GLMX has a front row seat for observing how financial instruments are digitalizing and the way that market structure and participants are adapting to electronic trading across front-end interest rate-related products. We speak with Glenn Havlicek, chief exec of the securities financing execution platform, about the swelling volumes and shake-up of traditional liquidity channels as the market passes a tipping point.

Securities Finance Monitor: We hear there’s a lot of growth in use of GLMX’s trading platform – how specific can you get about your traction and volumes?

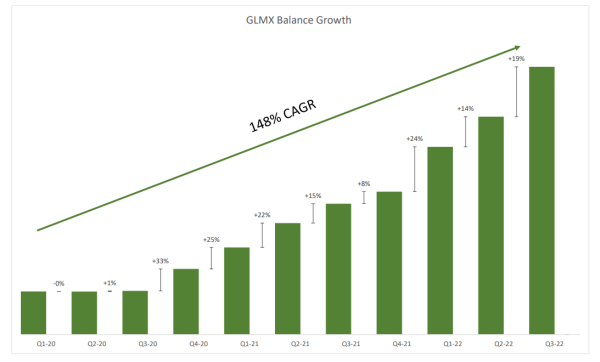

Glenn Havlicek: We had some reasonable traction at end-2019 and beginning of 2020, and then the pandemic kicked in. Everybody was confused, there was a risk-off scenario and so we saw a little bit of a dip in volumes.

But then people realized that this was not going to be a one- or two-month thing and frankly, an integral function like financing needed to continue and so we saw a dramatic uptick in activity from March 2020. We’ve been growing on the order of 150% compound average growth rate since then.

Our daily volume varies depending on market conditions but has been well over $300 billion recently, with robust growth across all types of collateral. In addition, our geographic footprint continues to expand, and now almost half of our volume derives from UK/EMEA.

SFM: Digitalization is one of those buzz words that can have different meanings – what does it mean in your context?

GH: We’ve all heard the story about the US stock market’s genesis under the Buttonwood tree on Wall Street in the 18th century. Why there? Because that’s where the liquidity was. The only thing that’s changed today is the available technology: markets are still fundamentally about the search for liquidity because people want to be able to get things done at the best price with the easiest access.

In the 20th Century, markets moved into a more modern era of telephones and messaging systems, and then email. So, when I say digitalization, I mean that today’s technology can replicate the style and quality of communication provided by phones and messaging, with nearly identical flow, more efficiency and with almost no risk of communication errors.

When we set out to build GLMX’s technology, the first thing we did was to roleplay various participants in the marketplace. In doing so, we confirmed our premise that we could provide the same ‘feel’ to negotiation and execution with the added value of equal and ultimately superior access to liquidity.

Said simply, people – still the enduring core of financing markets – are able to do their jobs more effectively, enabling scale without comprising quality

SFM: How does that translate to GLMX’s tech development for repo and sec lending?

GH: In the early days of GLMX, our clients asked us for basic execution technology because being able to negotiate and execute efficiently with a wide array of counterparties in an environment of near-zero, stagnant interest rate markets and resultingly smaller teams was nice to have. Fast forward, in a world of remote work, massive sovereign debt loads and rapidly rising rates and volumes, the use of technology which digitally replicates the full array of secured financing flow – things like re-rates, open trades, collateral substitutions, to name a small fraction – has become an imperative.

Repo and securities lending are demonstrably different from buying and selling securities: there’s an on leg and an off leg, and there are mid-life events. For example, we see massive spikes in activity on our platform the day of, or the day after, central bank rate changes. These rate modifications used to be done manually. But doing so for thousands of mid-life events on a given day is an unnecessary and unmanageable burden, especially when presented with an easy-to-use alternative.

Under those circumstances, people have come to appreciate the power of GLMX technology. In a manner of speaking, once people realized that basic functionality worked and that there was sufficient liquidity on the other side of the system, they began to ask for functionality which streamlined and de-risked their entire workflow.

SFM: Repo markets are often considered a laggard for adopting tech. Where do you think things are at for repo getting “digitalized”?

GH: Our CTO, Ilia Mirkin, is a brilliant guy with an MIT double master’s in physics and computer science. A few years ago, we started to get some traction on the platform, and he said: “Pretty soon we are going to have built all of the functionality that exists for repo.” Now, he realizes there’s a lot more to do.

