Funds Transfer Pricing (FTP) is emerging as not just a nice to have, helpful tool in managing a financial services business, but in some cases has become a regulatory necessity. FTP, also called Collateral Transfer Pricing in some firms, is the exercise of allocating the cost of liquidity between business units at the same firm. It is no longer enough to have a friendly handshake about cost allocation, especially when one desk is providing liquidity and another is a high-octane consumer.

The new requirement is that a robust model be in place that can show all internal participants as well as regulators how costs are allocated and absorbed. While FTP started with capital market activities, the next evolutionary step is in expanding the concept to include money markets, repo trading and securities lending activities. FTP is a reflection of the fact that term liquidity has become a finite and scarce resource that is not easy to manufacture for capital markets.

A Brief History of the Problem

Before the financial crisis, neither FTP nor collateral optimization played much of a role in financial institutions. The traditional model was that Treasury or an Asset/Liability Management department would match up both sides of the balance sheet. The Treasury team would link illiquid loans on the one hand and retail funding plus an equity component on the other hand, making trades to balance the difference and consider the matter closed. There was often no explicit cost of liquidity or collateral consumption to any trading desk, and certainly trading desks were not paid if they were net contributors to the overall collateral pool.

The traditional Treasury did not really understand the capital markets concept that can easily separate legal and economic liquidity mismatches, both on the asset as well as on the liability side of the balance sheet. This is in a way remarkable as exactly this mismatch is considered to be the Achilles heel of any deposit based banking system. But Treasury managers were not looking beyond banking deposits.

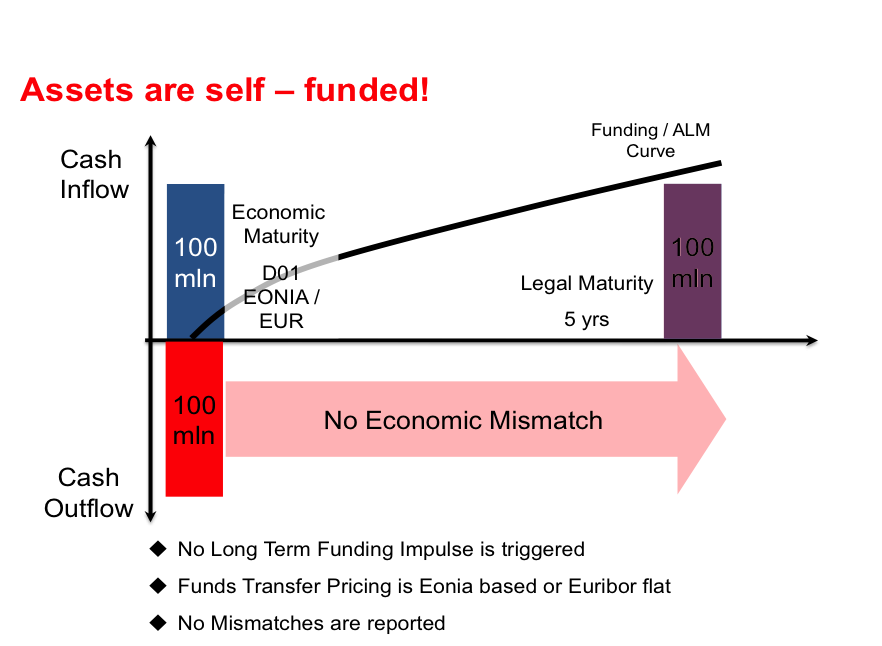

To illustrate the nature of the problem, we take an example of how capital markets assets were measured at the time. While the purchase of an asset causes a €100 million outflow and produces a legal mismatch of, say, five years, it does not show up with this mismatch on the liquidity radar screen of a treasury department (see Exhibit 1). The reason for this is that assets could be funded any day in the repo market, exchanged in the securities lending markets, or sold without a great loss under the assumption that there is ample liquidity and value at risk is relatively small.

