Indemnification in securities lending has been a recognized part of the business for over three decades and is a must-have for most beneficial owner clients. But is indemnification still necessary for the majority of clients when balance sheets are reinforced by Basel III, and clients are engaged in peer-to-peer and central counterparties (CCPs)? In this article with State Street Securities Finance, we evaluate the pros and cons of indemnification in the current market environment.

Indemnification is typically viewed by clients as ‘insurance’ against a counterparty default, and clients believe it aligns their interest with agent lenders to ensure safe lending practices. As a large global asset manager told us, “Indemnification provides a great comfort to me and our Board. We could not lend without it.” Some asset owners have gone so far as to require indemnification as part of government legislation: the State of Louisiana says that, “Each securities lending agent shall indemnify the state for any losses resulting from the insolvency of a borrower.” Whether driven by market sentiment or a legal mandate, it is seemingly hard for any agent lender to avoid offering indemnification to their clients.

Indemnification imposes costs to the largest agent lenders that were not foreseen when the facility arose, and which are passed on to both beneficial owner clients and through to the borrower value chain. The option price of indemnification is close to zero, according to State Street research, and the capital cost of providing the indemnity was very low prior to Basel III. However, the introduction of Basel III and the US Collins Amendment raised the hurdle to an estimated 10.3 basis points based on a 12% rate of return and 15.7 bps with a 15% rate of return. For a General Collateral transaction that earns eight basis points from intrinsic value and one or two basis points from a government cash reinvestment pool, this may be a cost-ineffective solution for service providers.

For both agents and clients, a rethink about the value of indemnification may be due. Clients may find that although indemnification is preferred, the costs are higher than they think and indemnification may not, in fact, accrue them the benefits they believe may be in their best interests given collateralization levels and careful counterparty credit exposure management practices. One choice could be more variation in the provision of indemnification, with some clients choosing to continue and others opting-out across borrower and collateral types.

Tracking the costs of indemnification

Competition between agent lenders, and the fact that indemnification has rarely if ever been used even during the Global Financial Crisis, had served to hide the cost to clients. This is now changing as clients recognize that different routes to market, some indemnified and some not, mean differences in pricing and collateral margin. Francesco Squillacioti, Global Head of Client Management at Securities Finance State Street, recently said that “I started my career when there were unindemnified clients and then that disappeared. Now in the last 18-24 months, we have clients asking about being unindemnified. It’s about looking at the tradeoffs. Clients are sophisticated and don’t always want to pay for what indemnification entails.”

Indemnification costs show up both in the trade and the fee split. Large custodian banks indemnify from their own balance sheet, promising their clients that they will make up the difference in the event of a default. Other agents offer indemnification through an insurance company or other third party; the client may pay the cost directly or the agent might pay from their share of the fee split. Somehow or another however, clients are still paying the bill.

The direct cost to agent lenders that offer indemnification from their own balance sheet is found in the calculation of Risk Weighted Assets (RWA). Bank regulatory regimes around the world can be slightly different; US domiciled banks must calculate RWA using a standardized and advanced approach as required by the Collins Amendment and use whichever is the most conservative. Since the launch of Dodd-Frank, the Collins Amendment has had an output floor of 100% for the standardized approach to RWA. Non-US banks will see a change in the next iteration of Basel III that changes the floor to 72.5%. Agent lenders around the world may benefit from a separate change in Exposure at Default (EAD) calculations that account for correlation and diversity, which could produce balance sheet savings of up to 70%.

Revisions to Basel III, which have been long-discussed and fodder for many a conference panel on regulatory change, will be a change welcomed by securities lending practitioners. The question of when these changes are implemented is becoming clearer. However, two issues remain: first is that lending practitioners will still need to continue to operate under the old guidelines for some time; second, while these changes may have a positive impact on securities lending transactions, this must be considered in the context of each firm’s overall capital position.

Indemnification costs help raise the floor on the profitability requirements of securities loans and cash collateral reinvestments. The more that clients need indemnification, the higher this floor becomes. But when the market rate is below the floor, indemnified clients may be missing out on market opportunities compared to unindemnified lenders. Lower rates mean lower costs through the securities lending value chain and more opportunities to do business, as well as more transactional liquidity for the market as a whole.

