The new ICMA European Repo Council survey was just released. The headline numbers don’t show a lot of change in the overall size of the market beyond the normal ebb and flow, but behind these figures are some interesting trends. We note some findings that the financial press seems to have skipped over including the fact that some of the largest banks increased the size of their repo books significantly, and this offset declines elsewhere.

The three main things that caught our eye were

- the increase in directly-negotiated trades

- the steady movement toward equities as collateral

- the dealer concentration trends in the market

Directly negotiated trades may seem innocuous, but they often represent transactions outside of the more commoditized part of the financing market. It is straightforward to deal in box standard trades in high quality collateral using electronic platforms. But when paper has more of a story behind it (or any unusual terms), traders like to negotiate on the phone or using direct messaging. ICMA says that 57.5% of trading is direct, up from 53.2% a year earlier.

Any increase in direct trading implies that these are more trades in lower quality paper at higher spreads. This has been a question that is often asked when trying to predict how repo dealers respond to having less balance sheet to play with. Will traders maximize their P&L by going for the high yield trades? That “story paper” can have less liquidity with pricing involving more guesswork & “mark to model”. Connecting all these dots without a ton of supporting evidence might be a stretch…

From the report:

“…The most notable change in business revealed by the latest survey is in the share of directly-negotiated transactions. This has been trending up since 2012, which is presumed to reflect a regulatory-driven shift away from low-margin interbank and commoditized transactions, much of which are electronically traded, towards higher-margin customer and customized business, most of which is directly negotiated…”

and

“…Direct business has been trending up since 2012 and, over the last six months, jumped. This was despite a fall in the share of tri-party repo (which is largely directly negotiated). In comparison with electronic trading, direct business tends to be longer-term, can be against non-government bond collateral and includes customer business…”

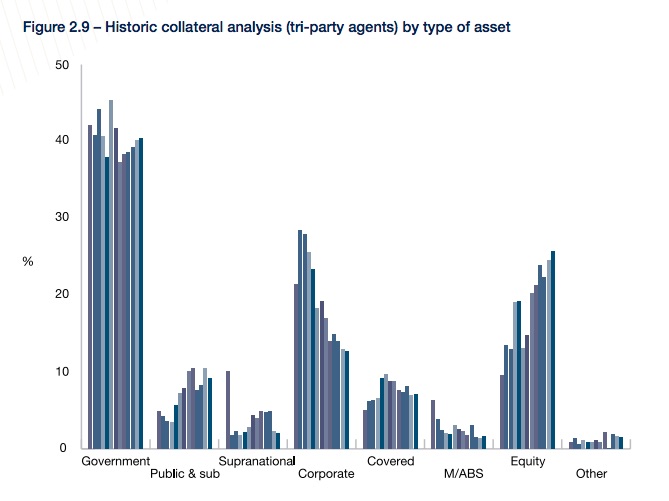

Perhaps connected with the bump in direct trading is the steady increase in the use of equities? They have wider spread than financing HQLA.

From the report:

“…There was a drop in the share of all government bonds within the pool of EU-originated fixed-income collateral reported in the survey to 77.0% from 81.5%. This change was driven to some extent by an increase in non-government bond and equity collateral…”

Source: ICMA ERC European Repo Survey, June 2015

The chart, which looks at tri-party trading, also shows a steady decline in corporate paper being used, almost mirroring the percentage increase in equities. Smaller dealer inventories and illiquidity in the corporate FI market may be culprit. While equities are volatile, at least the pricing and volume figures tend to be more transparent.

We also noted in our Sept. 16th post “ISLA’s 3rd Securities Lending Market Report shows an industry adapting well to market and regulatory changes” that (from the ISLA report) “…the past six months has seen a 13% overall increase in the lending of equity securities…” A lot of that flow seemed to be lending equities vs. borrowing HQLA paper for term — a trade that has LCR written all over it.

Dealer concentration is the other issue we wanted to look at. The very big seem to be getting bigger. Wasn’t this supposed to not happen? The intense regulatory focus on leverage was going push balance sheet hog / low return businesses like repo into shrink mode. It seems some of the biggest players are shrinking, but others growing quickly. The financial press hasn’t caught that subtle change.

From the report:

“…The market growth seen in the first half of 2015 also needs to be judged against the fact that the repo books of most survey respondents contracted again but was more than offset, in large part, by very significant increases in the repo books of a few of the very largest banks…”

and

“…The repo books of 35 of the latest sample of 65 institutions contracted, compared to 31 out of 67 repo books in the December 2014 survey. This means that more repo books contracted but those that expanded more than offset those that contracted…”

The change in the shape of market share is very interesting. The smallest dealers shrank and the next tier was split. The top half showed some big increases, with the bottom part (of the top half…) showing some big increases and the top-most tier expanding in some cases, shrinking in others. Did everyone catch that?

“…The bottom quartile of participants overwhelmingly shrank their repo books. But most of the third quartile expanded, many by a significant percentages. The second quartile was split: the lower half followed the general expansion in the third quartile but the upper half mainly contracted. Most of the top quartile also contracted but there were very significant increases in the repo books of a few of the very largest banks…”

The report suggested that banks were responding to regulation in different ways. Are some big banks not subject to balance sheet constraints? We don’t think so. ICMA said that in earlier reports, larger banks shrank more than smaller competitors. There are some new participants entering the market as profitability rises (at least in the US, we would expect some parallels in Europe) and this may account for the growth in the middle tiers. The strange behavior in the top tier — some growing by a lot, others shrinking — seems pretty schizophrenic. Maybe not everyone sees repo as a dying business?