Entities in the scope of phases five and six of the Uncleared Margin Rules (UMR) will need reliable and efficient access to cash in order to manage their daily OTC derivatives collateral obligations. Yes, the current coronavirus pandemic has delayed the deadlines, but the challenge has not disappeared. Impacted firms need to take this time to better prepare for compliance and take the opportunity to put a complete solution in place. A guest post from Eurex.

While firms may be able to sell assets to bilaterally raise cash, CCP cleared repos offer a way to cheaply monetize assets. Almost unique among financial assets, liquidity on EurexRepo’s GC Pooling service is inversely correlated to the excess liquidity offered by the European Central Bank, and thus fares well during volatile market periods.

Uncleared Margin Rules have created substantial questions about collateral and where margin will come from. While the Basel Committee on Banking Supervision has mandated an expanded set of eligible collateral for UMR, market participants have their own preferences. In practice, Initial Margin (IM) can be posted in cash or securities, but for Variation Margin (VM) there is a steady trend in bilateral collateralization of posting in cash only because it is easier to manage and account for. So long as cash is required as collateral, market participants will need to be prepared to source liquidity on short notice, especially in the case of market volatility.

Theories abound on how asset managers will meet their cash requirements for VM. Some think this cash will be generated by securities loans, while others think that asset managers and other in-scope firms will need to sell assets to generate cash, creating a drag on their portfolio. Still others expect that dealers will intermediate a bilateral repo transaction as part of their broader collateral services.

At Eurex, we offer another solution based on the argument that the only reliable liquidity source is one that performs during volatile periods, especially when bilateral markets may struggle to deliver either natural buyers or financing options. GC Pooling, a cleared repo product, meets these requirements and has shown durability over time. Cash rich investors, including recipients of cash VM and Money Market Funds, can also benefit from the increased balance sheet capacity, as well as typically better investment rates, available through centrally cleared reverse repos.

Volatility vs. liquidity

Volatility and liquidity are often unfriendly bedfellows. In 2008, a large part of the trouble during the Global Financial Crisis was the freezing of credit markets: buyers had lost enough confidence due to market volatility that market makers simply had to step back. Similar situations have occurred every few years since, including in March 2020 as the coronavirus led to widened spreads and immobile markets for less liquid fixed income assets. Indeed, a March 9, 2020 Bloomberg article noted liquidity gaps in Italian, Portuguese, Indonesian and Mexican government bonds:

Investors say it is becoming increasingly difficult to trade due to the extent of swings on a day that saw 30-year Treasury yields drop the most since the 1980s and a fall in US stocks so sharp that trading was halted minutes from the open. Even before today financial conditions were tightening at the fastest pace since the 2008 crisis.

While financing markets tend to behave rationally, exceptional central bank and government intervention in the form of Quantitative Easing, combined with Basel balance sheet regulation, has made the provision of liquidity less predictable. Hedge funds talk about buying liquidity or paying in advance to get access to cash pools on a contingent basis. However, not everyone is so fortunate and, at a certain point, contingent liquidity can get expensive or disappear.

Not only does volatility decrease liquidity, it can also raise VM requirements right when market participants are struggling to find the liquidity they need to meet margin calls. Traders have learned this lesson the hard way on multiple occasions, including in the case of MF Global’s ultimate failure due to increased margin calls on Italian bonds. There is no such thing as guaranteed liquidity, and volatility makes the situation worse at almost every turn.

