Securities lending market dynamics are changing, driven by ongoing efforts at financial institutions to improve balance sheet efficiencies and Basel III Endgames around the world that create further capital and operational requirements. These factors, along with regulatory mandates like the move to T+1 settlement and securities lending reporting under SEC Rule 10c-1, mean that beneficial owners should be prepared to review their agent lender relationships, consider their lending parameters and investigate new routes to market.

Securities lending is still a relationship business, but for the majority of trades, borrowers want counterparties that offer the best balance sheet outcomes and easiest operational efficiency. This is a far cry from the securities lending market of a decade ago. The new model has become sufficiently engrained that the cost of a loan as measured in rebate rates or fees may now be a secondary consideration; if the balance sheet treatment is right and processing is automated, then agents with the best operations and fair market rates may win the business over competitors.

RWA for counterparty exposures

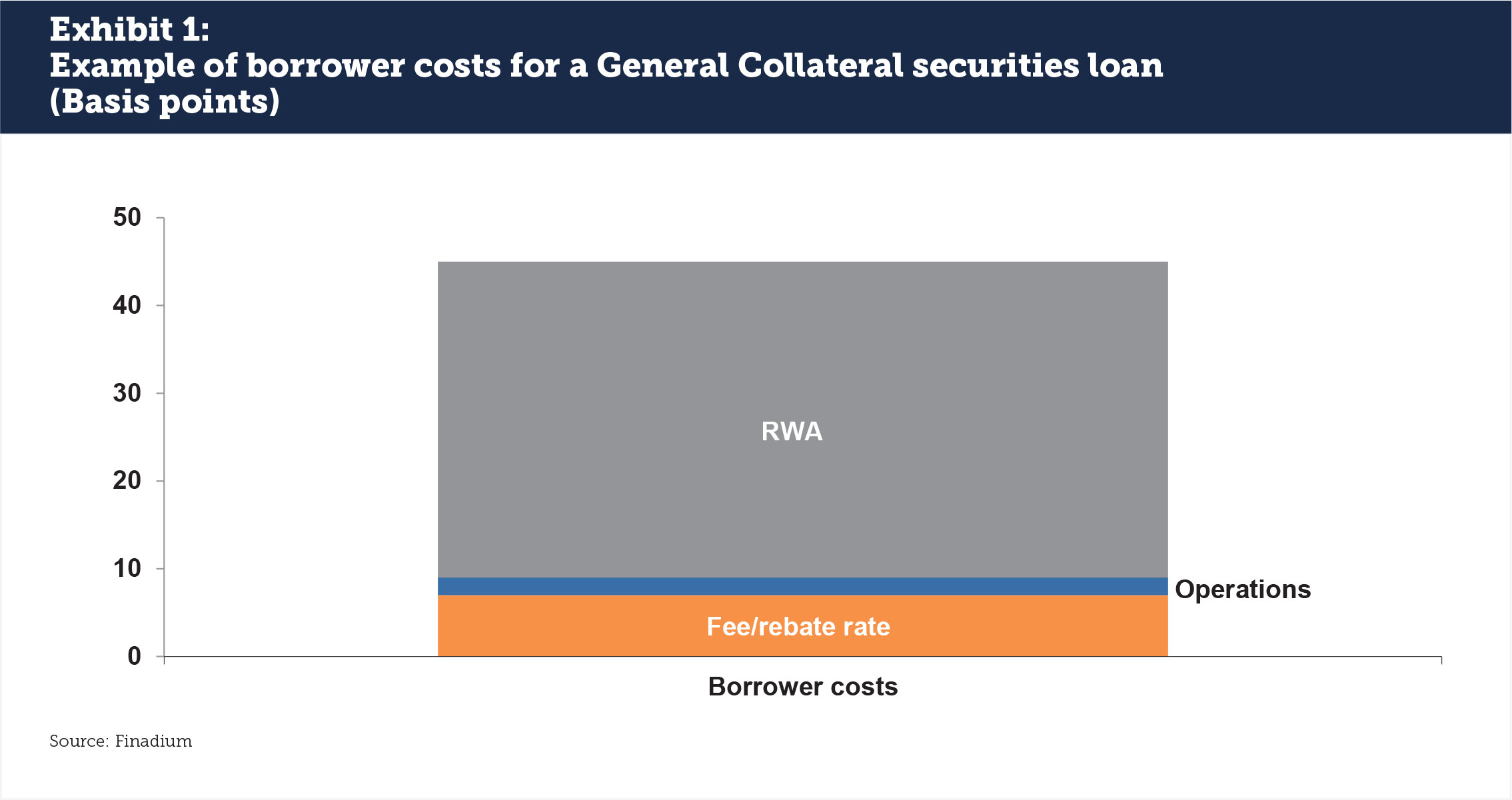

In an example of a General Collateral (GC) securities loan, the risk-weighted asset (RWA) cost of counterparty credit exposure to a borrower can be more expensive than the actual rebate rate or fee paid by the borrower to the lender, with operational costs as an additional factor. If a GC loan fee is 7 bps, RWA could reach 36 bps for a costly counterparty, or more than 5X the loan fee (see Exhibit 1). If there isn’t a lower RWA alternative, then these costs will likely be