In late November, the Investment Industry Association of Canada (IIAC) held a panel discussion on the path to winding down Canada’s bankers’ acceptances, which will cease to exist as a money market instrument with the cessation of CDOR publication in June 2024.

BAs are debt instruments created by banks as a result of a client loan drawdown from certain types of lending facilities that have a BA based borrowing option:

- They are short-term discount instruments primarily issued in the 1-month tenor (the tenor of the BA matches the tenor of the client drawdown)

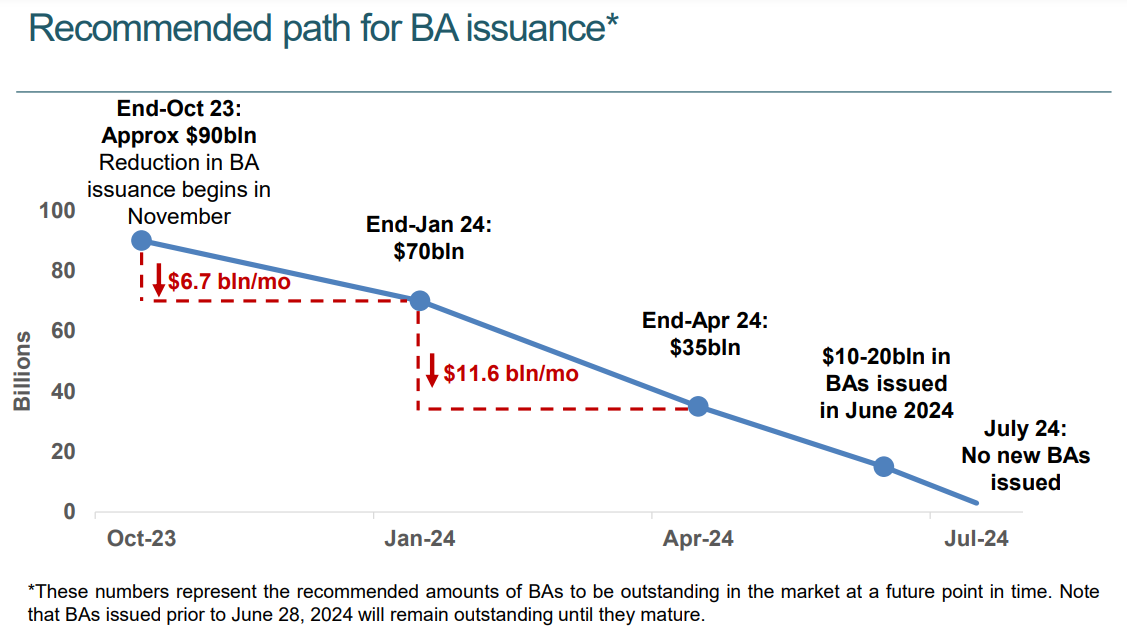

- BAs are the second-biggest security in Canada’s money market (accounting for about CAD$90 billion, or 20% of total assets) and are an especially important asset in the 1-month tenor for money market investors

- Banks will replace their short-dated BA funding with longer-dated bearer deposit notes (BDNs), bank deposits or other forms of funding. This will leave a gap in bank-issued money market securities, particularly in the 1-month tenor

The Canadian Fixed Income Forum (CFIF) has tasked the BA Transition Virtual Network (BATVN) to monitor and help facilitate, where appropriate, a smooth transition away from BAs to ensure the well-functioning of the Canadian money market. BATVN is co-chaired by Elaine Lindhorst (TD Asset Management) and Charles Lesaux (RBC Capital Markets).

Potential alternatives to BAs include both new and existing options.

New alternatives are: Triparty Repo – Canadian Collateral Management Service (CCMS) initiative from CDS (TMX); SGC Note –Secured General Collateral (SGC) Note from CDCC (TMX); Secured Discount Note –Bilateral collateralized commercial paper program; and Potential 1-month Canadian Government T-bills.

Existing Alternatives are: Bilateral repo; Government T-bills / Provincial T-bills; Asset Backed Commercial Paper (ABCP); Commercial Paper (CP) / New CP issuers; Floating & Fixed Rate Bank/Bearer Deposit Notes (BDNs); and Term Deposits.