Repo markets have seen several innovations over the last decade, including the introduction of sponsored programs on central counterparties (CCPs) and indemnified repo provided by repo dealers. As the market evolves, the broad universe of buy-side client cash and collateral providers should upgrade or continue to revisit their understanding of how different execution and settlement venues affect their businesses across risk, operations and investment management.

by

Travis Keltner, Head of Repo Trading and Financing Solutions, State Street

Ingvar Sigurjonsson, Head of Analytics and Optimization for Financing and Collateral Solutions, State Street

Josh Galper, Managing Principal, Finadium

- Buy-side preferences in repo service and counterparty exposure models result in recognizable costs for repo dealers.

- These costs are passed back to clients in the form of repo spreads or fees for related transactions.

- This paper quantifies repo dealer costs across four types of transacting routes: bilateral on balance sheet, central counterparties sponsored repo, indemnified peer-to-peer and non-indemnified peer-to-peer.

- Buy-side clients have the option to ask their repo dealers for one or more models that suit their risk, pricing and counterparty exposure preferences.

- Dealer revenues (spreads) in traditional repo are outweighed by balance sheet costs – by as much as 70-75 basis points for leverage constrained firms.

This paper aims to demonstrate the impact of repo market pricing across service types from the perspective of the charges that dealers accrue on their balance sheets. “Service” is defined as the means by which a repo trade is initiated and closed out and whether the end counterparty is a dealer, a CCP or another client type (pension, hedge fund, etc.). The four models evaluated are: (1) bilateral trading with a dealer; (2) sponsored clearing through a CCP; (3) peer-to-peer (P2P) indemnification with direct counterparty risk exposure; and (4) non-indemnified P2P. The results show that buy-side clients may want to consider their options in repo by weighing trade-offs between pricing and counterparty exposure.

The need for innovation

Bank capital requirements are the main drivers of new repo service models in the post financial crisis era. It is widely known that these capital requirements limit availability of bank balance sheets, including in the context of bilateral uncleared repo. For example, the Leverage Ratio (LR) looks to assess the asset and liability exposure of a bank without risk asset weighting; implying that a low revenue United States (US) treasury repo counts as much towards a bank’s LR as a high revenue equity repo. Banks look to maximize their revenue opportunities within the limits of these capital rules, and have developed increasingly sophisticated methods of allocating capital accordingly.