recaptured by charging end-borrowers or the market may shrink as borrowers decide not to trade. For hard to borrow securities with higher loan fees, the lower the relative impact of RWA and the more palatable that cost becomes. US equity GC under 20 basis points represents around 60%-70% of balances, according to EquiLend. While a much smaller percentage of industry revenues, it remains an important part of the business’s economics.

RWA charges have been a consistent focus for many financial insitutions. This figure rolls up to Basel III Liquidity Coverage and Net Stable Funding Ratios and is a central factor in how they assess the cost of every trade with every counterparty. RWAs can vary by beneficial owner, and some institutions now ask to borrow from beneficial owners that they have determined are in the lowest RWA categories, a practice known as smart bucketing, which can potentially separate out different borrowers into different allocation methodologies in agent lender queues.

The high cost of RWA for borrowers may be thought of as lopsided economics. After all, shouldn’t the cost of the loan be the most important deciding factor for borrowers in a competitive market? While the answer is yes on paper, in practice these other costs faced by regulated entities are more important. As a result, agent lenders and beneficial owners have worked to adjust their programs to continue to be seen as a preferred counterparty. For Fidelity Agency Lending (FAL), this means investing to reduce operational frictions both pre- and post-trade through automation, connectivity, and developing trade structures that are attractive for all involved parties.

