With continuing economic and political challenges showing no signs of easing, financial resource efficiency is more critical than ever, write LSEG Post Trade’s James Upton, COO of LCH RepoClear and Collateral and Liquidity Management (CaLM), and Konstantina Travlou, LCH RepoClear Commercial Director. This article describes how access to LCH RepoClear, LSEG Post Trade’s repo and cash bond clearing service, can help market participants optimise their resource efficiency, increase access to liquidity, and ultimately reduce their costs.

Shockwaves continue to reverberate around the world. Changing interest rates, inflationary pressures and political uncertainty have created a challenging environment. The ability to adapt and respond quickly, while in parallel positioning for future structural market changes, is critical.

In this context, market participants, including dealers, official institutions and buy-side participants, are laser-focused on costs. Now more than ever, the cost of a transaction is assessed versus the cost of funding, balance sheet consumption and the impact on regulatory ratios, making the optimisation of financial resources key to effective decision-making. As a result, post-trade offerings – and, in this context, repo clearing – have become increasingly important for market participants.

How does RepoClear meet the market’s needs?

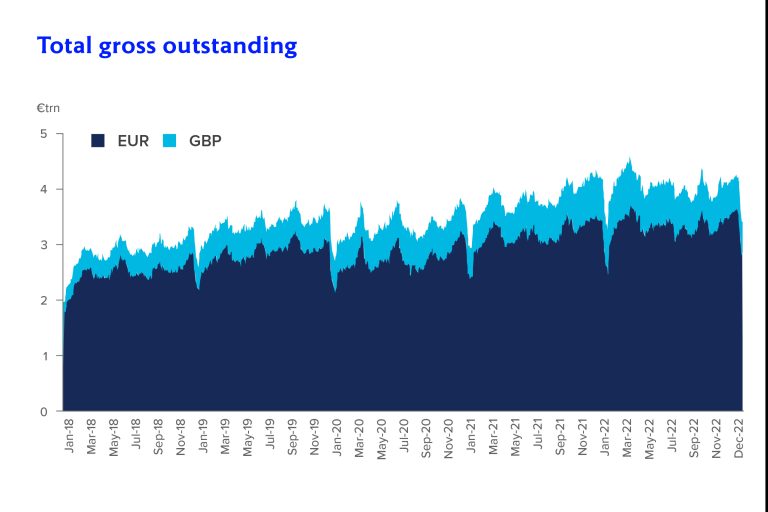

Market participants recognise the importance of access to the largest cleared liquidity pools. This is demonstrated by figure 2.14 from the ICMA European Repo Market Survey, published in December 2023, which illustrates LCH RepoClear’s outstanding value – especially during periods of heightened market volatility.

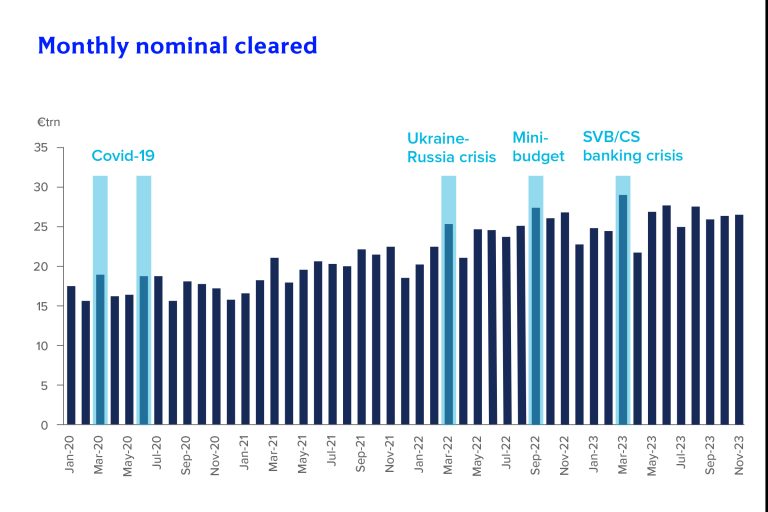

This access allows participants to benefit from best-in-class risk management, standardised operational and settlement processes that follow market best practice, and a lower risk weight (with beneficial regulatory treatment) from facing a CCP compared to a standard market counterparty. LCH RepoClear’s resilience and liquidity during recent periods of market volatility is demonstrated by the accompanying bar graph, which shows the increase in cleared volumes during key events that have impacted the market.

Source: LCH

Source: LCH

The importance of access to cleared repo is highlighted by the spike in UK gilt yields in September 2022, during which liability-driven investment funds (LDIs) came under severe stress. At this time, levels of liquidity in LCH RepoClear were incredibly resilient and, in contrast to the non-cleared environment, the service did not experience any failed margin calls.

Focus has now switched to the learnings from the mini-budget event, and several significant developments, such as Andrew Hauser, the Bank of England’s former director for markets, proposing a ‘liquidity lifeline’ lending facility for non-bank financial institutions (NBFI).*

Within the right construct, liquidity lifeline solutions have the potential to use CCP infrastructure for improving how liquidity is directed to precisely where it is required. Other recent regulatory publications, such as the PRA’s fixed income financing thematic review,** have highlighted the lack of haircuts in non-cleared repo versus cleared repo, leading to an increase of the risk within the overall system, and have considered the arguments to ‘level up’ between the two.

Amid this backdrop, one trend is emerging: there will be an expansion of the number and range of market participants that will clear their repo transactions. LCH RepoClear is well positioned for this future state by already increasing access to clearing, enhancing its product offering, improving risk management, as well as expanding its global membership.

