The Regulated Liability Network (RLN) is positioning as a financial market infrastructure (FMI), operating a shared ledger with central bank money, commercial bank money and electronic money on the same network. It would have a number of partitions for each regulated entity to be able to record, transfer and settle their liabilities.

The purpose of the RLN is to create a new substrate for sovereign, regulated currencies that enables innovation around commercial bank money and is not just limited to central bank liabilities. Some of the core features of RLN would mean that it is “always on”, “programmable” and can support multi-asset settlement, thanks to the adoption of distributed ledger technology (DLT).

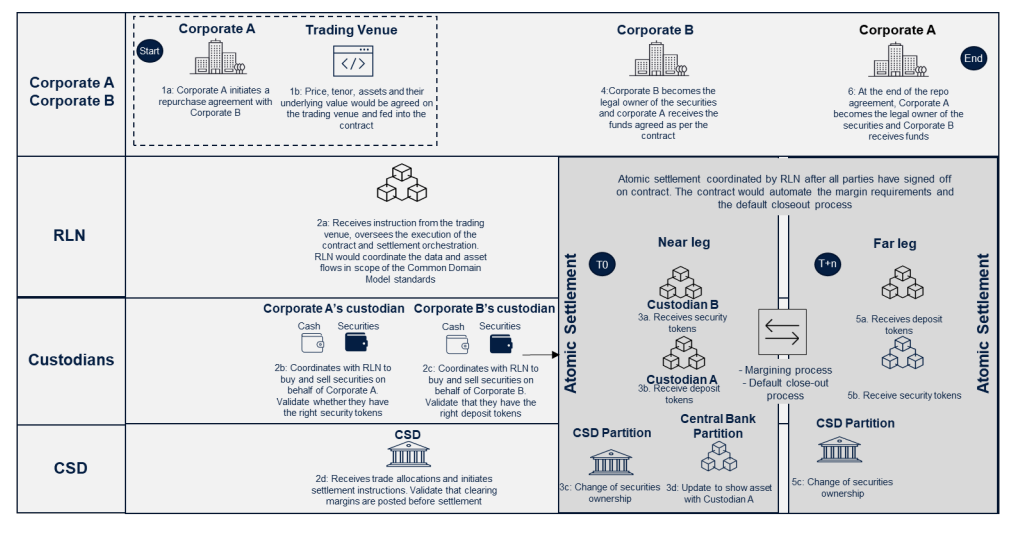

Repurchase agreements

One of RLN’s use cases relates to securities settlement in wholesale markets. It explored a bilateral cleared repo transaction between two corporates, with a commitment to buying back securities at a pre-agreed future date at a pre-agreed price.

RLN would oversee the execution and settlement of the transaction but would not be a trading facility. In this case, the orchestration and programmability functions that RLN offers, could provide the following benefits:

- 24/7 Liquidity: The use case could enable 24/7 availability and settlement windows, which would potentially enable 24/7 access to liquidity for both buy and sell-side firms. This could open intra-day repo markets, as well as other securities transactions, help firms manage low points and reduce the need for buffers. For example, firms may be able to improve operational efficiency and reduce uninvested cash or unfunded securities positions at the end of the traditional settlement window.

- Settlement efficiency: Settlement benefits for this use case could be maximised due to high-frequency multi-party and multi-asset settlements. Settling cash and assets atomically together has the potential to enhance the settlement process. There could even be a potential in certain repo transactions to position assets before a trade can be entered into the application, which could help mitigate and/or eliminate settlement failures.

- Simplification of process: RLN has the potential to simplify the process by programming various steps into the smart contract and coordinating the movement of money. By having a node on the RLN, other financial institutions (such as trading venues, clearing houses and Central Securities Depository’s (CSDs)) can participate in this streamlined process. For the repo use case, by consolidating all flows onto a unified platform, RLN enables efficient netting and simplifies the settlement of diverse securities.

- Automated margining: There is potential to greatly enhance the margining process by automating various steps (especially for non-centrally cleared trades) via the smart contracts, such as pricing the difference between the market value of the security used as collateral and the value of the loan across a range of factors (length of repo agreement, quality of collateral, credit quality of the counterparty, etc.). This could result in a higherfrequency margining system.

The securities settlement has a medium degree of feasibility to carry out this use case as a proof-of-concept (PoC). This is due to the multi-asset focus, which means multiple non-bank parties would be involved (e.g. CSDs), as well as potential additional regulatory complexity. However, it is worth noting the other participants are regulated financial institutions. Source: RLN

Source: RLN

Another use case in the report relates to wholesale B2B cross-border, multi-currency payments.