Changes to RWA and beneficial owner control of the process

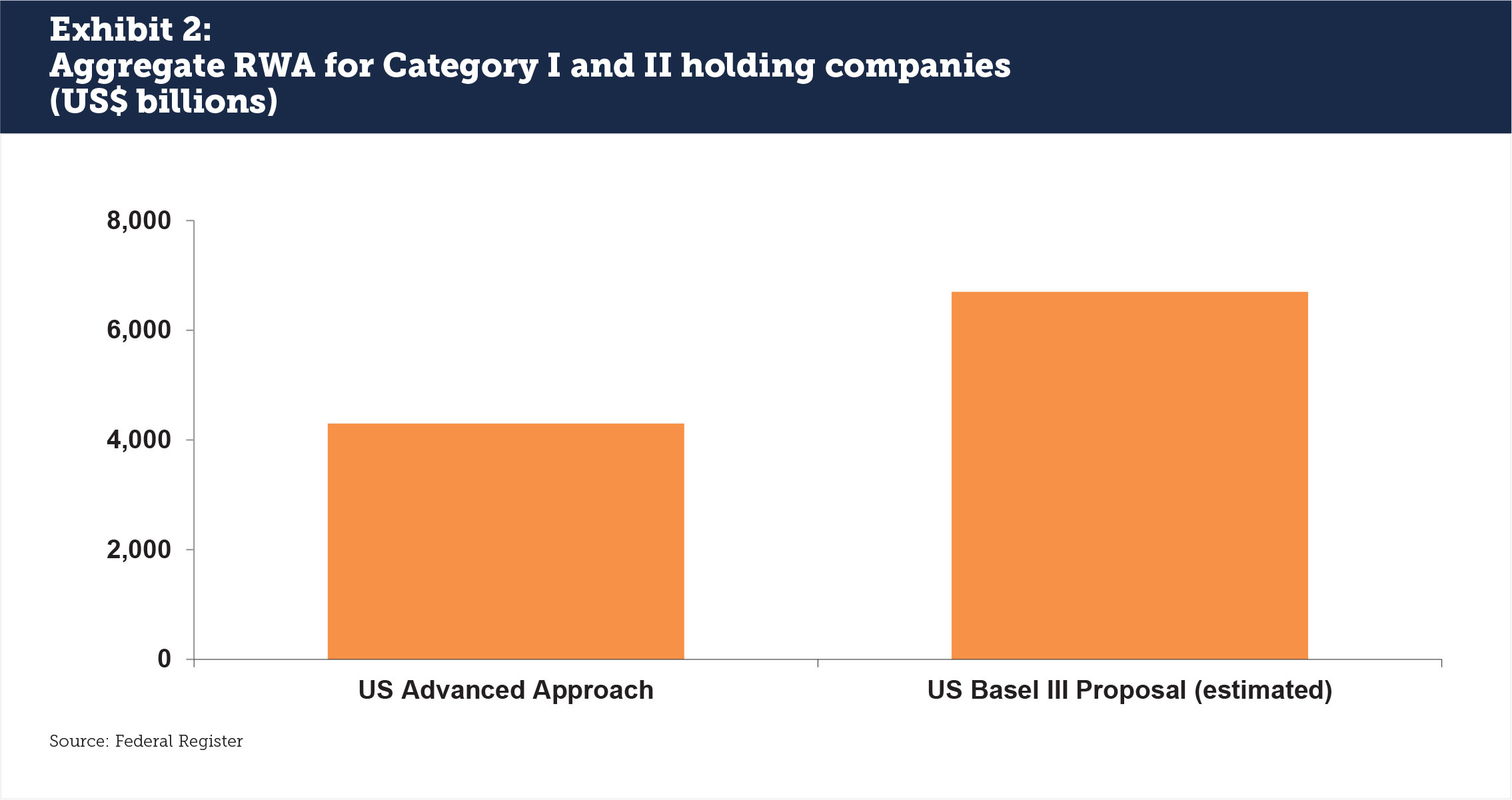

Beneficial owners in securities lending have some flexibility in the RWAs that are assessed to them by financial institutions, as it relates to securities lending transactions. At the highest, most expensive tier, unrated counterparties may be assessed a 100% risk weight. At the lowest, certain sovereign entities have a 0% risk weight. The difference is significant for financial institutions when using the Basel III Advanced Approach to measure credit risk today. The US proposed Basel III finalization rules substantially reduce borrower options for assessing their own credit risk. According to the proposal, RWA costs for larger institutions that typically use the Advanced Approach would increase by $2.4 trillion (see Exhibit 2). This is a substantial sum.

Beneficial owners are not locked in to one credit rating however. A variety of options exist to mitigate this cost for regulated borrowers including use of the DTCC’s National Securities Clearing Corporation (NSCC) Securities Finance Transaction (SFT) Central Counterparty (CCP). The rules for Qualifying CCPs like NSCC provide a 2% risk weight; beneficial owners in high risk weight categories that opt to use the CCP can lower their RWA for borrowers accordingly. While other costs are introduced including a requirement to post margin to the CCP, Finadium analysis suggests that in many cases the trade-offs are worth the effort for lenders and borrowers alike, but all require that agents and clients conduct their own reviews. Some lenders are also looking at getting their own credit ratings from existing ratings agencies.

