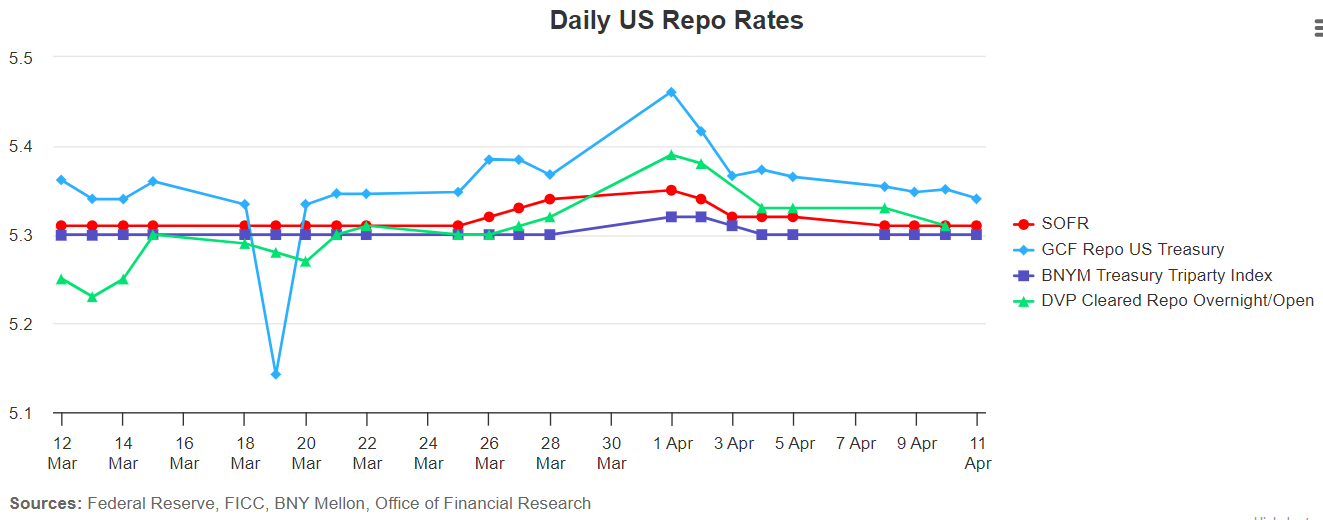

Something odd just happened in US short-term funding markets: a benchmark interest rate suddenly fell precipitously on March 19 before bouncing back up the next day. The drop, which has garnered little attention outside Wall Street trading desks, happened in a corner of the repurchase agreement market, or repo, where firms borrow funds from investors against Treasuries.

That day a key repo interest rate, called the Treasury GCF Repo Index, fell to 5.142%, a significant drop from its previous day’s print of 5.334%. The volume of transactions went up $57.64 billion from $31 billion the previous day.

Behind the drop was a large, single trade late in the day involving a big player, according to three market sources and a review of publicly available transaction data. The trade was in the mid-$20 billion range at a 5% rate and happened sometime after 1 pm, according to two of the sources.

The trade was odd as the bulk of repo market activity happens in the morning. A big investor was likely stuck with a huge amount of cash and needed to get it off its books, the sources said. They attributed it to bad collateral management.