GLMX has delivered the majority of the repo functionality that people use – like reprice, rerate, substitutions, evergreens, callable trades, open trades. But there are ongoing tweaks for specific functionality. We’ve recently introduced “one cancels other” for example, which is when a client is looking to do a variety of funding trades: they execute on one and they immediately want the other orders canceled.

There’s a virtuous cycle that comes with the “new” digitalization of a market – once users become comfortable with the basics, they find many uses for technology which nobody has thought of before. That’s fun for us.

As an example, now that GLMX has made negotiation and execution much more efficient, clients are increasingly focused on how technology can have a similar impact on other parts of the trade lifecycle – digitizing more of the pre-trade and post-trade workflow as they look for a seamless integration of trade decision support, execution and settlement.

SFM: Beyond repo, you are also executing securities lending, how is the traction there?

GH: We are deeply engaged in developing for the securities lending space, particularly in fixed income, and we are in the heart of building out functionality for our clients. We work with several of the major sec lenders, and they tend to focus on discovering liquidity as distinct from accessing liquidity, so we are working to define exactly how that distinction manifests itself in the real world.

Sec lenders are, along with money market mutual funds, the poster children for GLMX’s original, ongoing and ultimate view that an array of global short-term interest rate markets form one, massive, integrated marketplace. That marketplace includes participants – asset managers, securities lenders, hedge funds, broker dealers, banks, money market mutual funds, corporates, sovereign wealth funds, insurers, pension funds, prime brokers – and products – securities lending, repo, time deposits, CDs, commercial paper, government and agency debt, total return swaps.

And those participants all are seeking some variant of the same liquidity pools. We’re building a single, digital interface to all those markets. In that vein, Sec lenders are a great proving ground for the GLMX premise above as they often raise cash by lending securities and reinvest that cash into other money markets.

I was responsible for wholesale liquidity management at J.P. Morgan Chase for 22 years. From the start, I found those short end markets highly and unnecessarily fragmented. The real question has always been: how do we get from fragmented to unified? The simple but excruciatingly difficult-to-execute answer is: by combining a critical mass of users and highly capable technology.

SFM: What is your core user base?

GH: We have a significant, diverse client base made up of all of the participants listed above. The first mover on our platform was one of the leading asset managers. We leveraged their support to attract a subset of the sell side. As GLMX was able to deliver what it promised technologically, we gradually attracted more participants from each side of the market. I like to say that liquidity begets liquidity.

At this point, the vast majority of the sell-side uses GLMX technology – over forty will be on the platform by the end of the year. As our system sell side liquidity is compelling, we’re now able to onboard buy-side clients at a very rapid pace.

In particular, we are seeing an increase in demand from real money accounts to leverage our technology as repo is growing in importance as an investment vehicle. The increase in real money accounts, such as money market funds and corporate treasurers who trade electronically provides further efficiency to the sell-side, too, as more of their workflow is digitized.

SFM: We’ve heard that you’ve been advancing the “single digital interface” for getting multiple money markets on the same screen – what is the status there?

GH: Completely true and consistent with our long-standing objective. We have an ongoing pilot program for time deposits – which is a reasonably simple concept but also operationally complex for a lot of clients. And we’re now designing a solution for commercial paper. And as none of this would be possible without full straight through processing, we’ve spent the better part of 3 years building pipes to an extensive list of up and downstream systems, custodians and clearers.

I’d like to end with this key point: If you buy the premise that users and instruments in the global front end overlap massively, it makes obvious sense to have a single interface to access those liquidity pools.

Glenn is a 22-year veteran of JP Morgan Chase where he served as Managing Director responsible for Global Liquidity Management and as Chair of the Liquidity Risk Committee. His responsibilities within the Global Treasury Division included oversight of all debt issuance for JP Morgan Chase and its subsidiaries; development and implementation of the Bank’s asset and liability management process; and establishment of the Bank’s liquidity risk policies. Glenn holds an AB/Economics from Dartmouth College.

Glenn is a 22-year veteran of JP Morgan Chase where he served as Managing Director responsible for Global Liquidity Management and as Chair of the Liquidity Risk Committee. His responsibilities within the Global Treasury Division included oversight of all debt issuance for JP Morgan Chase and its subsidiaries; development and implementation of the Bank’s asset and liability management process; and establishment of the Bank’s liquidity risk policies. Glenn holds an AB/Economics from Dartmouth College.