An April 16th article in Bloomberg, “Safest U.S. Debt Likely Only Collateral Covered in Repo Clearing” by Liz McCormick confirms what we already suspected: central clearing of repos will not address where the risk is — less liquid and more volatile collateral.

From the article:

“…Treasuries and U.S. government-related bonds are likely be the only collateral covered when financial institutions begin offering centralized trade clearing in the short-term market for borrowing and lending debt.…”

According to the article, the (U.S.) repo market’s $1.7 trillion in daily volume is 85% high quality paper. So any solution that covers that much of the market is a good idea, right? That is a good start, but it leaves out the risky stuff. This is where the stress was focused during the crisis and transmission of systemic risk was centered. Equities volumes may go higher during a crisis, but the volatility will hurt you if haircuts prove inadequate (think: flash crash). Corporates and EM paper simply stops trading in any size. If there are going to be fire sales, the cause célèbre of the Fed these days, it is likely to be in the other 15%.

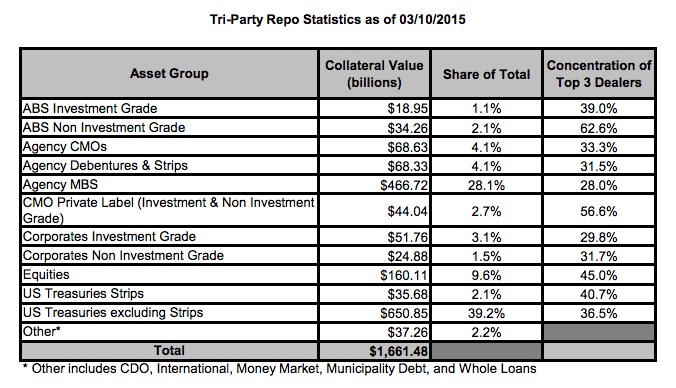

Looking at volume in tri-party repo (see below), just above 20% of the collateral value could be characterized as having episodic liquidity (a euphemism we like for “it’s only liquid if you are buying when everyone else is selling” – see our post from April 7th “ETF liquidity: will it be illusory in volatile markets?” and Howard Mark’s investor letter “Liquidity”). About half of the non-HQLA constitute equities. Non-HQLA isn’t a small market.

There is also some disturbingly high top-3 dealer concentration in the less than liquid sectors, but we digress.

Source: Federal Reserve, http://www.newyorkfed.org/banking/pdf/mar15_tpr_stats.pdf

(An observation about the tri-party numbers: Tri-party is driven by dealers financing their GC. For paper to end up in tri-party settlement, dealers need a cash lender willing to take it. So securities that can’t be financed in tri-party because no one will accept the paper won’t be in these figures, suggesting perhaps that these stats undercount that amount of illiquid/funky assets being financed by banks. Those instruments are left sitting on bilateral books funded catch as catch can. And we all know the sorry state of bilateral repo stats.)

Central clearing does not do well when the underlying is not liquid or the assets prone to being volatile. The slow uptake on less liquid/harder to reliably value derivatives contracts in central clearing, for example swaptions, is a reasonable parallel. A recent paper by LCH.Clearnet “Stress This House, A Framework for the Standardised Stress Testing of CCPs” highlighted “auction risk” as a potential issue in stress testing CCPs. We wrote posts on the paper, links are here and here. The paper described auction risk as:

“…Evaluating the risk of successfully auctioning defaulted clearing members’ portfolio of trades under each cover 2 scenario without exhausting the pre-funded default fund of the CCP…”

An auction has many facets to it, but fundamental is the ability to price the trades. The less liquid the assets, the harder that is.

From the Bloomberg article:

“…Whatever we clear needs to be liquid, easily priced and manageable in a default,” said David Weisbrod, chief executive officer of LCH.Clearnet LLC, the U.S. unit of LCH.Clearnet…”

In all fairness, central clearing of repo is not really new. DTCC has been centrally clearing repo for a while, albeit just for banks & broker/dealers. In a move that will change market dynamics, DTCC is expanding to include some of the buy-side as well. LCH has been centrally clearing repo in Europe for years. There are other organizations working on it too; CME recently hired Kevin Walker from Barclays to spearhead their repo CCP effort. And OCC, we have heard, is working on central clearing of equity financing trades too.

It is not a surprise that repo clearing will be focused on HQLA. But the market and regulators should not declare victory and go home. Solutions still need to be found for those other markets. Maybe capital surcharges for repo books – a potential solution talked about last year but not in the news lately – can target less liquid books? Or perhaps a public/private bailout resolution fund to take over those illiquid trades until some semblance of liquidity comes back (which could be measured in months…)?

Some may say the idea of imposing a couple day stay on liquidations, OLA style, will fix the market. But it will take more than 48 hours for stressed markets to right themselves and in the meanwhile repo dealers will have hedged themselves, depressing markets anyway.

Liz also wrote a related piece in Bloomberg on April 13th “Financial Firms Move Closer to Central Clearing in Repo Market”. It is also worth a read.