The GC Pooling experience

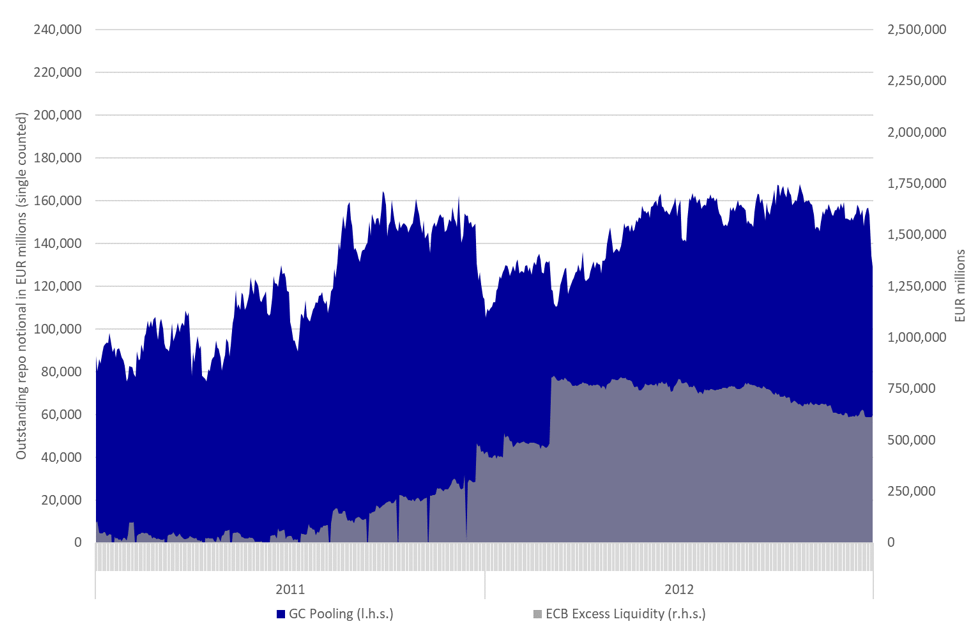

At Eurex, we have watched the relationship between volatility and liquidity closely, especially during stressed periods. For example, Eurex Repo`s centrally cleared triparty repo market segment, GC Pooling, has provided consistent liquidity over the last 12 years, even during times of extreme market turmoil (see Exhibit 1). In particular, the 2012-2014 southern European sovereign debt crises greatly reduced the availability of bilateral repo funding capacity for certain banks and against certain securities. Instead, GC Pooling repo volumes surged as banks recognized that secured funding via the CCP would enable participants to raise funding more reliably and against a wider set of collateral than in bilateral repo markets. Volatility proved its winning power over bilateral liquidity once again. Since then, we have continued to see that GC Pooling trading volumes have been significantly higher than, for example, EONIA during problematic month-, quarter- and year-ends. When volatility is high and bilateral liquidity suffers, CCP-based liquidity in the GC Pooling universe excels. Today, more than 160 financial institutions have access, including commercial banks, central banks and supranationals, selected government financing agencies and buy-side entities.

Exhibit 1: GC Pooling vs. ECB excess liquidity

Source: Eurex

Learning from the US

As firms included in the UMR regulation need to find cash to post as VM, they will work through the normal avenues: cash on hand, then bilateral transactions bundled into the cost of the derivative, and potentially selling assets. Not all these choices are viable every day, however. GC Pooling represents an option, not just for liquidity crunches, but also for treasurers’ general usage.

