An article from last week (Dec. 2, 2013) in the NY Fed’s blog Liberty Street Economics is worth a closer look. Entitled “Who’s Lending in the Fed Funds Market” by Gara Afonso, Alex Entz, and Eric LeSueur, it reviews the sorry state of the Fed Funds market.

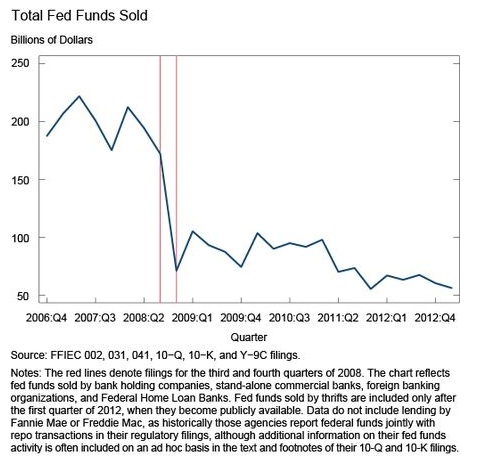

The Fed Funds market has shrunk from around $200 billion in 2007 to near $60 billion at the end of 2012. In the process, it has become something of a one trick pony – the GSEs (and in particular the FHLBs) lending cash cheaply. Unlike commercial banks, GSEs cannot park their cash with the Fed. Unlike the banks, GSEs don’t earn (the current rate of) 25bp on reserves. Banks are flush with cash anyway, so there isn’t a lot of natural demand. So where does the FHLB cash go? Banks bid for it, then stash it with the Fed. The banks pay some FDIC insurance fees along the way. Still, it is better for the FHLB than letting it sit at the Fed, earning nothing. The government is allowing the commercial banks to arb the FHLB.

At the end of 2012, almost 75% of the Fed Funds sold came from the FHLB system members. Often you see Fannie or Freddie mentioned as being on the short end of the trade. From the post, “…While some have attributed lending activity to Fannie Mae and Freddie Mac, financial statements indicate that those firms reduced their fed funds participation in 2011 and haven’t been active in recent quarters…”

Fed Funds do serve an important role as the floating rate leg of the OIS market in spite of the Fed Funds market suffering from less and less liquidity. The Overnight Fixed-Rate Reverse Repo (or RRP for short) scheme has made matters worse for the Fed Funds market. GSEs can participate in RRPs, including the FHLBs. And they get a competitive rate with better credit risk (vs Fed Funds).

CCPs actively use OIS rates to discount curves and determine mark to markets, replacing even less liquid LIBOR curves. Theoretically this makes lots of sense. CCPs need to calculate the mark to markets based on achievable investment rates – and LIBOR was not cutting it. But will Fed Funds be much better?

As the Fed continues to move away from Fed Funds as a money market benchmark and closer to repo markets, will the CCPs shift gears again and discount using repo rates? Repos have traditionally been short term markets and extrapolating out years – which is what CCPs will need to mark long dated deals — won’t be very accurate. OIS rates have the advantage of themselves being centrally cleared, hence without the counterparty risk of LIBOR levels. Repo is collateralized, although (other than RRP) it is still a market with counterparty risk.

There are a lot of moving parts in the short end of the curve: IOER, Fed Funds, RRP, bilateral repo. If the Fed starts to move those relationships around, the first casualty will likely be Fed Funds and along with it OIS.