Delta One and synthetic financing businesses continue to command attention at prime brokerage firms, the result of a complex web of regulations and client needs that direct business to these divisions. While some of the business is in OTC derivatives, other portions are in a growing segment of the listed derivatives market. Physical financing (securities lending and repo) still plays an important part but is smaller than it used to be. In this article I present the current state of the synthetic prime brokerage business and discuss an important new listed financing product where Societe Generale has taken a leading role.

The role of the synthetic financing desk

At its heart, synthetic financing remains the same business as always: it is a trading desk that facilitates client access to options, futures and swaps. Synthetics can be a supplement, complement or competitor to physical trading activity. In fact, synthetic desks themselves have traditionally been consumers of bank financing and a client of securities financing and repo desks on their way towards servicing hedge fund clients.

The recent growth of synthetics has been driven by capital regulations. This has resulted in steady growth for synthetic businesses over physical, but at the same time, there is a greater need than in the past for synthetic desks to create their own liquidity rather than using bank capital. Synthetic financing must be highly sensitive to on and off-exchange costs and optimizing netting opportunities; for every non-netted trade, a synthetic desk requires a physical or derivatives trade to hedge market exposure. This is a regular juggling act that is performed daily in order to minimize both client and bank costs.

The decision of whether to trade a derivative versus a physical is based on client preferences first and internal costs second. If a client is willing to pay the fee for a securities borrow on a hard to borrow stock and the market is liquid we will facilitate that trade at the best possible rate. We may find though that derivative markets offer better liquidity than underlying physical markets, or that the client prefers a derivative over physical financing for the built-in leverage that derivatives offer. In this case, we take the derivatives route. We want to offer our clients the most competitive access to financing; how they get there in the end is their choice.

Physical and derivative market trends

Recent market trends show the demand for synthetic financing over physical, which is a function of both market liquidity and the regulatory costs assigned to both products. The securities lending market currently has declined from US$1.8 to US$1.7 trillion outstanding over the last two years, including equity and fixed income products. Repo between banks and cash investors is also declining according to both US and European surveys. These declines are driven primarily by the costs assigned to these trades by Basel III and domestic regulations.

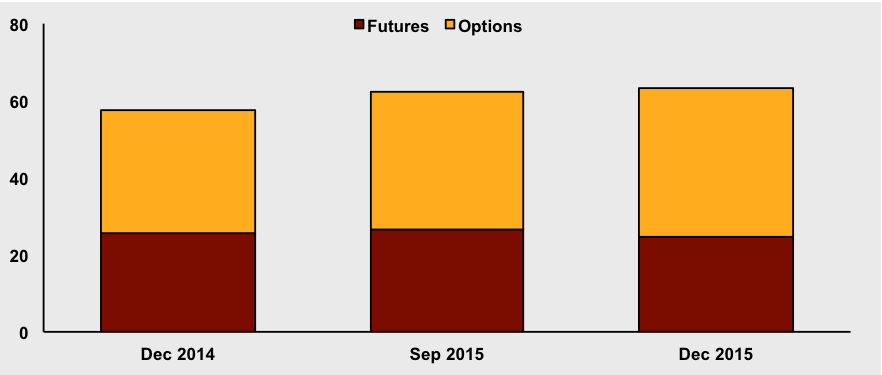

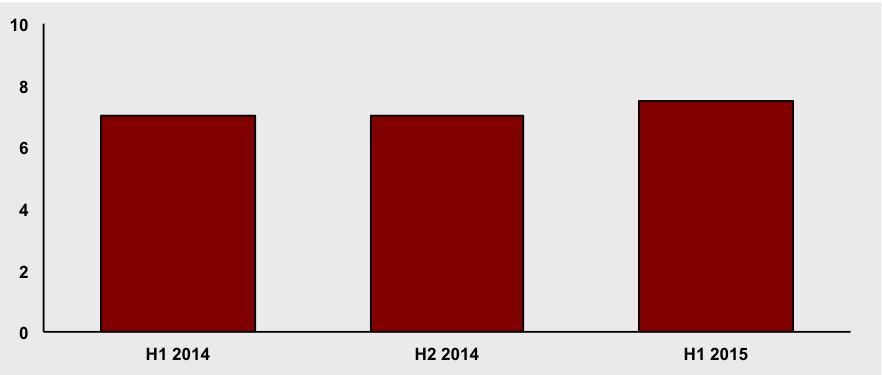

Meanwhile, open interest in futures and options markets globally ended 2015 at US$63 trillion and continues to climb (see Exhibit 1). While overall OTC derivatives markets have shrunk over the same period, this was due almost entirely to compression in the interest rate contracts space; equity-linked OTC contracts continued to grow steadily to US$7.5 trillion in outstanding notional as of H1 2015 (see Exhibit 2).

