The other day we wrote in our post “Our analysis of the FSB’s securities lending and repo policy framework” about the FSB paper “Strengthening Oversight and Regulation of Shadow Banking Policy Framework for Addressing Shadow Banking Risks in Securities Lending and Repos”. Some of the FSB recommendations did not go as far as feared. But there are some in the paper which, if they become rules, could change the face of securities financing.

Re-hypothecation was discussed in the context of client assets. We should note that the FSB looks at re-hypothecation as a subset of collateral re-use. “…define re-use as any use of securities delivered in one transaction in order to collateralize another transaction, “’re-hypothecation’ more narrowly as re-use of client assets…” and “re-use of securities can be used to facilitate leverage…”

The problem comes when client assets are used. “…Client assets may be re-hypothecated by an intermediary for the purpose of financing client long positions and covering short positions, but they should not be re-hypothecated for the purpose of financing the intermediary’s own-account activities…” This squarely addresses the Lehman (Europe) problem of client collateral being lent out, but may also catch U.S. prime brokers who can lend out 140% of a client’s debit balance (Securities Exchange Act, Customer Protection Rule (Rule 15c3-3)). The FSB does not appear to be looking to preempt all re-hypothecation and we are certainly pleased about that.

Rather the FSB plans to attack the problem of complex collateral chains (that come from re-hypothecation) with a trade repository. The FSB recognizes the difficulty of this, especially the cross-border & cross bank / shadow bank nature of the task. It will be gargantuan.

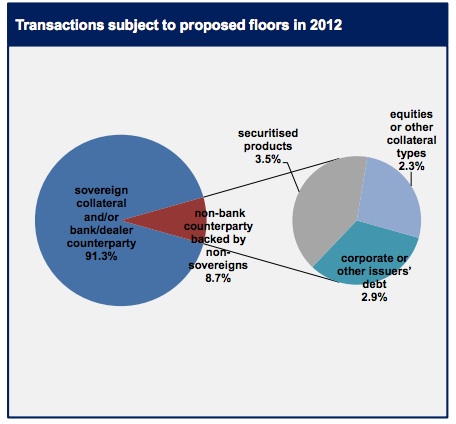

Minimum haircuts have made great sound bite in the press (we have done our fair share too). But the reality is that the FSB response is really tame. The minimum haircut proposal only impacts trades done between banks & broker/dealers and shadow banks on non-sovereign paper. The FSB calculates this to covers less than 10% of the market.

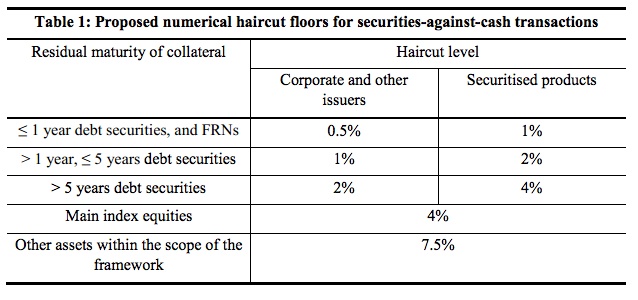

And what about those haircuts? Well, they look really low — especially if many of the counterparties are hedge funds. We mentioned the other day that some of these haircuts are even lower than those commonly found in tri-party funding.

Finally, in Recommendation 8, “Minimum regulatory standards for collateral valuation and management” the FSB says

“…Securities lending and repo market participants (and, where applicable, their agents) should only take collateral types that they are able following a counterparty failure to: (i) hold for a period without breaching laws or regulations; (ii) value; and (iii) risk manage appropriately…”

This sounds a lot like the FSB saying that tri-party cash lenders should only take paper they can hold onto following a default. This goes back to the Fed and avoiding fire sales – a popular topic on this blog. But managing that constraint is going to be a problem not only on the IT side, but also for the broker/dealers who will face problems financing their longer dated paper in tri-party with, for example, 2a-7 funds. If a fund can’t own, say, corporate bonds but still takes corporates in tri-party, this rule could bring that to a grinding halt.

A link to the FSB paper is here.

A link our earlier post of the FSB report is here.