As registered vehicles with the SEC, leveraged US mutual funds , including open and closed end 40 Act funds, must adhere not only to robust reporting but also Uncleared Margin Rules for OTC derivatives for the largest funds, and securities and margin borrowing protocols for stocks and bonds. Their combination of hedge fund-style strategies plus regulatory obligations puts leveraged funds in a unique position, which both contributes to their appeal and raises their operational requirements. A guest post from Bob Zekraus and Marc-Andre Wilson at Scotiabank.

US mutual funds and ETFs that employ leverage are an unusual part of the asset management ecosystem. As registered vehicles with the Securities and Exchange Commission (SEC), these funds have a robust raft of reporting obligations including annual reports, holdings reports and more under recent SEC modernization rules. At the same time, the funds themselves function more like hedge funds for daily investors than traditional long-only mutual funds. From a financing perspective, the traditional prime brokerage model has been adapted to also service this part of the investment community.

The idea of leveraged funds has seen some contention in the last year out of concern that retail investors might not know what they are purchasing. In 2019, the SEC proposed rules that would have required among other things that investors self-certify that they understand the risks of leverage. Both the SEC and issuers agree that these products are not for everyone and that the right type of investor must pay close attention to their portfolio. While the SEC has not taken action yet, the potential remains.

Meanwhile, leveraged funds that trade OTC derivatives must adhere to Uncleared Margin Rules if they are large enough; this is a small group but still important. These funds must understand their collateral obligations with counterparties and, like any fund manager, optimize their collateral use across derivatives and securities financing.

For investors, leveraged mutual funds provide a viable access point to the markets. The importance of these vehicles for sophisticated investors should not be overlooked: when leverage is part of the trading strategy, these funds balance simplicity with low cost. This article looks at the size and strategies of leveraged ETFs and mutual funds, along with upcoming challenges and opportunities to the business model.

