One industry objective of a securities lending CCP is to drive lender participation and increase the size of the overall market. By providing a known and consistent counterparty, as well as lowering borrower costs and potentially improving prices, more lenders should be incentivized to join up and borrowers should have more capacity. We test the idea of whether Eurex’s Lending CCP is succeeding in market expansion, including whether lenders are utilizing the CCP’s services for non-traditional purposes.

Eurex’s Lending CCP is the first global example of a CCP that offers buy-side membership for securities lending services. When the idea was discussed in the early 2010s, borrowers were immediately interested but the buy-side and agent lenders took longer to sign on. By 2020, however, Eurex was successful in seeing buy-side firms come directly to the CCP and agent lenders participating on behalf of underlying clients. Both market participants and Eurex report that there are important points of momentum that prove the value of the model.

Alongside individual firm considerations, changes to the broader European regulatory landscape and industry trends have supported the Lending CCP business case for post-trade automation. The introduction of the Securities Financing Transactions Regulation (SFTR) has encouraged electronic trading and processing for the generation of unique transaction identifiers (UTIs) and other information that can be manually intensive to process. CCPs solve a series of operational and technological challenges for reporting firms. SFTR data from 31 July 2020 show €1.26 trillion ($1.49trn) of European securities loans transactions; this is a large market with shared infrastructure needs.

This article explores why firms are engaging with the Lending CCP, where having a securities finance CCP matters most, and if, in the end, the size of the market can be expected to grow as a result of the CCP’s services.

How buy-side firms are engaging

One piece of big Eurex news of the last few years – that Dutch pension fund PGGM signed on as a Lending CCP client – has been followed up by a variety of new types of lenders. Eurex reports that new sign-ups and prospects are roughly 50% lenders coming directly to the CCP and 50% agent lenders. Direct lenders tend to be larger institutions that can connect through existing market infrastructure like EquiLend NGT or Pirum’s CCP Gateway. Lenders see that the balance sheet benefits to their borrowers outweigh the set-up time, and that collateral upgrades for term can be safer and more efficient using the CCP’s services. Both lenders and borrowers say that the set up can be daunting, but that the risk and pricing improvements are either worth it already or are expected to be worth it in the near future.

Eicke Reneerkens, Head of Securities Lending at Union Investment PrivatFunds GmbH, thinks that the move towards electronic trading and central clearing is on track. Five years ago, he projected that most of his firm’s securities loans would be centrally cleared by 2025. While PGGM was the first wave, Union Investment is part of a second, much larger wave of client adoption on the way. Reneerkens sees the move towards a CCP as helping all participants in the process: “Like OTC derivatives, we prefer to trade securities loans on an exchange rather than OTC. We get one counterparty in the event of a counterparty default, the CCP, and we can help the banks. Balance sheet relief doesn’t help me as a fund management company but some of the bank’s benefits are shared in better pricing. This is an improvement for our clients and our firm.”

Agent lenders are joining the CCP on behalf of beneficial owners for the same underlying reason as direct lenders – better RWA for borrowers – as well as capital benefits to their own businesses. They can continue to offer their clients outsourced operational support and counterparty default indemnification; even with the CCP, the indemnification service continues to be sought after. Eurex reports that agent lender interest is centered around fixed income term transactions with equities in a collateral transformation trade.

Mike McAuley, Global Head of Product Development & Strategy for Securities Finance at BNY Mellon, notes that the CCP serves an important function by providing borrowers with the capital benefits of collateral held by the CCP when transacting with lenders domiciled in a jurisdiction where borrowers may not be able to obtain a clean netting opinion. Clearing through a CCP also provides the borrowers the benefit of the CCP’s risk weight when transacting with other lenders that would be unattractive counterparties from an RWA perspective. McAuley notes that “the CCP is our only distribution channel where demand exceeds supply and, as a result, it attracts a premium.”

