A post at www.soberlook.com caught our eye. They look at the impact of SIFI 5% minimum capital ratios on repo. They make some good points but there are some problems too.

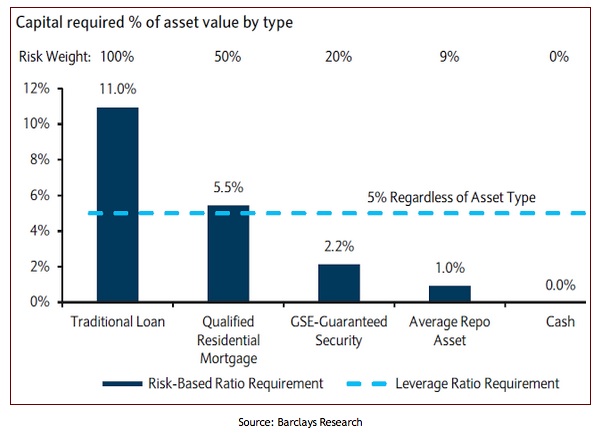

Using research from Barclays, soberlook benchmarks repo as having a 1% “risk based ratio requirement”. That sounds like a GAAP RWA calculation — which makes sense given that the vast majority of repo is on high quality paper.

In a world where U.S. regulators require U.S. SIFI banks to average 5% across the institution, soberlook implies that repo (@ 1%) will be incredibly dilutive and hence unattractive. So will every business that doesn’t make it over the 5% hurdle rate be tossed, especially ones which facilitate so many other businesses and irregardless of its risk profile? Probably not. Repo has been called the grease that lubricates the markets. Take the grease away and bad things happen. But that is not to say that repo businesses won’t be under intense pressure to make higher returns. That will inevitably flow down to higher financing costs.

The post has a “this is what happens when you mess with Mother Nature” series of things which will go wrong. Lets look at the laundry list highlights. You can start each point with “If you make repo uneconomic you will…”

1.) “…Disrupt the functioning of money markets by pushing larger banks out of secured deposits. Deposits collateralized by treasuries (reverse repo) is the only way many institutional players can place cash with banks without taking unsecured bank risk. Now these institutions will be forced take bank risk or buy treasury bills – which will likely go negative as a result…”

2.) “…Reduce liquidity in the treasury markets…”

3.) “…Increase fails and the overall volatility of the treasury markets

4.) “…create similar headwinds as in #2 and #3 above in the MBS markets and potentially other markets that involve some form of securities lending…”

We are not sure about their analysis of capital ratios. First of all, looking at the U.S. G-SIB GAAP capital ratios reported by the FDIC, we see Tier 1 Capital Ratios ratios well above 5% already. Presumably banks already manage their balance sheet and risk. Despite repo balance sheets under continued pressure, the business has still not gone away.

We do wonder about the impact of adopting a simple leverage ratio. But even there, Tier 1 Capital / Total Assets are above 5% for all but one of the U.S. G-SIBs (as of the end of 2012). But there is a catch. Repo businesses manage their statement date balance sheets via Fin 41 netting – but regulators are pushing back on that, looking to use monthly average balance sheet numbers. So unless dealers can do the statement date netting optimization fire drill on a daily basis, they will increase reported balance sheet usage considerably. Irrespective of adopting minimum capital ratios, if repo balance sheets balloon, it will make the business less attractive. So we think that soberlook had the effects right, but maybe not the cause.

A link to the FDIC report is here.

A link to the Soberlook blog post is here.