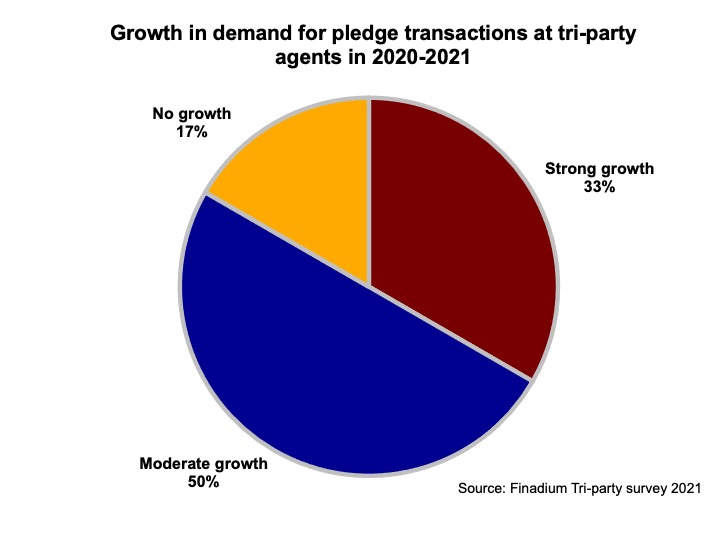

Most TPAs noted moderate to strong growth in demand for the pledge model in the last year (see Exhibit). According to the International Securities Lending Association’s (ISLA) guidance on pledge from February 2019, the model is well suited for TPAs, where “the Lender transfers ownership of the borrowed securities to the Borrower outright (as it would have done under the GMSLA 2010 title transfer version). The collateral provided by the Borrower is, however, not transferred to the Lender outright. Instead, collateral securities or collateral cash are transferred to the secured accounts and the Borrower grants security of the posted collateral in favour of the Lender.” The tri-party agent holds the collateral.

The growth of pledge demand fits tightly into the general growth story for TPAs with an emphasis on the buy-side. UMR is creating the demand for a large number of new account openings; a promotion of the securities lending pledge model in Europe with robust documentation is creating balance sheet cost reductions for banks, and a variety of other structured product types benefit as well. The combination of UMR, outsourcing and improved mechanics of pledge for certain market segments has been beneficial for the tri-party model.

A direct link for Finadium subscribers to the 2021 tri-party survey is https://finadium.com/finadium-report-desc/triparty-global-services-market-2021/

For non-subscribers, more information is available here.