Market size and fund strategies

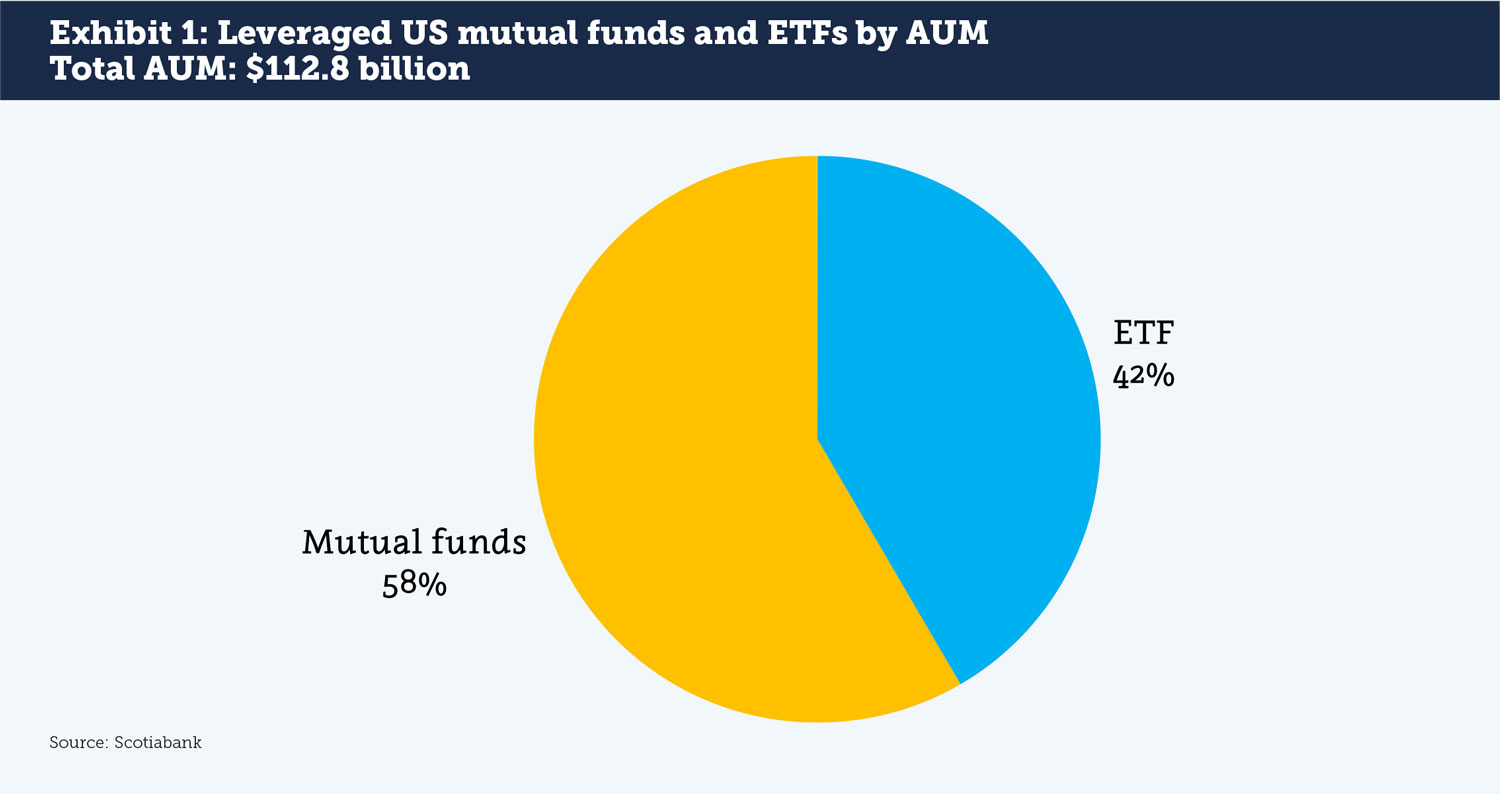

There are over 300 leveraged ETF and mutual fund strategies registered with the SEC with a total AUM of $112.8 billion (see Exhibit 1). We have identified 145 ETFs with US$46.9 billion in AUM. ProShares and Direxion are the largest players, while eight other managers have offerings available in the market. The objective of these leveraged ETFs is to deliver a multiple of returns of an index, ranging from -3 (an inverse ETF) to 3. In fund literature, this can also be written as -3X to 3X. Funds accomplish their leverage objective through a mix of long-only holdings and swaps, typically based on another fund that tracks the underlying index. For example, a 3X NASDAQ ETF might hold the Invesco QQQ Trust then enter into swaps agreements with banks to achieve the necessary leverage. The swaps themselves reset on a daily basis, allowing the manager to invest the exact amount that it has gathered from clients.

The mutual fund landscape is more diverse with US$65.88 billion in AUM and offerings from 94 firms. While a few well-known names like BlackRock, Calamos and SEI lead the AUM ranking, other funds manage from US$1 million to over US$3 billion. Many of these funds are long/short equity or market neutral, with the fund relying on the expertise of a human portfolio manager. A few funds are quantitative, shifting the human portfolio management responsibility to a computer model. Some funds employ leverage from securities and margin borrowing from a prime broker, while others use OTC derivatives. In all cases, these funds are looking to meet investor needs by extending beyond a traditional long only mutual fund into what clients hope are differentiated strategies that can effectively manage market risk and/or generate excess returns.

Regulation vs. flexibility

As regulated entities, leveraged mutual funds must file extensive documentation with the SEC that a hedge fund or private trader would not. These filings now include Form N-PORT, which provides details on the specific strategies, positions and holdings used for each fund.

For individual investors looking for transparency, this reporting may provide some comfort that leveraged mutual funds do not operate as a black box. For example, the names of positions, counterparties, quantities and securities on loan allow an investor to have some understanding of where their money is going. This is not a perfect system, as reports are released by the SEC with a two-month delay. Still, it can be more informative than a hedge fund 13F filing that is issued both with a delay and may no longer be required for funds with less than $3.5 billion in assets if the SEC adopts its proposed amendments to Section 13F.

