Late in October, US regulators announced final rules for margining of non-cleared dereivatives. This topic has been controversial since it imposes margin requirements where there often weren’t any before and is the final leg in the process to collateralize derivatives exposures. It will create demand for eligible collateral that will flow down to the repo world.

A publication by PwC, “Derivatives: Clear road ahead for uncleared margin”, November, 2015 did a good job of reviewing the rules and looking at some of the knock-on effects. Non-cleared derivatives represent around 40% of the outstanding market – so we are talking about a major impact.

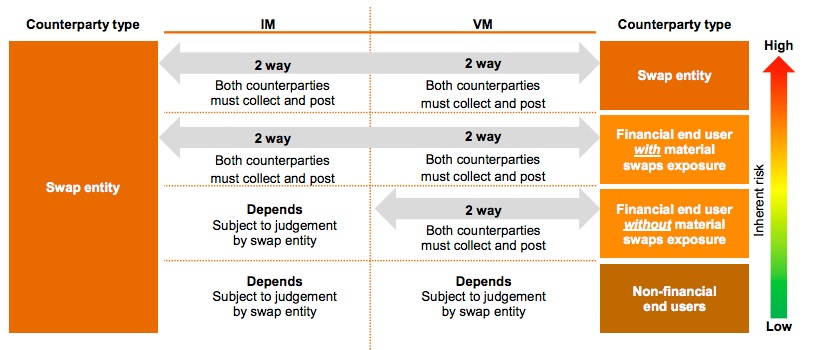

There was a lot of back-and-forth on the rules. Regulators were careful not to paint with too broad of a brush when calibrating Initial Margin (IM) and Variation Margin (VM) rules. The regulations are based on the counterparty type. The scale ranges from trades with other swap entities (most strict) to non-financial end users (most lax). From the report:

“…Because each of these counterparty types poses a different level of risk to the financial system, the final rule calibrates requirements to each type’s perceived risk level…”

Source: http://www.pwc.com/us/en/financial-services/regulatory-services/publications/assets/uncleared-margins.pdf

For IM there is a materiality threshold of $8 billion in exposure for trades with other swap entities and financial end users with material exposure. The $8 billion is calculated by taking “…the average daily aggregate notional amount of non-cleared swaps, non-cleared security based swaps, foreign exchange forwards, and foreign exchange swaps of the financial end user and its affiliates on a consolidated basis with all counterparties…”

One topic of particular relevance was what types of assets were eligible for VM. In cleared derivatives, VM is a zero sum game. One side’s surplus is another’s deficit. This forces VM to be limited to cash. CCPs standing in the middle are not in the collateral transformation business and need VM symmetry. But in non-cleared derivatives, dealers have more flexibility (although ultimately they may be doing collateral transformation to manage their cash flows). The new rules allow for VM to be in securities that are otherwise eligible as IM. From the report:

“…The final rule also increases the types of assets eligible as collateral for variation margin (VM) beyond only cash (as proposed in 2014). Non-cash assets that qualify as initial margin (IM) now also qualify as VM in trades between certain counterparties. This expansion alleviates industry concerns regarding potential collateral shortfalls…”

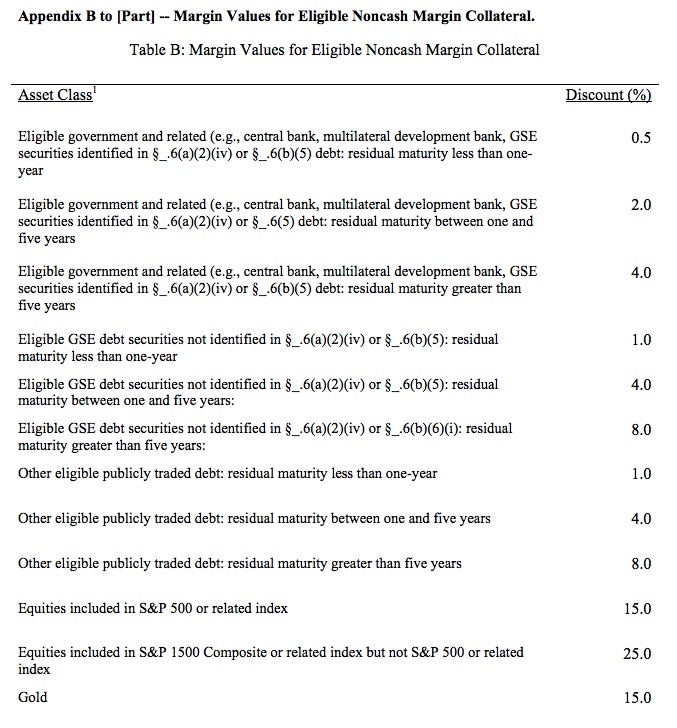

Securities utilized as VM will be subject to a haircut, ranging from 0.5% for government paper under a year to 25% for equities in the S&P 1500 (but not in the S&P 500). Below is a list from “Draft Final Rule and Draft Interim Final Rule – Margin and Capital Requirements for Covered Swap Entities”, Federal Reserve, October 21, 2015

Source: http://www.federalreserve.gov/aboutthefed/boardmeetings/swap-margin-board-memo-20151030.pdf

One other rule that will impact the collateral markets is the requirement that IM (although not VM) must be segregated with a third-party custodian and assets not re-hypothecated. This probably means setting up tri-party accounts – a process that can be time consuming. For derivatives dealers who used cash and securities to fund themselves, this could be a big issue. From the PwC report:

“…a custodian may hold cash collateral in a general deposit account if the funds are used to purchase collateral-eligible assets. This change is likely to increase the cost of collateral due to increased demand for eligible assets, and to force efficient use of existing collateral through optimization methods such as “cheapest to deliver”…”

While this sounds a bit confusing, we are told that making cash bankruptcy proof is difficult, so there will be a need to invest that cash in eligible securities. We wonder if the custodians will charge substantial fees to simply hold cash — consistent with the push to avoid deposits — and this will make securities more attractive. That demand created by investing the cash could take large chunks of eligible paper out of the market and may be the tipping point for the long feared collateral shortage.

Managing a derivatives desk without the use of client IM cash may cause liquidity issues for the dealers. Remember that the most common form of collateral for non-cleared derivatives, according to the 2015 ISDA Margin Survey, was cash (accounting for 76.6% of collateral received). Of that cash, 91.6% was eligible to be re-hypothecated and 82.2% was actually re-hypothecated. The cash is important for funding the desk. But if those assets held as IM are frozen at a custodian, they cannot be utilized. Since non-cleared derivatives are often hedged with cleared trades (which will continue to require IM) or non-cleared trades with other dealers (which will now have to be margined) derivatives dealers will need margin but won’t be able to recycle the client IM. Where is the IM cash (or securities) going to come from?

The shift to margining non-cleared derivatives de-risks the derivatives dealers by collateralizing exposures. But in the process, it may shift the dynamics of an already strained collateral market.

1 Comment. Leave new

Not sure if the margining of non-cleared derivatives trades will precipitate the long anticipated ‘collateral shortage.’ To date cleared derivatives have not moved the needle at all and they represent 60 to 70% of the market.

In the cleared space, cash (the current preferred IM option) is not left idle. CCPs invest these funds in short govies and HQLA repo. Cash margin on non-cleared transactions will most likely follow the same pattern in order to mitigate risk.

If there is a collateral shortage it will impact money funds and other short term investors who will not be able to find sufficient repo opportunities. Dealers will simply deploy their assets (in some cases transformed assets) in the most efficient manner.