Exhibit 1:

The pre-crisis view on capital market assets

Source: DekaBank

As a consequence, the outflow is 100% neutralized with a cash inflow and the mismatch disappears. The asset is now self-funded. Correspondingly, with no mismatch on the radar screen of the treasury and no long term funding impulse, there was a fair argument that a trader should only pay the repo rate as FTP or pay no more than EONIA / EURIBOR flat or equivalent based funding. This was all fine with high quality assets in very liquid markets, but might have gotten more complicated with less liquid securities. In essence the underlying assumptions were ultra-liquid assets, in ultra-liquid markets where neither market, nor funding, nor macroeconomic liquidity risk existed.

Moving closer to today, a laundry list of factors has emphasized the importance of FTP and collateral optimization and the technologies that accompany them. The factors we include are: recent regulations; balance sheet deleveraging; the increasing role of central clearing and CCPs; regulatory and central bank demands for transparency; internal auditors; and even internal trading desks when confronted with their funding costs. These have all increased pressure on Money Market, Treasury, repo, securities lending and collateral management departments to improve transparency on pricing and bring more rigour to their allocation methodologies.

Part of the new pricing paradigm are haircuts. While most people only had a limited understanding of haircut calculation before 2007 / 2008, today we find all kind of haircuts: central bank haircuts, LCR or NSFR haircuts, large exposure risk haircuts, VaR and gap risk haircuts, FSB haircuts, stressed and going concern haircuts, etc. Haircut calculations have become an art in itself and are an important driver of FTP or collateral optimization as they are used to inject longer term funding impulses into security positions, repo or securities lending and even structured or derivatives transactions.

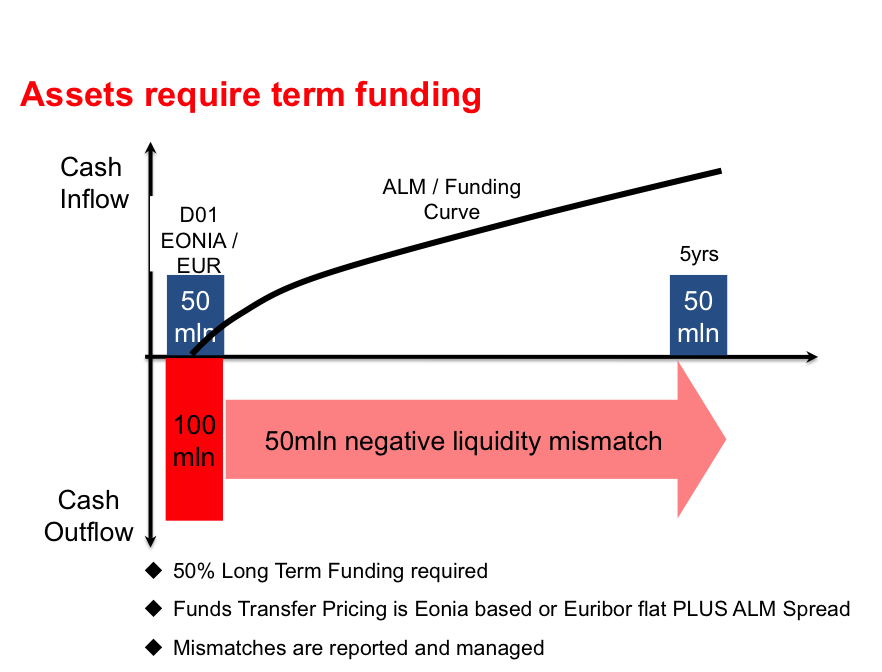

Taking the same example from above, this trade is not only not self-funding, but it generates a strongly negative funding position (see Exhibit 2). Less liquid credit assets like NIG rated ABS, CLO’s, CDO’s or third tier equity, etc. now have a much more limited funding value. In this example they attract a 50% haircut. And what is more, this haircut gives rise to a €50 million negative liquidity mismatch, which shows up on the mismatch radar screen of the treasury and creates a long term funding impulse. With the cost of funds at 50%, a five year Asset/Liability Management curve and only 50% EONIA/market-based funding, it is obvious that the cost of liquidity has increased significantly for the holder of such a position. Accordingly, the trading position or instrument is not self-funding any longer.