Exhibit 1:

Futures and options market open interest, Dec 2014-Dec 2015

(US$ trillions)

Source: Bank for International Settlements

Exhibit 2:

Notional amounts outstanding equity-linked contracts, H1 2014-H1 2015

(US$ trillions)

Source: Bank for International Settlements

The reason behind these figures is pretty clear: the costs to banks are lower for both listed and OTC derivatives products than for physical financing trades. At the same time, restrictions on bank proprietary trading, banks unwilling to commit capital to physical markets, and investor preferences all play a role. But in an even analysis, if our costs to cover stocks through futures trades are lower than to borrow a stock, we can pass on that cost reduction to clients. They in turn make the final decision how to trade.

New listed products for financing

We have been expecting for some time that listed derivatives products would grow in popularity as an alternative for physical financing. These products can take many names including Swap Futures, Single Stock Futures and repo index contracts.

In the US, the CME recently launched Basis Trade at Index Close (BTIC) futures. This product allows us a new way to trade and finance the S&P 500®, NASDAQ 100 and other indices by quoting our clients a basis (financing cost) on the underlying index referencing the index closing price. This allows clients to perfectly replicate the index close through derivatives (more) efficiently. Societe Generale has become a leading market maker in BTIC; traders can see quotes or enter block trades directly with our trading desk. This also permits us to internally cross the S&P 500® with the future and enter the futures trade on CME’s block trade facility. The guaranteed basis then locks in a financing cost for the duration of trade.

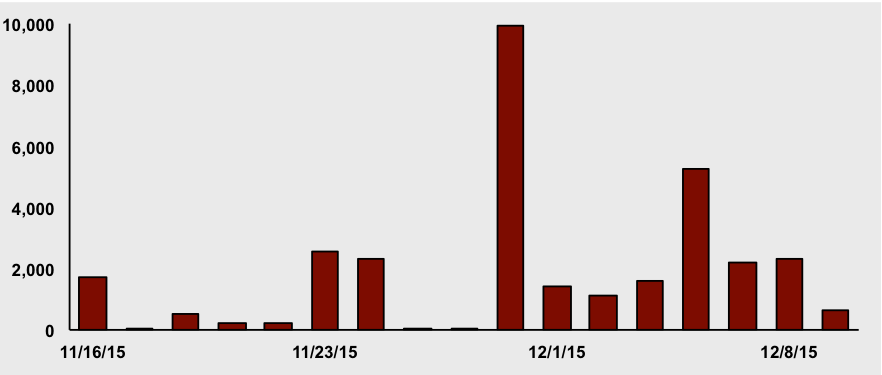

These BTIC contracts have experienced strong interest since their launch with some days of very high usage. At their peak so far, round turn volume has been almost 10,000 contracts with the second highest day at 5,000 contracts (see Exhibit 3). Most days have been closer to 2,000 contracts. Even so, this is a very good start for any new product launch especially at the end of the calendar year.

Exhibit 3:

Volume (round turn) on BTIC on E-mini S&P 500 (symbol: EST)

Source: CME Group

The CME has also launched futures on listed index dividends. While not as critical for our business as the BTIC futures, they nonetheless provide more flexibility for clients to gain exposure to dividend payments than the underlying physical S&P 500® Annual Dividends Index and the S&P 500® Dividend Points Index indices.

Also in the US, our trade volume of reverse conversions in options to generate financing doubled in 2015 from the previous year. In this trade, the client sells a put and buys an option, creating a synthetic long position. This generates cash for the client to use in other trading strategies. This has been a very convenient trade for hedge funds and small proprietary trading firms.

While listed products may seem like they are taking over, and this may be true for firms needing short-term financing, the opposite is happening when clients need longer-term financing. The problem is that traditional strategies that relied on financing in the futures markets are no longer viable as futures indices roll over at expiration periods. Investors have found that liquidity is too volatile at the roll since market makers (mostly banks) do not want to finance the rolled (physical) index positions and market flows may be unsteady. A sudden lack of liquidity decreases the certainty of financing at a preferred rate and makes this trade very unattractive. As a result, some investors are returning to traditional swaps to lock in financing rates of up to one year. Clearly, the benefits of the liquidity guarantee at a higher cost outweigh the low cost of the futures trade with no certainty that liquidity will be available.

Delta One and synthetic financing businesses continue to be an effective means of helping clients achieve their financing objectives. As limited balance sheets become more of a daily fact of life in financial markets, creating derivatives strategies using listed and unlisted products become more important. While physical financing will always have a role in financial markets, we expect that 2016 will see increased growth and additional product opportunities in the synthetic financing space.

Salim Nemouchi is Head of One Delta Swap Trading, Prime Services, Societe Generale.