The economic and emotional value of indemnification

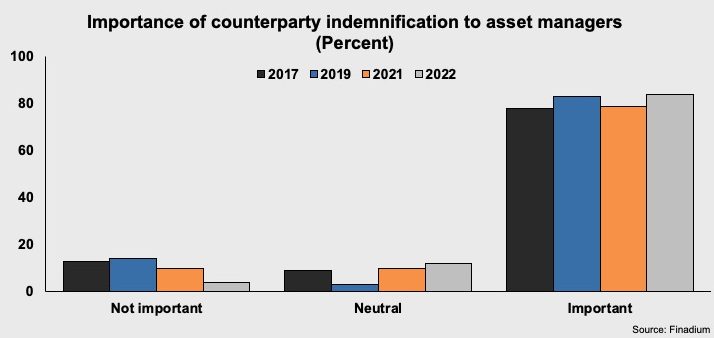

Beneficial owners both like and believe in the value of indemnification as insurance against a counterparty default. In Finadium’s November 2022 survey of large asset managers in securities lending, 84% of executives reported that indemnification was very important for their program, up slightly from 79% in 2021 and consistent with prior years. For the majority of clients, lending without indemnification would be either unthinkable or could be rejected by their Boards.

The 16% of funds that said indemnification was not important or were neutral were focused first on counterparties and collateral. As a securities lending manager at a large European firm noted, “if you really have to worry about indemnification, you haven’t set up your counterparties and collateral correctly.” Indemnification is meant to fill in any possible gap between counterparty risk and collateral exposure, and should optimally have no role at all.

The economic value of indemnification appears to be weak: in a recent white paper, Credit Benchmark CEO Mark Faulkner noted that “the distortions associated with agency lending indemnification have been most detrimental to the lending agents, whilst broadly benefitting the beneficial owners and the borrowers.” So long as agents keep paying the bill, everyone is happy, but is the cost worth the warm feeling that clients receive from it? And while borrowers have benefitted from certain pockets of supply in the market, they may be more on the losing end as indemnification costs mean higher rates than what they may pay otherwise. Agent lenders say that if clients paid the actual cost of indemnification then they would be happy, but this would result in even more intense fee split competition for client business. No agent lender wants to be the first mover.

Glenn Horner, Managing Director and Chief Regulatory Officer for Global Markets at State Street, said that the firm needs to justify the capital they are utilizing to continue to provide indemnification. “The long-term hope is that some things realign with the finalization of Basel III; they won’t go back to pre-2013 but could get back to a decent position.” The more that clients are willing to consider their emotional and economic attachment to indemnification, the more opportunity there may be for market-wide progress.

Agents say that there are no recent cases of borrower defaults where indemnification has been needed, and that they are comfortable pricing their clients based on different tiers of indemnification for some portfolios but not others. At the May 2022 Finadium Investors in Securities Lending Conference, some agents asked about the relevance of indemnification at all given the reliance on cash collateral reinvestments that are not indemnified. Agents also emphasized the ongoing disconnect between the reality of their non-commoditized business versus regulatory and public thinking that one loan is the same as another. In practice, there are multiple factors that influence pricing both for client fee splits and individual transactions.

A call to action

To date, the costs of balance sheets and higher loan rates leading to lost utilization and liquidity have rarely been priced in to agent lender indemnification offerings. Some agent lenders have priced client portfolios with and without indemnification, but the end result so far has largely been a choice for indemnification. This may not be in the best interest of beneficial owners, but how can agents and clients engage in a conversation about the cost of indemnification without creating price competition with other agent lenders?

One starting point is a recognition that perhaps indemnification in its current form has outlived its purpose of ensuring clients against the last piece of market risk in their programs after collateral. If the objective is to ensure that clients have a AAA credit experience in their lending programs, perhaps this is now being met by the combination of collateral plus the current balance sheets of large lenders, although indemnification may still need to apply to smaller lenders.

Clients may also be encouraged to consider the value of indemnification in light of peer-to-peer and central counterparty (CCP) opportunities for lending. While both could still be indemnified, neither need to be to achieve the desired goal. Some beneficial owners have stated publicly that especially for low-risk General Collateral loans, they see no need for indemnification against a peer. CCPs operate with a default fund to effectively insure members against any one counterparty’s risk. Is agent lender indemnification still needed in that scenario, or is “CCP indemnification” enough?

A good time has come for agent lenders and beneficial owner clients to have a conversation about the value of indemnification and where it comes from. The benefit of flexibility could result in better utilization and lower costs through the value chain, leading to gains for clients, agent lenders, borrowers and the broader market.

This article was commissioned by State Street Securities Finance.