The Financial Stability Board (FSB) published the final report on its evaluation of the effects of too-big-to-fail (TBTF) reforms for systemically important banks (SIBs). The evaluation examines the extent to which the reforms have reduced the systemic and moral hazard risks associated with SIBs, as well as their broader effects on the financial system.

The evaluation finds that TBTF reforms have made banks more resilient and resolvable, and that they have produced net benefits to society. Indicators of systemic risk and moral hazard moved in the right direction, suggesting that market participants view these reforms as credible. Increased bank resilience and greater market discipline have been tested by the COVID-19 pandemic. However, banks – thanks also to the unprecedented fiscal, monetary and supervisory support measures – have so far been able to absorb the shock.

Nevertheless, the evaluation finds some gaps that need to be addressed:

- resolution reforms should be implemented in full to enhance the feasibility and credibility of resolution, minimizing the need for state support of failing banks. This includes further work to enhance the resolvability of SIBs.

- there is still scope to improve public disclosures of information relating to resolution frameworks and funding mechanisms, the resolvability of SIBs and resolution actions.

- information may be needed for public authorities to assess the potential impact of resolution actions (such a bail-in) on the financial system and the economy.

- The application of the reforms to domestic systemically important banks warrants further monitoring. In addition, risks arising from the shift of credit intermediation to non-bank financial intermediaries should continue to be closely monitored.

Claudia Buch, vice-president of the Deutsche Bundesbank and chair of the group that produced the report, said: “Having robust banks and a mechanism to resolve them in the event of failure is key to maintaining financial stability. While the evaluation highlights the progress we have made, more can be done to fully realize the benefits of these reforms. I look forward to further work by the FSB and standard-setting bodies to close the gaps we have identified”.

Funding cost advantages

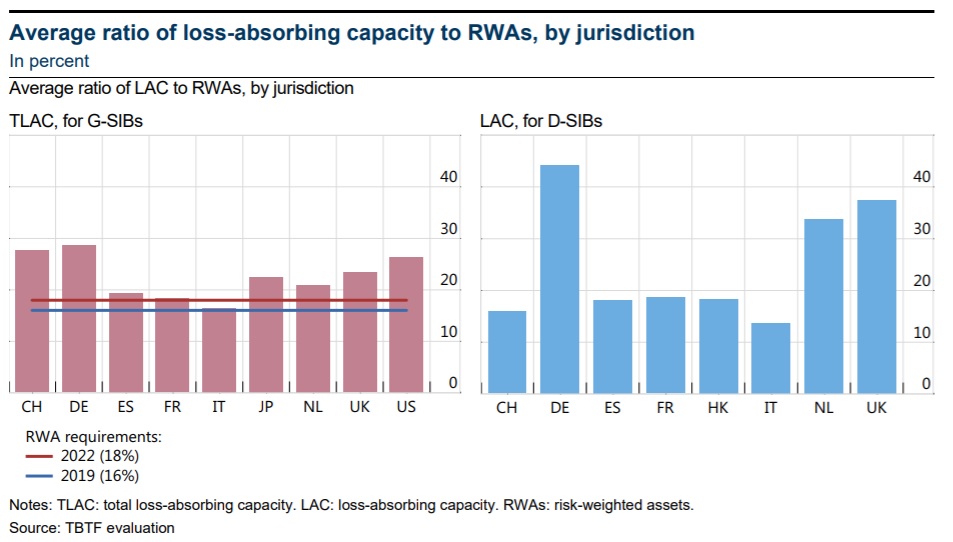

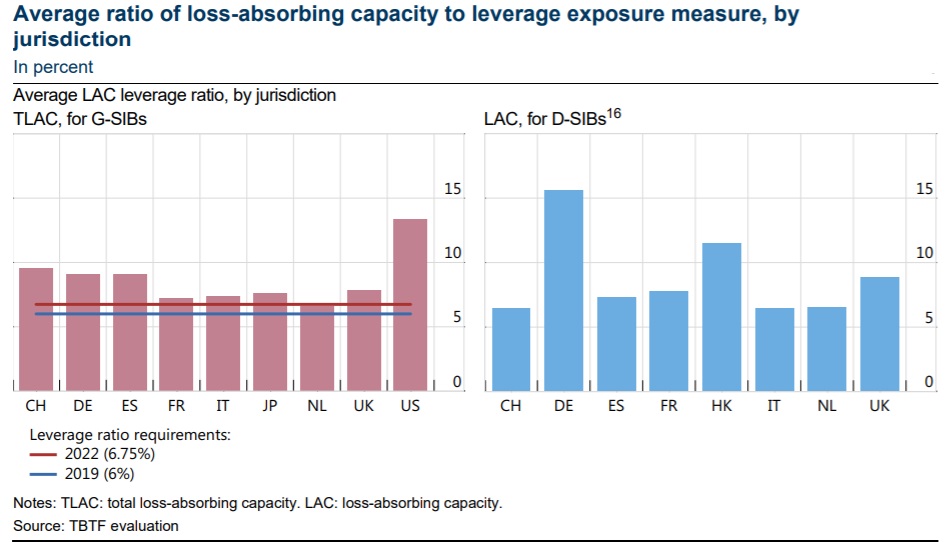

The evidence suggests that the funding cost advantages of SIBs have declined since TBTF reforms were implemented in 2012 but remain higher than before the global financial crisis. These results broadly suggest that reforms may have been effective in reducing subsidies. However, in spite of the reduced funding cost advantage in the reform implementation period, the average post-crisis funding cost advantages have not fallen below their pre-crisis levels. Moreover, the average funding cost advantages in the reform implementation period are not consistently below their pre-crisis average in all studies.

The evidence also suggests that the credibility of resolution reforms has risen. Thus, the funding cost advantage of SIBs is lower in jurisdictions that have implemented resolution reforms more fully. Credit rating agencies have removed or significantly reduced sovereign support uplifts for G-SIB ratings in a number of jurisdictions since the introduction of resolution reforms. Funding cost advantages and sovereign support ratings of SIB holding companies have decreased relative to their operating subsidiaries, suggesting that bail-in has become more credible.

Finally, there is some evidence that resolution reforms have improved market discipline. Other factors influence funding cost advantages, without affecting their general pattern of evolution. These factors include macroeconomic conditions, the size of the banking sector, the stance of monetary policy and investor uncertainty. The funding cost advantages of SIBs tend to be lower in countries where sovereign risk is higher and the share of the banking sector is lower. They are also lower when interest rates and investor uncertainty are lower.

Increased credibility and the associated benefits have not been uniform. In spite of the positive association of reforms and reductions in the funding cost advantage, the results vary across countries. Jurisdictions that have progressed further in enacting the reforms see bigger reductions in SIB funding cost advantages.

Inadequate disclosures may be limiting market participants’ understanding of how they may be exposed to loss in resolution, which in turn, may impair market discipline. Increased transparency is not, however, costless and the disclosure of otherwise confidential information may create the potential for adverse market reactions and consequences in resolution.

Disclosures should not constrain the ability of the resolution authorities to choose the approach that best supports orderly resolution in the circumstances. Nevertheless, there may be opportunities to enhance credibility of reforms by enhancing disclosures of information relating to the operation of resolution frameworks and funding mechanisms. The appropriate level of transparency is the focus of ongoing work by the FSB and member authorities.