The Financial Stability Board (FSB) published a report on implications of leverage in non-bank financial intermediation, which forms part of that work by providing an overview of aggregate nonbank financial intermediation (NBFI) leverage trends across FSB jurisdictions. It’s also developed a comprehensive work program to examine and address vulnerabilities, including those associated with NBFI leverage that contribute to systemic risk.

The report also discusses the vulnerabilities associated with NBFI leverage, including propagation and amplification mechanisms; looks at aggregate trends in NBFI leverage through a set of metrics; discusses hedge fund leverage and the links with prime brokers; covers leverage, liability-driven investment (LDI) strategies, and long-term investors; and describes the data gaps that lead to hidden leverage.

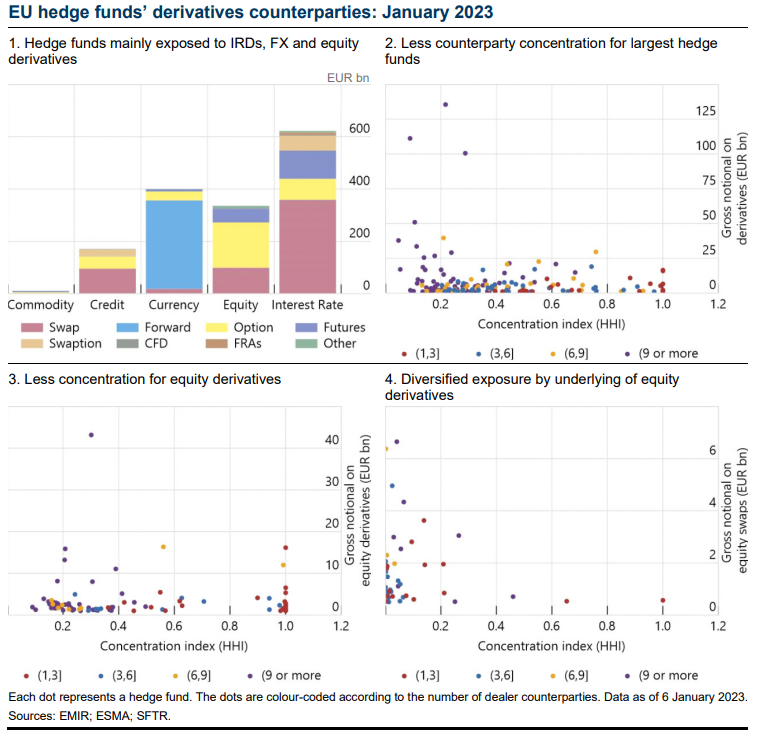

The connections between hedge funds and prime brokers are composed of derivatives transactions and securities financing transactions (repurchase agreements and margin lending in particular). This set of relations is complex and, therefore, a single prime broker might not be aware of the linkages of its clients with other prime brokers (and other entities). In some jurisdictions, public authorities may be able to estimate the network from supervisory data, although there are significant operational challenges in merging different datasets, according to the report.

The report includes a case study that looks at the counterparties of EU hedge funds in derivatives, repo and securities lending markets, and concludes with policy implications of the work that authorities could consider.

Among the policy recommendations, the FSB said that members could consider accelerating efforts in implementing the agreed FSB minimum standards and haircut floors on non-centrally cleared securities financing transactions. Another issue to consider is whether rules on risk-based leverage ratios could be extended to financial institutions that are currently not subject to such rules. However, such work would be complicated by the challenges in identifying pockets of leverage, differences in leverage metrics across jurisdictions and the complexity and calibration across different types of non-bank investors, business models and investment strategies.

The report also highlighted “one area to explore”: whether prime brokers’ risk management of exposures to leveraged non-bank entities could be enhanced. The BCBS is planning to develop additional guidance for banks on their interconnections with NBFIs.

Measures could also be considered to improve prime brokers’ understanding of hidden leverage (e.g. through requirements for non-bank investors to disclose the full extent of their exposures to their prime brokers and through stress tests of prime broker exposures to non-bank investors). Another possibility could be to consider measures to abate the position liquidation channel and reduce internal liquidity imbalances in response to spikes in collateral and margin calls.