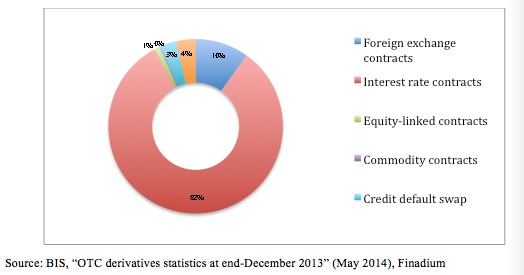

The global derivatives market is undoubtedly large. In the BIS “Statistical release: OTC derivatives statistics at end-December 2013” (May, 2014) the total derivatives market, as of the end of December, 2013, was reported to be a notional of $710 trillion. Of this, 82% ($584.364 trillion) were interest rate derivatives; foreign exchange contracts accounted for 10% ($70.553 trillion) and 3% ($21.020 trillion) were credit derivatives. Of note is that within the interest rate category, 79% ($461.281 trillion) were interest rate swaps.

Global OTC Derivatives market

Notional Amount of Derivatives

Source: BIS, “OTC derivatives statistics at end-December 2013” (May 2014)

Notional amounts make for good sound bites in the media, but the better statistics are “gross market values” and “gross credit exposures”. The BIS defines gross market value as “the cost of replacing all outstanding contracts at current market prices” and gross credit exposures as:

“…Gross credit exposures: Gross credit exposures are calculated as gross market values minus amounts netted with the same counterparty across all risk categories under legally enforceable bilateral netting agreements. In other words, the market value of dealers’ claims and liabilities are netted when they are claims on and liabilities to the same counterparty and the reporting dealer and the counterparty have a valid, legally enforceable netting agreement. The absolute value of amounts across counterparties is then summed. Gross credit exposures provide a measure of exposure to counterparty credit risk. However, they do not take collateral into account. Collateral would offset losses should the counterparty default…”

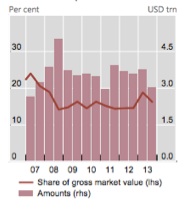

Year-end 2013 BIS figures show that gross credit exposure is 16.3% of gross market value – roughly equal to $3 trillion, less than 5% of total notional.

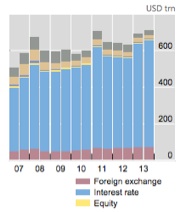

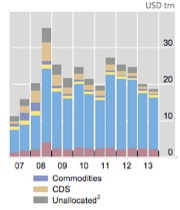

Gross Market Value of Derivatives

Source: BIS, “OTC derivatives statistics at end-December 2013” (May 2014)

Gross Credit Exposure of Derivatives

Source: BIS, “OTC derivatives statistics at end-December 2013” (May 2014)

Gross credit exposure is particularly important since it is before collateral is taken into consideration. But much of this exposure is collateralized — so the actual risk is even smaller. But when the press reports $710 trillion and compares that to GDP or other metrics, remember that it is not the real story.

The real risk is, first, how much is collateralized and how much isn’t. Second: can the collateral be realized if it need to be? And finally, when there are netting offsets it implies that the trades will economically offset each other, even in a crisis situation (and especially in a crisis..) This is something you won’t know until tested. One way to mitigate the correlation risk issue is to bucket transactions by asset class and collect margin netted within the bucket, but not across buckets. IOSCO has suggested this with non-cleared bilateral derivatives. FCMs might margin this way too.

We wrote about this topic last May in our post “More on why looking at derivatives notionals makes for great eye candy but not much else”