By investigating nonfungible tokens (NFTs), researchers from the University of St. Gallen and Swiss Finance Institute provide the first systematic study of retail investor behavior through asset bubbles. Given that NFTs are recorded in public blockchains, they are able to track investor behavior over time, leading to the identification of numerous price run-ups and crashes.

The study reveals that agent-level variables, such as investor sophistication, heterogeneity, and wash trading, in addition to aggregate variables, such as volatility, price acceleration, and turnover, significantly predict bubble formation and price crashes.

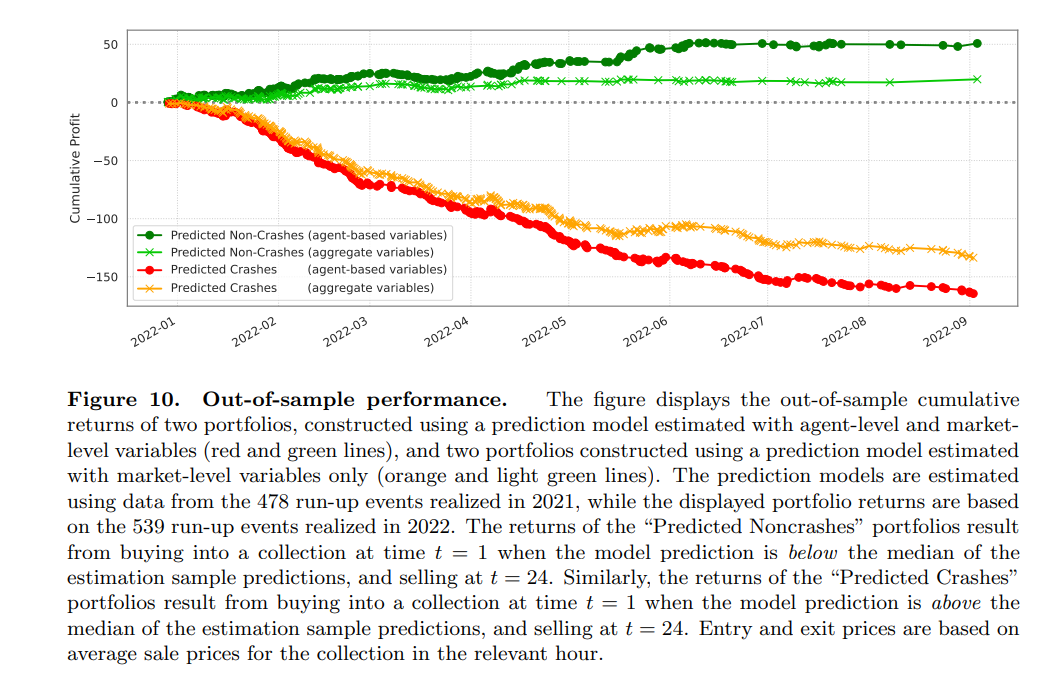

The first question addressed is whether crashes can be predicted using aggregate variables. Researchers find strong empirical evidence that collection-specific variables, rather than market-wide variables, predict price crashes. More precisely, the higher the volatility and acceleration of the price, the more likely it is to crash.

On the contrary, high turnover is associated with a lower probability of crashing, suggesting that, due to an inability to sell short, a lower concentration of optimistic investors and smaller liquidity risk predict smoother ex-post price adjustments. The picture that shines through this first analysis is that NFT bubbles are predictable, and they are not very dissimilar to those in equities since they share similar asset-specific predictors of price crashes.

Researchers also find that sophisticated investors consistently outperform others and exhibit characteristics consistent with superior information and skills, supporting the narrative surrounding asset pricing bubbles.

Of the findings, one is that the agent’s profitability is persistent across run-up events, suggesting that some agents possess more advanced abilities to perform consistently better over time. Another is that outperforming agents are distinguished in terms of (a) greater market presence, (b) financial leverage, and (c) sharper timing.

In addition to trading more volume and frequently, their activity spans multiple exchanges (crossmarket trading), they are more likely to provide liquidity and to trade in decentralized exchanges (DEX), like Uniswap, Balancer, or Curve, and they leverage up their positions to exploit profit opportunities and access arbitrage capital through decentralized lending platforms. Furthermore, these investors are more skilled in timing the bubbles, by both buying early into the run-up phase and selling close to the peak of the bubble.

Researches also analyzed wash trading at the aggregate and transaction levels, identifying suspicious trades empirically, finding that when wash trading is more pervasive ex-ante, ex-post crashes and liquidity deterioration are more likely.