With interest rates in developed markets (DM) currently hovering at historic lows, a long-only exposure to DM sovereign fixed income may prove challenging in the years ahead. Style investing offers an alternative way of capturing returns uncorrelated with traditional assets, and has recently been extended to bonds.

In this paper, RavenPack researchers show how standard style factor performance can be enhanced with tilts based on real-time sentiment analytics. They construct cross-sectional, dollar and duration neutral long-short portfolios for value, carry, momentum, and defensive styles as benchmarks, and show that combining them into an equal-weighted strategy results in substantial portfolio diversification benefits.

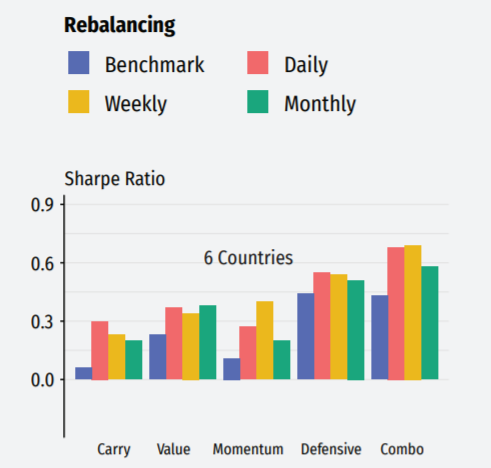

Researchers then apply economic news sentiment tilts to benchmark portfolio weights and find that this more dynamic style implementation significantly improves risk-adjusted performance across all four styles, in different country universes and at daily, weekly, and monthly rebalancing frequencies.

With weekly rebalancing, sentiment boosts the Sharpe ratios of the combined style strategies from 0.77 to 1.08 for the sample of 18 countries, and from 0.43 to 0.69 for the sample of the 6 sovereigns with the most liquid bond futures markets.