Repo can learn a lot from the securities lending market. Automation in securities lending post-trades processing is at an advanced state whereas repo participants are at various stages of transitioning from manual to electronic practices. This article draws on Pirum’s recent market experiences to identify opportunities for repo market participants going forward.

Financial markets are looking for automation. It is clear that Straight-through Processing (STP) creates efficiencies by reducing operational errors and managing complexity across hundreds or thousands of transactions requires systems that can scale effectively. The trend towards automation has been as notable in securities finance as anywhere else, where managing balance sheet exposure is a critical part of the trading exercise. STP enables near real-time analytics of counterparty and risk positions, which translates into tangible cost savings where collateral exposures are reduced.

The repo market has lagged behind securities lending in post-trade automation. This imbalance is beginning to change as previously manual repo processes are not supportable given a competitive cost environment, ongoing balance sheet constraints and the increased application of technology on all trading desks. Repo is already a key product that many firms use to control their liquidity and capital exposures; close management of repo trading activity is a prerequisite for effective capital management. Going forward, it is expected that more repo trading will become automated partly to support regulatory requirements as well.

A transition to repo automation will happen most successfully if the market has a vision for where it is heading. Securities lending offers one such vision, having made the transition from a manual to electronic market already in both the front and back office.

Automated or not?

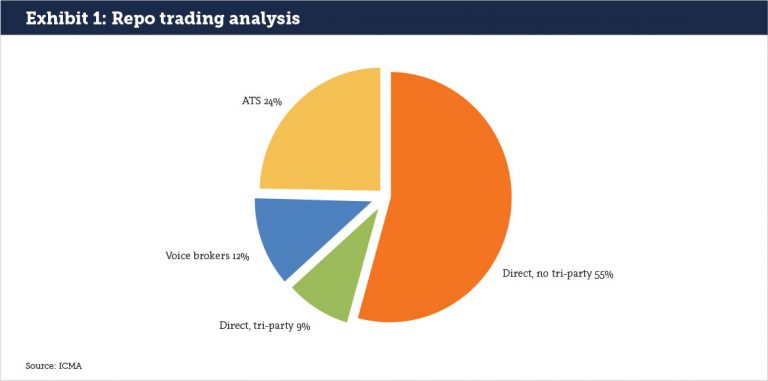

Today’s repo market is an agglomeration of bilateral and central counterparty (CCP) cleared trades amongst government, bank and cash management participants worldwide. The December 2017 ICMA European repo market survey shows that direct transactions with bilateral processing are the most popular, with tri-party, Interdealer Brokers and Automated Trading Systems all having an active role (see Exhibit 1). Following the trade, collateral movements and valuations may be managed internally, by tri-party, a CCP or a tri-party agent after receiving netting details from CCPs. Most firms are using internal systems to reconcile their outstanding CCP and bilateral positions.

The repo market struggles with its own inefficiencies, some of which are now being mitigated by firms adopting more advanced technology to manage the processing. In recent years there has been focus on netting only at end of quarter, which has resulted in last minute scrambles to rebalance trading books. Correspondingly, repo has not always been integrated with other balance sheet metrics in a timely fashion, leading Treasury managers to direct repo transactions that lift or lower liquidity requirements to the detriment of the trading desk. All three of these challenges are receding although the pace varies by firm type and sophistication.

On the other hand, securities lending is one of the most automated business activities from a post-trade perspective in capital markets. Repo may be more automated on the trading side due to more plain vanilla transactions, but in post-trade, there is more manual work required to ensure smooth processing. Securities lending post-trade on the other hand is managed by vendors that consolidate trade information and act as connectivity hubs in order to streamline the trade lifecycle. Securities lending transactions are easily captured on one or several platforms for reporting and capital management purposes.

Operational inefficiencies still exist in securities lending but are rare; the primary exceptions occur when firms fail to deliver securities that have been recalled. A recent ISLA survey of securities lending settlement practices showed that five out of seven reporting borrowers said that their settlement rates for new borrows was over 80%. When fails occur, they are almost always because settlement instructions are not in place. 83% of respondents with a plan said that they will use pre-trade matching services to improve settlement rates prior to the introduction of the Central Securities Depositories Regulation (CSDR).

Similar data does not exist for the repo market, but anecdotally, fail rates can be much higher than the securities lending market. In 2016, the US Treasury repo market had fail rates spike to 13%, the result of balance sheet tightening and less inventory held by primary dealers. Balance sheet constraints will continue to drive the need to reduce fail rates. Fails in any market increase counterparty risk, unsecured credit costs and could have knock-on effects leading to poor trading and operational market functioning.

The securities lending market is turning to greater utilization of tri-party to manage operations due to the fact that the counterparty set and complexity has expanded. In an October 2017 survey of tri-party providers, Finadium found that 25% of the AUM of tri-party was based on securities lending transactions compared to 20% across all non-repo products in 2014 including securities lending. This increase is partly due to the operational efficiencies of tri-party and the growth of non-cash collateral usage.

