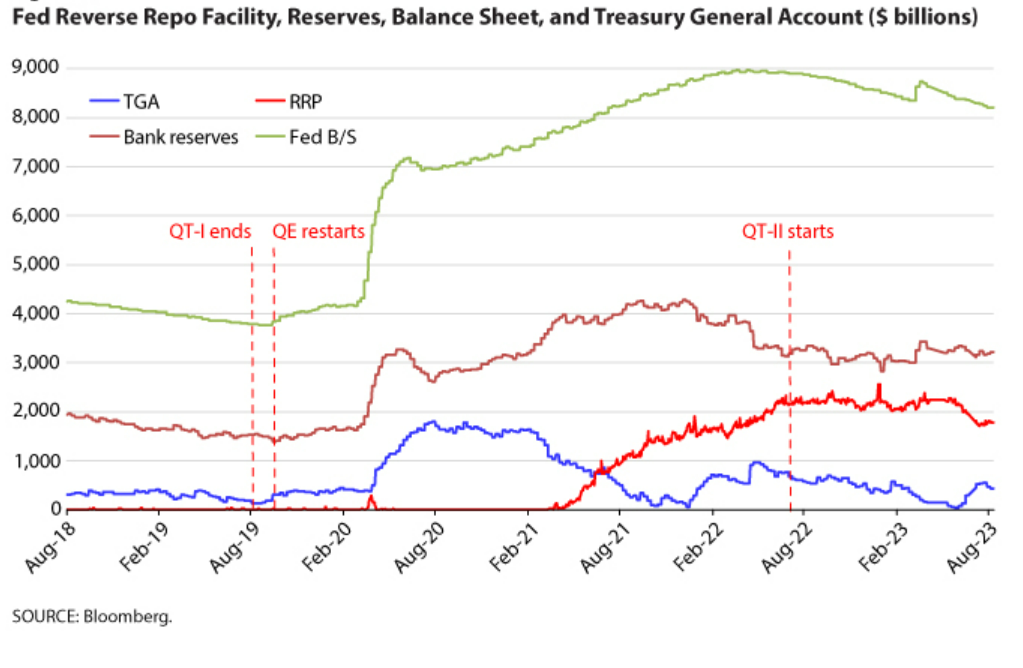

The US Treasury can have a large impact on the Fed’s balance sheet. With the resolution of the debt ceiling impasse in June, the Treasury began issuing debt again and the TGA balance was rebuilt to $432 billion by August 14, 2023. Meanwhile, reserve balances as well as the ON RRP (overnight reverse repo) facility take-up fell by $86 and $455 billion, respectively. As money market mutual funds buy US Treasury bills that are now yielding more than the ON RRP offer rate, non-banks’ funds are migrating from the facility to Treasuries.

The Fed can take actions that affect the level of reserve balances. The banking turmoil in March 2023, when there were sudden runs on bank deposits triggered by the (eventual) failure of three relatively large US commercial banks, resulted in the Federal Reserve establishing the Bank Term Funding Program. This program, together with the Discount Window, triggered a temporary surge in bank reserves and liquidity in general, as the Fed balance sheet temporarily increased. These actions were seen as efforts to bolster financial stability, as we were facing contagion at the time. As the banking turmoil subsided, and the additional use of the liquidity facilities stabilized at lower levels, quantitative tightening (QT) actions dominated the Fed’s balance sheet so that reductions in total assets resumed at its previous pace.

So where do things stand?

On August 14, 2023, the Fed balance sheet was at $8.19 trillion (about 30% of GDP), bank reserve balances were at $3.22 trillion (about 12% of GDP), and ON RRP facility take-up was at $1.79 trillion (about 7% of GDP). As QT-II continues at an accelerated pace, the Fed is likely to reassess the optimal level of reserves in the near future. In the Senior Financial Officer Survey from May 2023, 78% of total respondents reported that their bank prefers to hold additional reserves above their lowest comfortable level of reserves (LCLOR), with 35% preferring to hold additional reserves of at least 50% above their LCLOR. Moreover, roughly three-quarters of respondents reported that their bank does not allow reserves to fluctuate below its LCLOR.

Earlier this year, member of the Board of Governors of the Federal Reserve System Christopher Waller suggested that ON RRP balances could drop to zero without impairing market liquidity. If this is the case, the Fed can continue QT for some time without draining reserves too low. However, there is a risk that ON RRP balances remain sizable and bank reserves represent the majority of the contraction of Fed liabilities as QT continues. In this case, regulatory banking constraints could start binding sooner than expected. Since late March 2023, the ON RRP take-up has declined by $576 billion; however, the planned issuance of Treasury bills alone may not be enough to fully deplete the facility in the second half of 2023.

What financial stability concerns should the Fed consider as it continues its balance sheet normalization plans?

In QT-I, roughly $1.5 trillion in bank reserves appeared to be the limit and lower levels led money market rates to spike. This lower level amounted to about 7% of nominal GDP. At today’s level of GDP, this lower limit would be $1.9 trillion in reserves. Thus, something closer to $2 trillion could be the optimal level of reserves in the system before liquidity constraints begin to force money market rates higher. The optimal level could be even higher, though. Financial markets keep evolving and desired liquidity may be something closer to 10% to 12% of nominal GDP ($2.7 trillion to $3.3 trillion), with the current level of reserve balances already around the upper bound of the estimate. However, in the July 2023 Primary Dealer Survey published by the Federal Reserve Bank of New York, the median respondent believes that reserve balances will fall to $2.625 trillion by mid-2024.