Exhibit 2:

The post-crisis view on capital market assets

Source: DekaBank

Now, this would probably not be such a big issue if we had long term repo- or long term securities lending markets that would be able to manufacture term funding liquidity at reasonable cost. But currently, more than 80% of the securities lending and the repo markets are less than one month duration and offer no means to close negative funding mismatches in later time buckets.

As a consequence, haircuts have partially eroded the market and asset based funding system. Capital markets activities are now a term funding drag for the bank and are in competition for term liquidity with both, internal and external actors. Investment bankers are back to the negotiation table with the treasury department. In order to keep these negotiations from getting too unwieldy, a fair and transparent FTP methodology has to be implemented.

The Practice of Funds Transfer Pricing

FTP is the practice of allocating funding costs fairly across all parties. It is at heart a governance matter, ensuring that liquidity givers and takers are each compensated for their actions. As a governance process, FTP has four parts:

- Liquidity Management

o Transparent liquidity reporting

o Make mismatches transparent

o Improve liquidity planning

o Ensure compliance with regulatory liquidity ratios

o Allocate cost of liquidity

buffers - P&L Management

o Determine P&L after Funding Cost

o Manage Funding Cost at Desk / Unit Level

o Determine Fair price for firm Liquidity - Balance Sheet Management

o Ensure efficient balance sheet utilization

o Help determine cost of balance sheet utilization - Pricing

o Determine fair transfer pricing between liquidity providers and liquidity users

o Determine correct LVAs for derivatives

o Ensure transparent liquidity prices

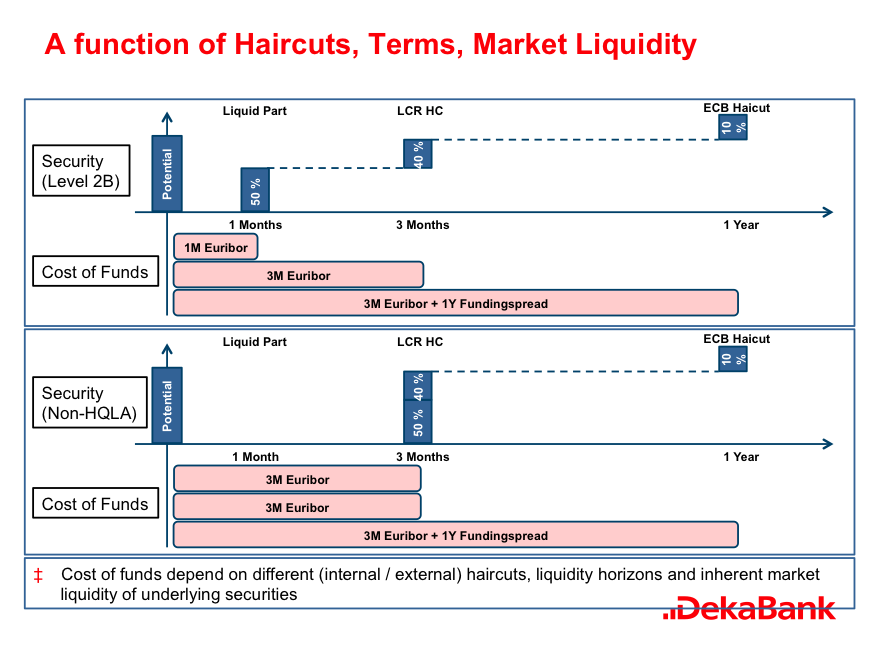

The hardest piece of FTP is actually figuring out how the pricing methodology occurs. Some firms have turned to market-based funding rates (repo and securities lending) while others use a haircut methodology. Some firms use a combination including taking haircuts from multiple internal and external sources. A 2014 white paper by SunGard, Finadium and InteDelta described a methodology for finding the fair value of an asset for FTP. With this collection of methodologies, it would come as no surprise that the FTP values across security types are a complex function of haircuts, funding and market liquidity and regulatory requirements (see Exhibit 3).