The functional overlap between securities lending and repo

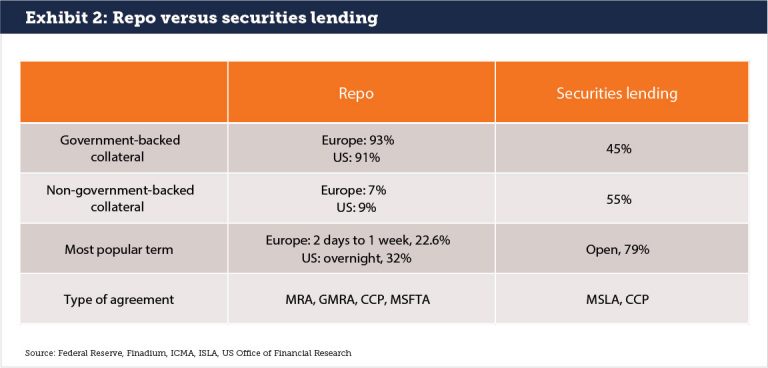

Conceptually, securities lending and repo are similar products. Both exist to temporarily lend assets between counterparties in exchange for collateral. SFTR captures both products in its reporting expectations. Regionally, the preference for repo over securities lending, or vice-versa, is driven as much by historical practices as the inherent structure of each product type. Sometimes the decision is due to what legal agreements a firm has in place with market counterparties. Market data from US and European sources show that in practice, market participants lean towards repo for government-backed collateral and securities lending for open trades (see Exhibit 2).

The situation is different in equities however; equity repo financing is primarily to cover margin positions and fund a bank or brokerage while cash is on loan; this is the original function of rehypothecation. While equity repo can also be used to source securities for short-selling, market participants typically turn to securities lending for that option. Securities lending is more flexible in terms of posted collateral. Where repo requires cash, a securities borrow can be for cash or non-cash.

Regulations are driving automation

The move to a more automated repo market is not just a nice idea: it is also driven by major new European regulations that come with heavy penalties for non-compliance. These regulations impact resource limits, margins and a drive towards efficient and scalable business units. As one example, SFTR requires firms to identify over 150 fields for possible submission to a trade repository; this is practically impossible for a human to accomplish for any quantity of trades. The only real way that regulatory reporting can happen is with the use of technology and automation. Non-compliance can lead to cash penalties plus reputational damage.

As another example, CSDR on the other hand carries cash penalties for settlement fails and mandatory buy-ins for fails. Cash penalties can range from0.25% and 0.50%, which are high for General Collateral securities but low for specials. The buy-in mechanism is unknown, untested and could cause instability in both the securities lending and repo markets. Most securities lending participants are prepared to meet CSDR requirements; anecdotally, not all repo market participants are able to say the same.Between CSDR and MiFID II, the cost and importance of fails is set to increase.

Pirum’s recent experience in the market

A concurrent desire by market participants is to centralize a range of liquidity and collateral-related functions, including the convergence of product and trading silos in the front and back office. It is no longer practical from a commercial or economic standpoint to maintain different funding and operational silos across multiple business lines. This trend has been evident for some years but is picking up renewed steam. Change must be underpinned by systems and technology that can support, simplify and centralize the lifecycle management across multiple product lines.

While repo allocations have shrunk by an estimated 60% to 80% since the financial crisis, they have lately grown again as banks have right-sized their capital across the firm. Banks in particular recognize that an enterprise-wide perspective is the only effective way to best manage their financial resources. Likewise, an inefficient post trade process across the collateral ecosystem is a drag on profitability that can determine a business line’s fundamental existence as well as its capacity to service its clients.

Pirum has aligned its connectivity hub to be product agnostic to where a trade is executed, settled or collateralized. We cross execution and settlement vendor platforms, and offer a network for client collaboration in real time.Our suite of tools across the transaction lifecycle (affirmation and pre-matching, life-cycle event management and automation, collateral workflow and efficiency) is commonly used in the securities lending market and is directly applicable to the repo market as well.

Todd Crowther is Head of Client Innovation at Pirum.During a 20-year career in investment banking, Todd held a number of senior sales & trading roles in Prime Brokerage, Equity Finance and Derivatives at PaineWebber, ING, Deutsche Bank and Nomura. In his last sell-side role, Todd was Head of Equity Finance Trading & Liquidity Management at Nomura in London. More recently, Todd acted as advisor to a major European exchange in developing its secured finance trading platform. Having joined Pirum Systems in 2017 as Head of Client Innovation, one of Todd’s major focus areas has been spearheading the development of Pirum’s new CollateralConnect platform, a collateral management solution for the market.

Todd Crowther is Head of Client Innovation at Pirum.During a 20-year career in investment banking, Todd held a number of senior sales & trading roles in Prime Brokerage, Equity Finance and Derivatives at PaineWebber, ING, Deutsche Bank and Nomura. In his last sell-side role, Todd was Head of Equity Finance Trading & Liquidity Management at Nomura in London. More recently, Todd acted as advisor to a major European exchange in developing its secured finance trading platform. Having joined Pirum Systems in 2017 as Head of Client Innovation, one of Todd’s major focus areas has been spearheading the development of Pirum’s new CollateralConnect platform, a collateral management solution for the market.