Use of the Federal Reserve’s overnight reverse repurchase (ON RRP) facility rose in 2022, coinciding with deposit outflows and declining reserves at commercial banks. A popular narrative suggests that regulatory capital requirements discouraged bank deposit-taking, driving up ON RRP use. However, this story neglects important contributors to the ON RRP’s surge. Researchers from the Federal Reserve Bank of Kansas City find that limited money market investment opportunities, policy uncertainty, and administrative changes likely explain increased ON RRP activity.

The researchers also argue that exempting banks from the supplementary leverage ratio (SLR) once more may not have the desired effects. When a pandemic exemption to the SLR expired in March 2021, bank deposit growth slowed and ON RPP usage increased. However, ON RRP take-up significantly outpaced net MMF inflows during 2021, suggesting factors other than deposit migration contributed to the ON RRP’s rise.

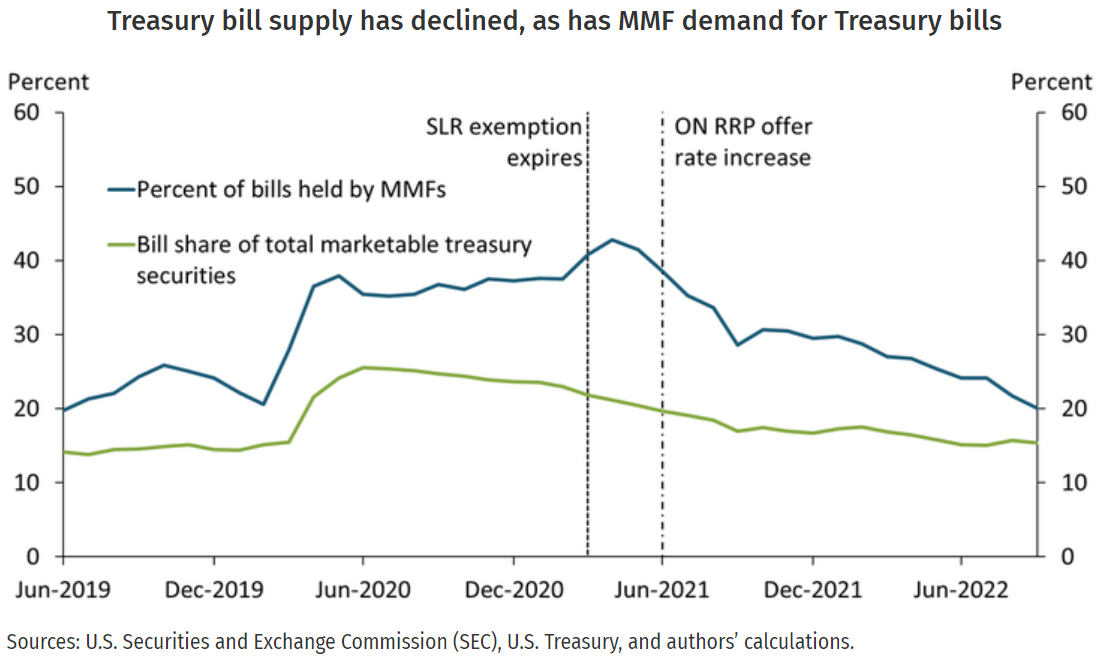

First, market investments for money market funds (MMFs), statutorily limited to short-maturity assets, became scarcer as outstanding Treasury bills began to decline in 2020:Q2. The share of US debt financed by short-term Treasury bills peaked in mid-2020, but bills outstanding have since declined by $1.5 trillion, moving the share toward historical averages.

Second, Federal Reserve asset purchases continued until March 2022, creating additional liquidity that flowed into both banks and MMFs. Third, administrative changes to support monetary policy implementation during a period of softening money market yields made the ON RRP more attractive to counterparties. In particular, the Fed relaxed ON RRP eligibility criteria, raised daily ON RRP counterparty limits, and increased the ON RRP offer rate. More eligible funds, larger counterparty limits, and higher offer rates all helped increase ON RRP usage during this time. Indeed, the share of total Treasury bills outstanding held by MMFs declined after these changes.