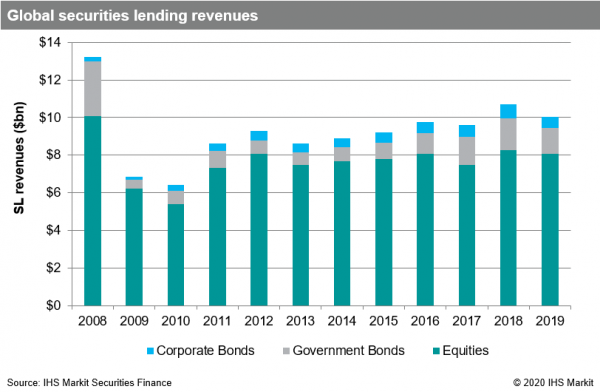

- Global revenue falls 6.3% to $10.1 billion

- 2019 delivers second-highest annual revenue in the last decade

- In North America, equity specials shine in 2nd half of year

- Fee compression weakens global fixed income revenues

It is neither the best nor the worst of times for securities lending, which means there is the opportunity for movement in either direction looking ahead to 2020.

At the end of 2018, things looked rather bleak for capital markets and securities lending revenues were soft given the decline in asset values which reduced loan balances. That makes Q4 2018 a relatively easy YoY comp, which Q4 2019 improved on by 3.8% with $2.4bn in revenues. That put the total for 2019 at $10.1bn, a decline of 6.3% relative to 2018. While the yearly revenue comparison is less favorable, the underperformance was primarily concentrated in the first half of the year.

Part of the narrative in recent years has been the push towards efficiency on the part of broker-dealers, which has resulted in greater amounts of broker-to-broker loans and internalized borrows. There has also been an increased presence on the part of retail brokers, in part the result of fully paid lending programs for retail investors gaining popularity.

These sources of lendable assets have reduced the demand for the traditional agency lending model; we see revenues from agency lending down 12.6% YoY in 2019. These additional sources of borrow have added market share, however most securities loans still come through the agency pipeline. The pressure on agency utilizations, along with a mandated lack of collateral flexibility for some beneficial owners, has caused a general shift in focus toward intrinsic value lending.

The resulting increase in fee level and volatility for hard to borrow securities has in turn challenged borrowers. Hedge fund frustration with borrow cost variability has led to an increased use of synthetic products. In theory, those products would be hedged in the underlying, however there is also the possibility of hedging synthetically as well. A consideration of securities lending revenues is therefore incomplete if it excludes the growing alternative sources of lendable assets.

Into 2020

With the opportunities and challenges of 2019 in the rearview, the future looks bright for securities lending. There has been an emerging dialogue on corporate governance which is vital to beneficial owners, though it’s worth noting that agents have actively managed lendable assets around corporate action record dates over the last decade per academic research, so it’s still important, but not new. The increase in lendable assets continues, largely as the result of asset appreciation though there has also been a consistent increase in accounts reporting to IHS Markit since the low point in 2013.

From 2008, the high point in securities lending revenue, to the low point in 2010, and up to the present much has changed and yet the core remains: the generation of lending revenues by beneficial owners, the funding of securities by asset owners and the provision of borrow to short sellers.