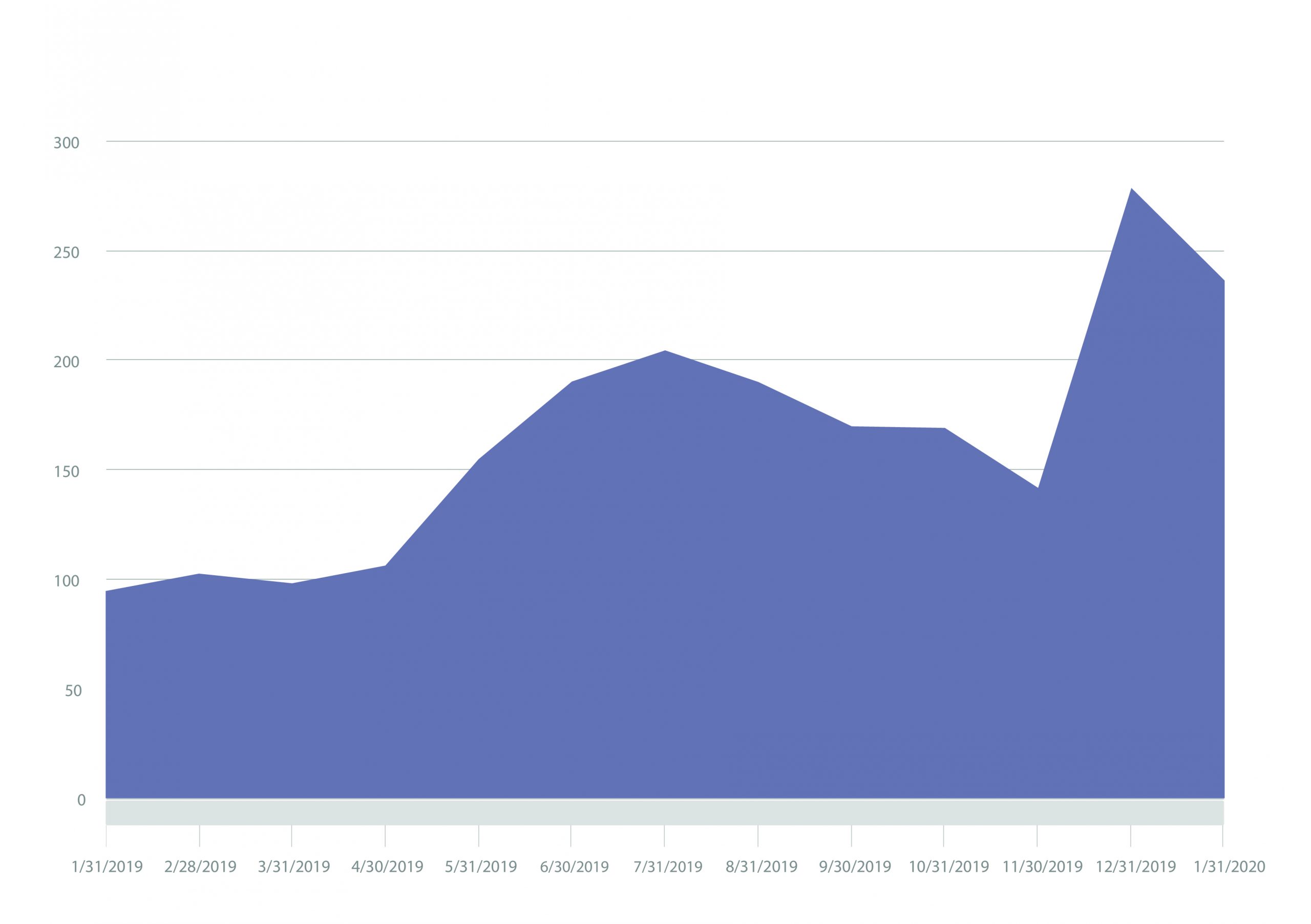

European market participants in particular have lessons they could learn from sponsored repo in the US. While US firms have turned to sponsored repo as one support for liquidity, European firms have not been as engaged. In the US, the majority of major money funds now participate in sponsored repo, with liquidity at US$236 billion in January 2020, according to data from the US Office of Financial Research (see Exhibit 2). This is more than twice the money fund volume recorded the prior year. Even during the tumultuous week of September 16, 2019, sponsored repo saw measured declines along with the broader repo market, but money funds continued their active engagement. The following month, FICC reported a high-water mark of $400 billion in transactional volume.

Exhibit 2: US money market fund exposure to FICC, US Treasury repo

(US$ billions)

Source: US Office of Financial Research

In Europe, however, market participants have been slower to adopt cleared repo strategies, even when the US divisions of the same companies are active on FICC. In some cases, according to our conversations, the European division had not known what the US group was doing. Now, however, UMR, along with the regulatory alphabet soup of SFTR, CSDR and NSFR, is forcing a rethink at European asset managers on how they source and place cash, standardize execution and execute on straight-through processing. This is no longer a nice-to-have, but rather an imperative as the current coronavirus crisis is highlighting again. If they are going to continue trading OTC derivatives, European asset managers recognize they will need access to larger pools of liquidity than they have now. GC Pooling on Eurex Repo offers a crisis-proven option for the market.

About the Author

Frank Odendall is Senior Vice President Head of Securities Financing Product & Business Development at Eurex. Frank started out at J.P. Morgan in London, developing tailor-made hedging structures for corporates, public sector entities and pension schemes using interest rates swaps and credit derivatives. At Deutsche Börse Group, Frank initially helped develop the client-centric interest rate swap clearing offering at Eurex Clearing which, at the time, contained the first individual client segregation model. After that, he worked in the listed derivatives product development group in Europe and Asia working closely with asset managers and banks on innovative products, e.g. Money Market Futures hedging repo interest rates. Since 2019, Frank is responsible for the securities financing product and business development at Eurex.

Frank Odendall is Senior Vice President Head of Securities Financing Product & Business Development at Eurex. Frank started out at J.P. Morgan in London, developing tailor-made hedging structures for corporates, public sector entities and pension schemes using interest rates swaps and credit derivatives. At Deutsche Börse Group, Frank initially helped develop the client-centric interest rate swap clearing offering at Eurex Clearing which, at the time, contained the first individual client segregation model. After that, he worked in the listed derivatives product development group in Europe and Asia working closely with asset managers and banks on innovative products, e.g. Money Market Futures hedging repo interest rates. Since 2019, Frank is responsible for the securities financing product and business development at Eurex.