The NSCC SFT CCP for US equity securities lending has low volumes so far. Still, Fidelity Agency Lending sees this as a potential opportunity worth further exploration and consideration, and analysis of the economics. FAL operates as part of National Financial Services, which is already an NSCC member. FAL may participate as an agent lender on the CCP or a sponsor, a popular model on DTCC’s FICC Sponsored Repo platform. Both options can benefit FAL clients by potentially making their assets more attractive to borrowers. According to Doug Brown, head of business development at FAL, “While the current CCP models do not work for our client base today, we are discussing new structures that could potentially be a game changer. We continue to test with our counterparties various options that can help reduce RWA costs across the industry.”

New calculations for Basel III operations costs and T+1

While there are no meaningful RWAs for operations today, borrowing decisions are already made based on trade efficiencies. The cost of trade break fails is a frequent frustration for both lenders and borrowers; the more that these costs can be eliminated due to efficient trades processing, the more that lenders may be seen as preferred counterparties by borrowers as a means to generate significant savings in time and resources. Justin Aldridge, head of Fidelity Agency Lending, notes that “we have invested heavily in automating tasks like corporate actions, reconcillations, and real-time settlements in order to minimize extra cost in the securities lending process for ourselves and our clients.”

More tangible costs are on the way for operational risk, which is a new element in the proposed US Basel III Endgame rules. Although Federal Reserve Chair Jerome Powell said in March 2024 that he expects a broad overhaul of the proposal, some level of operational risk assessments will potentially remain. According to the Bank Policy Institute, this could cost impacted financial institutions an estimated US$1 trillion in RWA assessed across a variety of institutional and retail fee-based lending activities. The higher the RWA, the more capital a financial institution must hold to support its business and the less business it can actually conduct.

In securities lending, faster loan processing post-trade means that borrowers may have less outstanding exposure and can calculate their RWA more accurately on an intraday basis. Securities lending is just one area that these borrowers are focused on to achieve this goal, with regular reviews of collateral and operations-related costs. Agent lenders with the technology to support fast processing of securities lending loans may offer direct help to borrowers in reducing operational RWA charges. The more efficient the lender, the more efficient the borrower and the lower the RWA cost.

The introduction of T+1 settlement in the US, Canada and Mexico at the end of May 2024 also means that operational efficiencies take on a new importance. Lenders must be able to recall their securities for timely delivery of sold positions, which means that borrowers must return their positions as well. This will be most challenging for hard to borrow equities and international securities in ETFs that operate on different settlement cycles. Lending agents with the most effective operational processes can best support their clients in meeting T+1 obligations.

Fidelity Agency Lending has delivered on a settlement infrastructure that minimizes operational hurdles today and is focused on keeping RWA operational charges low going forward. This already helps borrowers meet regulatory deadlines for Rule 204 short selling rules by settling trades in seconds. Fast settlement also speeds up delivery of cash collateral for reinvestment purposes; in a non-0% interest rate environment, this represents a tangible benefit for clients.

Agent lender partnerships

While the future environment for beneficial owners lending to certain types of borrowers offers some challenges, there are also routes to lessen new cost impacts and potentially make individual asset pools more attractive than today. FAL’s Brown notes that part of the choice offered to beneficial owners is selecting an agent lender that can align and support the types of clients that fit best into the overall program. FAL’s primary focus is on the ’40 Act Fund sector. By supporting fast settlement, Straight-through Processing and the evaluation of RWA mitigation opportunities like the NSCC SFT CCP, FAL believes that it can best support its clients through the next evolution of securities finance market dynamics.

This article was commissioned by Fidelity Agency Lending, a division of Fidelity Capital Markets. For more information about Fidelity Agency Lending, please visit https://capitalmarkets.fidelity.com/fidelity-agency-lending.

Fidelity Agency Lending® is a part of Fidelity Capital Markets, a division of National Financial Services LLC, a member of NYSE, SIPC. Clearing, custody or other brokerage services may be provided by National Financial Services LLC, or Fidelity Brokerage Services LLC.

Finadium is an independent entity and is not affiliated with Fidelity Investments.