A new research report from IOSCO looks at major trends in the corporate bond market over the last 13 years and going forward. While the study overall has some solid details on corporate bond issuance and secondary trading, the most interesting parts to us were towards the end. These focused on how the corporate bond market is already changing to account for less liquidity and what the authors expect could happen going forward.

In the report, “Corporate Bond Markets: A Global Perspective Volume 1” by Rohini Tendulkar and Gigi Hancock, the authors note the obvious reduction in corporate bond liquidity as new financial rules discourage structured products and dealer costs increase. They also note that while corporate bond trading statistics look healthy, “a number of research studies on the subject suggest that trading volume figures are being propped up by a small number of bonds being traded over and over.” This is consistent with what he hear about deep concerns in corporate bond liquidity. Indeed, SIFMA data show average daily US corporate bond trading in January 2014 at US$21.1 billion, up from US$14.8 billion in December 2013. Not to be too US-centric about it, but the authors also use SIFMA data as a reliable source of turnover data.

So what to do about liquidity?

“Markets could transform through increased usage of multi-dealer electronic trading platforms that allow non-primary dealer actors to provide liquidity. This may require some standardization of bond issuance, a move that could erode the tailored financing nature of corporate bond markets compared to equity markets and other forms of financing.”

Let that sink in for a minute: fewer corporate bond types (not yet happening), much fewer principal inventories (already happening), centralized trading (limited today), “non-primary actors” providing liquidity (are these Shadow Banks?). The authors continue:

“Issuing firms may choose to either standardize issuance in order to decrease liquidity risk and thus borrowing costs; or continue to issue tailored bonds but at a premium to account for reduced liquidity. This could result in a segmented market similar to listed equity and private equity markets; or standardized and over-the-counter derivative markets.”

This is indeed transformative stuff. Let’s set aside for a moment how issuing firms would respond and stay with the question of dealer liquidity in the secondary market. The authors are suggesting that the market is already moving in this general direction. “The ‘miniature stress test’ of the late 2013 bond sell-off highlighted the resilience of the secondary markets. Trade sizes momentarily declined and there was an uptick in the use of electronic trading platforms during this period.”

Given the clear regulatory push for dealers to hold less inventory, we think the authors are on to something. We’re not sure we agree with all of their expectations, but the idea of dealers acting more as agent and less as principal, for a smaller set of corporate bond types, makes sense.

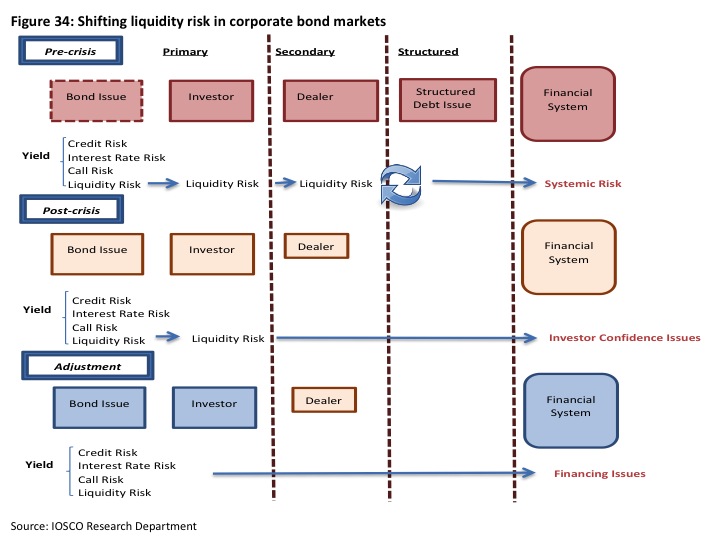

See below for a useful graphic provided by the authors to visualize their expected change in liquidity risk.