Increasing access to clearing by:

1. Diversifying our membership At LCH, we are continuing to develop our buy-side Sponsored Clearing models to extend and diversify the LCH RepoClear membership, with the objective of introducing a ‘virtuous circle’ for the buy-side and the sell-side. We strongly believe that attracting an increasing range of eligible participants to the CCP further deepens the liquidity pool and provides secure and stable funding access to all eligible firms.

Additionally, by alleviating pressure on banks’ balance sheets, extra capacity can be released to better support a larger number of buy-side firms, hence strengthening overall market stability.

Equally, regulators in jurisdictions served by other Repo CCPs are focused on the benefits of repo clearing, with the SEC recently announcing that clearing of US Treasury repo trades will be mandatory from 30 June 2026.

Our existing Sponsored Clearing product, which caters for pension funds, insurance funds (in both LCH SA and LCH Ltd), LDI funds and money market funds (available for gilts in LCH Ltd only), continues to adapt to market dynamics via the introduction of subtle changes, aimed at reducing costs for sell-side dealers, the buy-side and their Sponsors. These changes are built within the largest pool of cleared repo liquidity in the UK and Europe.

However, we are conscious that there is a need and demand to extend the sponsored model even further, and are planning, subject to regulatory approval, to extend access to new buy-side entities, including selected hedge funds, in 2024.

2. Expanding our international footprint LCH has a wide and global membership. The more globally diversified we are, the stronger, deeper and more stable our liquidity pool is for our members and clients. LCH RepoClear welcomes members from the UK, Europe, Canada and Japan, and continues to explore memberships in other jurisdictions.

3. Enlarging our product offering

We have engaged closely with all stakeholders to improve and widen our product offering. This includes General Collateral (GC) Clearing, where interest rate hikes and other market changes have led to banks needing to finance their inventories via repo and through greater use of GC financing products.

LCH RepoClear has been anticipating changes in the macroeconomic environment and the market’s need to be able to source liquidity using GC products when cash is scarce. As a result, we have delivered continuous improvements to €GCPlus, our GC triparty basket repo clearing service, offered in collaboration with Euroclear and Banque de France.

Improvements include the merger in July 2023 of €GCPlus with LCH RepoClear’s Euro debt service, which incorporates individual ISIN clearing. Removing the silos between these services allowed €GCPlus liquidity to combine with LCH RepoClear’s €3.4 trillion Euro debt liquidity pool unlocking additional Euro debt netting opportunities for members, as well as enhanced collateral management capabilities – all through a single clearing service.

Developing our offering does not stop there. To further accommodate our members’ needs, a new range of GC baskets was delivered at the end of Q4 2023, including our Green, GovSSA and Italian baskets. More country specific baskets will be delivered in 2024, facilitating netting between GC and specific activities on the most frequently widely traded European debts.

LCH is constantly looking to enhance its services and ensure efficiency. Working with members, further improvements will be delivered over the course of 2024.

4. Making refinements to risk management models

As a CCP, LCH is required to conservatively calibrate its margin models with the primary aim to ensure financial stability in line with our risk management requirements. It is crucial to have a stable and anti-procyclical model that is well understood and does not destabilise the market during periods of stress, whilst ensuring the proper level of protection to the CCP’s membership. It is for these reasons that in 2022, a value-at-risk (VaR)-based Initial Margin (IM) framework was put in place for Euro clearing in LCH SA reaching that goal, but also allowing for further cost optimisation. Additionally, for Gilt clearing, LCH RepoClear has recently introduced (in November 2023) a new IM model in LCH Ltd, which aims to deliver margin efficiencies while adhering to LCH’s high risk management standards.

5. Staying committed to our open access principles

We provide our members with choice, so they can connect to the trading venues and settlement locations that make the best sense for them; are aligned to their strategic needs; help them optimise their costs; and facilitate their access to liquidity. Examples of this include LCH SA’s recent connections to GLMX and BrokerTec Quote, expanding the range of execution options available to both the sell-side and buy-side.

6. Extending the scope of eligible collateral

LCH is continuously working to extend the scope of eligible collateral it accepts to cover margin liabilities. This gives our members more choice regarding the collateral they can post to us, which facilitates the management of their liquidity requirements and helps them reduce costs. Intelligent collateral management, where there is an intense focus on costs, is of paramount importance – and as the Markets’ Partner, we are here to deliver continuous extensions to collateral eligibility and thereby help our members achieve their objectives.

Recently at LCH SA, the scope of acceptable non-cash collateral was extended to a broader range of agency, supranational and government securities, with the addition of CADES, European T- bills and Spanish inflation bonds. LCH is planning to add new non-cash collateral types in 2024.

Conclusion

At LCH RepoClear, we understand that cost optimisation, resource efficiency and access to deep liquidity is more essential than ever. In an environment of ongoing interest rate, inflationary and industry developments, cleared repo is coming into greater focus as a key tool to achieve these goals for both the sell-side and the buy-side.

LSEG Post Trade, LCH and LCH RepoClear stand ready to support members and clients on their journey towards clearing. For further information on LCH RepoClear, please contact rcsales@lch.com.

Footnotes:

*Filling Gaps In The Central Bank Liquidity Toolkit, Andrew Hauser, September 2023

**PRA Fixed Income Financing Thematic Review October 2023

This article was sponsored by LCH.