McAuley finds the CCP model attractive from an operational and use standpoint and points out that “the CCP also helps agent lenders and large banks handle their capital requirement constraints. Not all trades will migrate into clearing but over time we expect CCP adoption to grow.” The biggest hurdles currently are in the documentation and ease of onboarding; the easier this gets and the more that clients are educated about the CCP in the context of known agreements like the GMSLA, the faster clients will adopt the platform.

Colin O’Keeffe, Director in the Equities and Securities Services business at Citi, agrees that a competitive RWA is a key reason to use the Lending CCP for both lenders and borrowers. “If banks and broker-dealers have RWA pressures to any degree or are looking to optimize, although there is an upfront material effort and cost associated, the upside of RWA reduction is clear to see as the CCP market grows for securities lending. This will become more competitive over time as critical mass arrives on the platform.”

The CCP’s RWA benefits also reflect a competitive dynamic impacting the securities finance industry more broadly. Finadium has shown in multiple studies that a centrally cleared securities loan can be as balance sheet competitive as a bilateral or CCP-cleared equivalent Total Return Swap. If lenders are competing on RWA against both each other and economically similar products, then joining the CCP can even the playing field. And the more buy-side firms that join, the more that others will see CCP membership as important to keep a competitive RWA and maintain their inventory utilization.

Term vs. overnight

Eurex tells us that 70% of the Lending CCP volume is term compared to 30% overnight. The CCP is capturing this business compared to the bilateral market due to rate improvement and better default management processes. This can become an important internal argument for lenders in favor of the CCP, not to mention that dealers are asking their counterparties to send trades to the CCP when possible. Market participants report that they prefer to start using the Lending CCP with General Collateral overnight names; this is a way to test the model with a moderate amount of commitment. O’Keeffe says that for Citi, they will look to term and collateral upgrade trades as the CCP relationship grows.