For leveraged ETFs, the general consensus seems to be that they are best employed as a day trading tool, or at most held for just one or two days. This allows investors to get in and out of specific market opportunities as desired. As one example, the Direxion Daily CSI China Internet Index Bull 2X fund with $57.5 million in AUM had a one-day return of 4.3% on August 5, 2020 while the underlying index gained only 1.7%. The same trade held overnight however could have resulted in a serious loss. This is typical of leveraged ETF products, and is among the reasons why the SEC has proposed including warnings for retail investors before purchasing.

The leveraged mutual fund sector on the other hand aims to attract long-term capital much as a hedge fund would. These products are meant for regular investors looking for diversity or to mimic a hedge fund strategy that would otherwise be too opaque or high cost to enter. For example, the AQR Diversified Arbitrage Fund with $393.4 million in assets looks similar to any long-only mutual fund with a total expense ratio of 1.2% and a strategy to acquire assets over an extended period. Unlike a traditional long-only fund however, returns are from a combination of event-driven, convertible arbitrage and merger arbitrage strategies.

Scotiabank works with leveraged US mutual funds and ETFs, as well as alternative mutual funds in Canada (NI 81-102 funds) and Europe (UCITS funds). Typical leveraged products offered by Scotiabank to mutual funds and ETFs include tri-party margin lending, short selling, securities lending, repo, and OTC derivatives such as portfolio swaps and index swaps. In addition, Scotiabank may assist with financing through revolving loans, structured notes, and preferred share offerings. The details of each financing arrangement will depend on the fund’s strategy, investment guidelines, and operational requirements. Scotiabank has witnessed the challenges faced in the business model of such regulated funds, but also the opportunity that the strategies represent that are available for investors looking for short-term leverage exposure to alternative investment strategies, without the cost and complexity of trading derivatives or obtaining leverage themselves.

Robert Zekraus, Scotiabank Global Banking and Markets, Prime Services

Robert Zekraus, Scotiabank Global Banking and Markets, Prime Services

Managing Director, Global Head of Client Capital Management & Funding

Robert (Bob) Zekraus is responsible for Client Capital Management & Funding for the Prime Services division. This mandate focuses on managing the asset and liability profile of the business, client pricing, and the strategic deployment and oversight of scarce financial resources. In addition, Bob works on developing customer-focused financing solutions that align with Prime Services risk appetite, liquidity, capital and balance sheet strategies. Bob serves on the Board of Directors of Scotia Capital (USA) Inc. He is a member of the Prime Services Executive Committee and global management team. He chairs the weekly funding and balance sheet forum and sits on the bank’s US ALCO and liquidity and market risk committees.

Prior to joining Scotiabank in 2014, Bob was Director, Prime Services, at Barclays where he was a member of the Global Equity Finance management team. He held various senior leadership roles in equity financing and prime brokerage. He was part of the original team that established the Collateralized Finance Group at the firm. Bob started his career at Daiwa Securities Inc. in Prime Brokerage. Bob received a B.S. degree in Economics and Business Management from Cortland College.

Marc-Andre Wilson, Scotiabank Global Banking and Markets, Prime Services

Marc-Andre Wilson, Scotiabank Global Banking and Markets, Prime Services

Director, Business Development

Marc-Andre Wilson is responsible for Business Development for Prime Services globally. This role focuses on structuring and executing securities finance and derivatives transactions for clients of Prime Services. In addition, Marc-Andre works on designing and implementing client products and internal arrangements to optimize net revenue, balance sheet usage, regulatory ratio impact, and other internal requirements of Scotiabank. Prior to his current role, Marc-Andre was the Global Head of Client Transition for Prime Services, responsible for managing the on-boarding of new client relationships. Prior to joining Scotiabank in 2012, Marc-Andre was an Associate at Stikeman Elliott LLP in Toronto. Marc-Andre received an HBA from the University of Toronto and an LLB from the University of Ottawa.