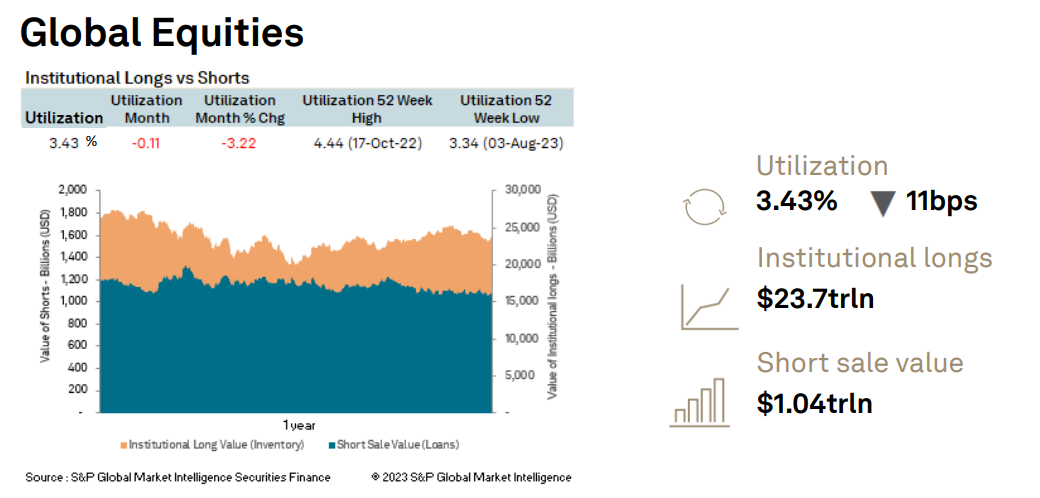

S&P Global Market Intelligence released its long/short report for October 2023. For global equities, utilization was at 3.43% (compared to 3.55% in September’s report); institutional longs at $23.7 trillion (compared to $24.4 trillion); and short sale value was at $1.04 trillion (compared to $1.73 trillion).

Across global equities, the largest increases in short interest was seen across the telecoms (+11bps), consumer services (+6bbps), commercial services (+5bps) and the financial services (+3bps) sectors.

Across global equities, the largest increases in short interest was seen across the telecoms (+11bps), consumer services (+6bbps), commercial services (+5bps) and the financial services (+3bps) sectors.

Across North American equities, short interest increased by 2bps over the month. The largest increase was seen across the consumer services sector.

Short interest across APAC equities decreased to 64bps during the month. Short interest increased across the technology hardware and equipment (+8bps), household and personal products (+6bps) and the materials (+4bps) sectors.

Across EMEA, short interest increased to 19bps. The most shorted sector continued to be real estate and property management.

Short interest decreased by 6bps across the government bond markets and increased by 3bps across corporate bonds.