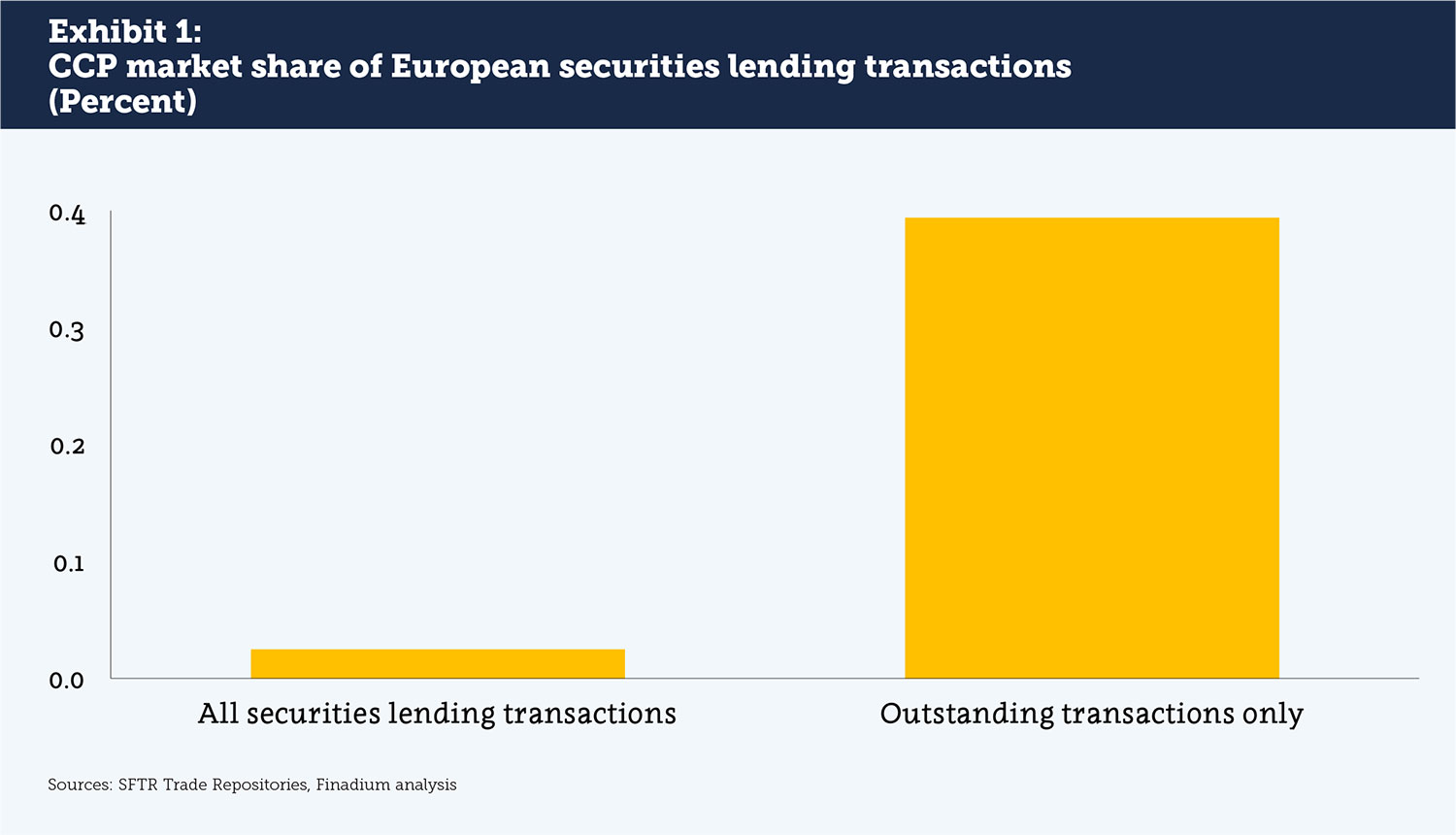

The idea that CCPs are efficient venues for term trades is reflected in initial SFTR data. From SFTR reporting from Trade Repositories on 31 July 2020, CCP business was .02% of all securities lending activity but .4% of outstanding transactions (see Exhibit 1).

The reverse stock loan trade

Eurex is reporting a new dynamic on the Lending CCP: interest in their reverse stock loan product. In a reverse stock loan, a borrower of securities places cash with the lender. Buy-side borrowers have no margin requirements owing to the structure of the CCP membership model. Eurex notes that 50% of market demand is now in reverse stock loan for funding, where a money fund desk can earn a better return on cash than in a money market by accepting corporates, equities or government bonds as collateral.

A reverse stock loan is conceptually similar to the Fixed Income Clearing Corporation’s sponsored repo model, which European market participants would like to see replicated in Europe. Eurex says that reverse stock loan participants are arriving from Treasury desks around the world, not just in Europe. But the attraction of the Lending CCP over the repo market is mostly operational and legacy; a client with an existing GMSLA is more likely to be comfortable with securities lending for funding instead of repo.

The need for buy-side desks to invest cash challenges the idea of Europe as a primarily non-cash marketplace for securities finance. While a more traditional securities loan may be against non-cash, the use of the product for new purposes means that previously unused inventory can now see demand when cash is acceptable. The protection of the CCP risk default waterfall can support lenders and borrowers in the trade, and even lead to a market where a bank can borrow cash from a Treasury desk then redeploy that cash for a loan on the same CCP. This opens up new opportunities across the market.

Two ways to expand the market

The securities finance market can grow either by increasing capacity at existing firms or encouraging new firms to join. It appears that the Lending CCP is succeeding on both fronts. Citi’s O’Keeffe says that “the CCP enables us to connect further with our current clients, and gives us capacity to continue our business growth.” BNY Mellon’s McAuley also cites expanded capacity as a direct reason for supporting the CCP, and Union Investment’s Reneerkens appreciates both the price improvement and security of the CCP risk model. Meanwhile, reverse stock loan participants are showing new interest in securities finance as a cash destination.

The motivations of direct members, agent lenders and borrowers ranges from operational efficiency to price improvement, which is especially valuable in the continued low interest rate environment. O’Keeffe notes that the CCP is now more than a “nice to have”; it is really a “should have”. With more client education and a streamlining of the onboarding process, we expect that Eurex’s Lending CCP will continue to expand the securities finance market going forward.

This article was sponsored by Eurex.