Exhibit 3:

A practical outcome of FTP for securities

Source: DekaBank

The exhibit shows an example for a level 2B security and a non-HQLA security. FTP decomposes any security position into different buckets of varying liquidity. The ultra-liquid parts may still be self-funded and attract a short term repo rate. The less liquid parts of a security position attract a higher portion of term money and thus higher costs of funding. In the below example, the Level 2B security attracts 50% funding at the one month bucket. The LCR haircut attracts funding at the three-month (internal or benchmark) rate, reflecting the fact that in order to neutralize the LCR impact you need longer term funding than just one-month. Eventually, there is also a longer term component (in this example illustrated by the ECB haircut), which attracts a one year funding impulse.

As can be seen in the exhibit, the non-HQLA asset attracts even 90% 3- months funding. The respective funding rates for the one, three or 12 months buckets may depend on the mix of funding instruments and access to funding markets for a certain institution (e.g. money market / deposit based funding, access to repo, CP, securities lending markets and other factors). It may be based on benchmarks like EONIA, EURIBOR or a mix of all the above. The methodology as outlined is relatively robust. As regulators inject even more long term funding impulses, e.g. through the NSFR, the methodology can be easily adopted.

Once you have proper funds transfer pricing for different collaterals as outlined, it is easy to construct FTP for repos by just adding or subtracting the term cash legs to the collateral leg. FTP for securities lending can be derived by adding / subtracting the FTP for the two collateral legs, or if that is easier and more direct by adding a repo and a reverse repo. As a consequence, you will have covered short term products in a straightforward, simple and transparent methodology that is both robust and flexible with regard to new requirements.

Regulators have made term liquidity both an essential as well as a finite resource of capital markets activities, despite the cash overhang created by QE in different parts of the world. This happened through simple measures like the de facto introduction of haircuts through of the LCR, NSFR, or by making it more difficult for beneficial owners to lend on term. As a consequence, costs of funds went up and financial institutions had to deleverage their balance sheet.

The Quest for Term Funding

The question is whether capital markets can create new sources of term funding to mitigate these effects. Repo CCPs may be a good starting point, however, with the exception of ultra-liquid government securities, which are self-funded anyway, term markets have not really developed there. Also, establishing term markets on a CCP is not a straightforward task. CCPs can change the collateral composition and counterparty risk requirements pretty much overnight, thereby invalidating the term nature of any transactions immediately. We are now discussing LCR baskets, but this is just an exchange of HQLA vs cash and will not do anything to generate term liquidity. Hence, what is good for systemic risk may be counterproductive for the development of secured term repo / securities lending markets. Bi-lateral transactions do work of course, but are not as balance sheet or capital effective as CCP transactions. That said, there have been some new ideas with regard to constant maturity type transactions recently. Eventually, term funding may be forthcoming from the shadow banking sector, but would this be in the interest of regulators and central banks?

Final Thoughts

Regulators as well as central bankers need to understand that by manipulating funding relevant haircuts (for instance by introduction of regulatory ratios like the LCR and NSFR), they can increase or decrease capital markets activity, respectively funding and market liquidity. Haircuts and market based funding levels are different sides of the same coin determining the internal and external cost of funds. Haircuts that are too high will exert funding pressures despite QE and prohibit market liquidity. Haircuts that are too low may lead institutions to leverage up their activities too much and add to too much credit sensitive assets to their trading books and balance sheets. Here, regulators and central bankers have some fine tuning to do.

Against this backdrop, FTP has become a requirement for any bank and capital markets division today. It is vital to have a fair and transparent methodology that allocates costs amongst liquidity givers and takers, thereby allowing institutions to price transactions according to their internal and external costs of funds. And here, banks have some optimization to do in steering and managing the supply of term liquidity that central bankers and regulators have allowed into the markets.

Michael Cyrus is Head of Short Term Rates at DekaBank.