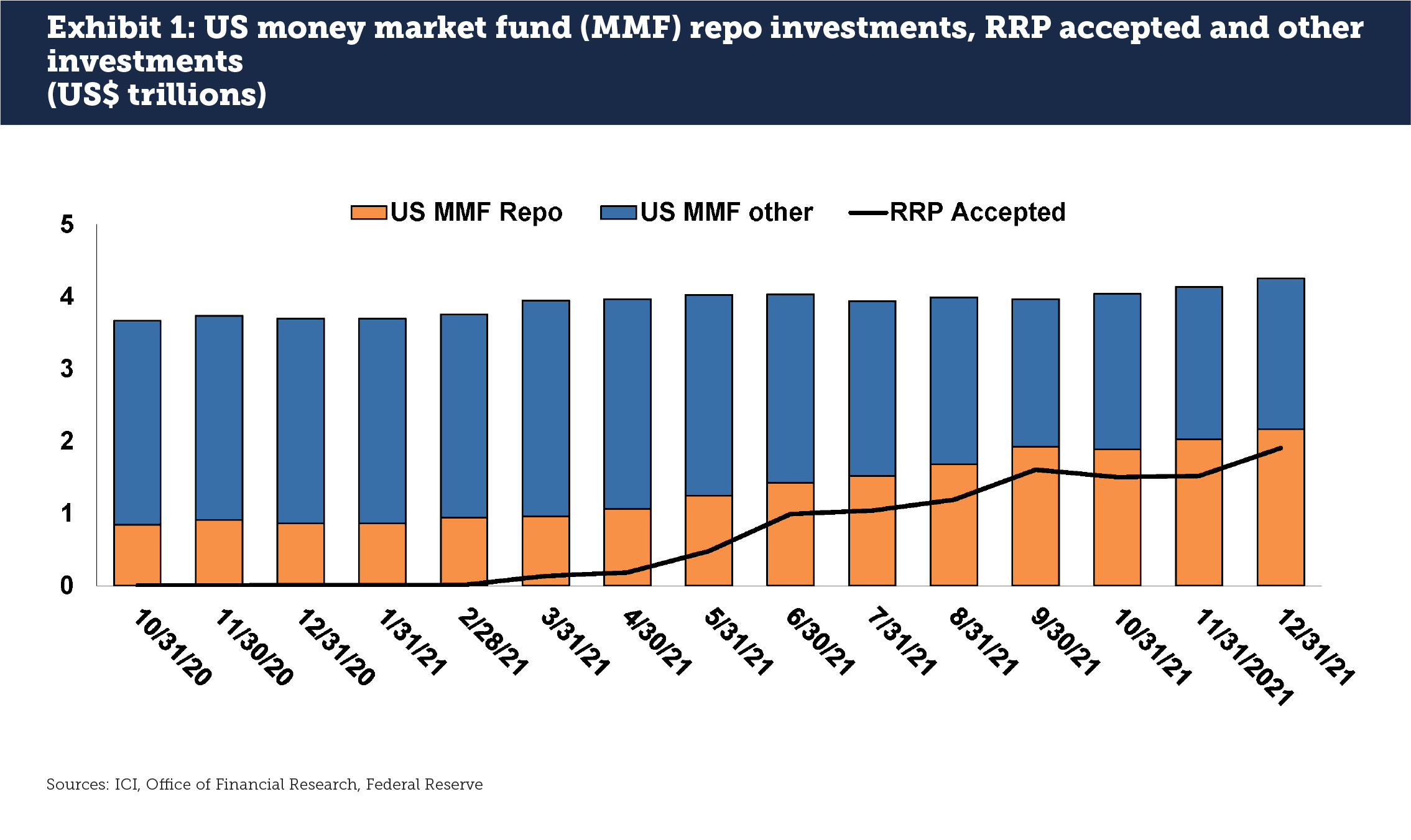

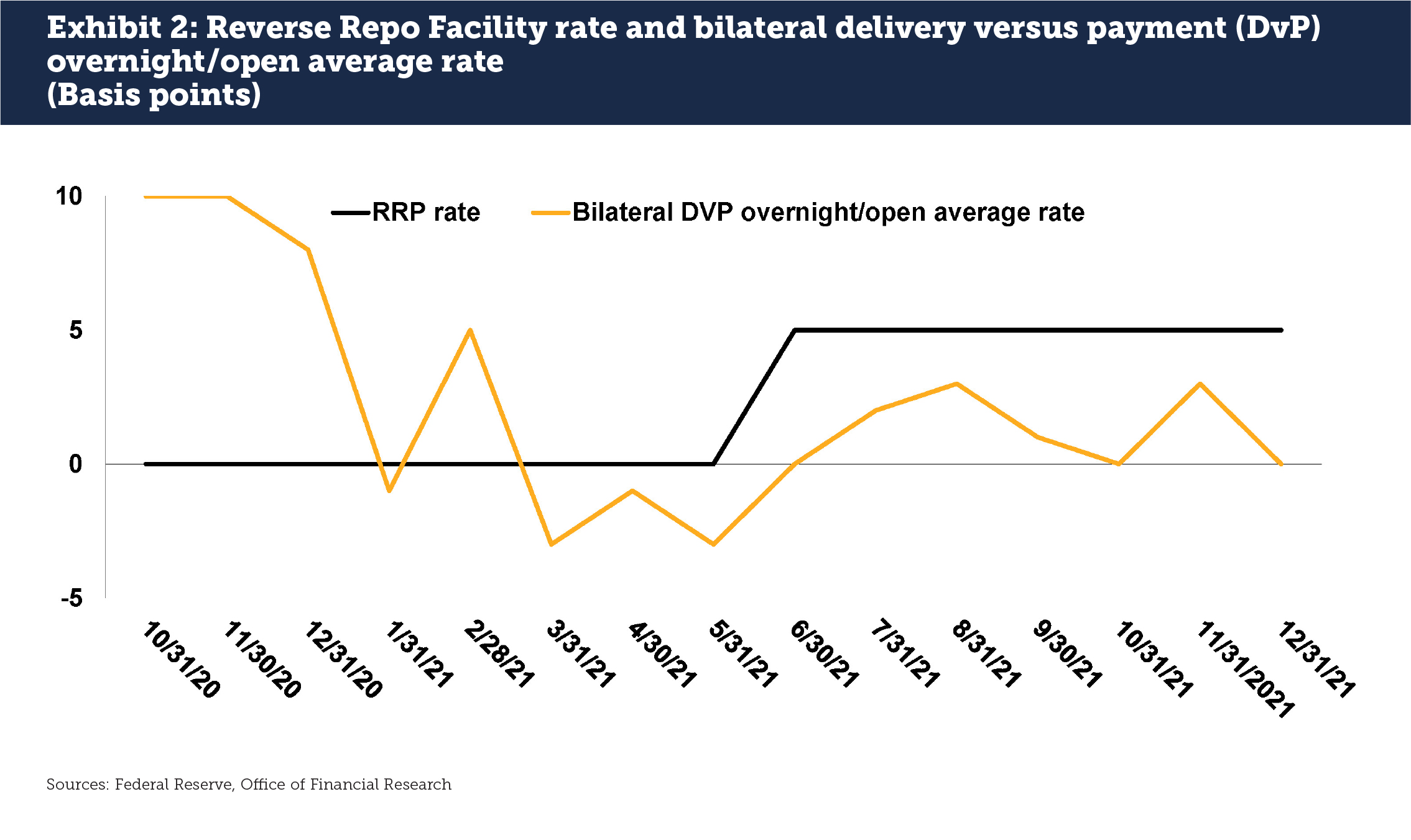

By appropriately following regulatory mandates, cash-rich banks have reduced their need to collateralize low value securities to raise short-term funding. Additionally, investor demand for repo has grown in line with US Treasury supply with a smaller amount of cash needed in the private market. This, in tandem with the Federal Reserve’s actions to add liquidity to the funding markets in 2020-21, has resulted in a surge in assets held by the Fed’s Reverse Repo (RRP) Facility. RRP volumes gradually grew from nearly nothing in October 2020 to US$1.9 trillion in December 2021 (see Exhibit 1). Meanwhile, private sector repo rates were generally above the Reverse Repo (RRP) rate until March 2021, when US regulators ended a temporary exemption allowing banks to not count US Treasuries on the LR (see Exhibit 2). It is no surprise that interest in the RRP grew materially once the Fed’s offered rates exceed those in the private market. Unfortunately, the growth of the RRP due to the regulatory constraints on bank LRs is not a desired outcome for capital market funding practices.

Four repo trading models

Alongside traditional bilateral repo trading, three other models offer valuable options to buy-side clients: sponsored repo on CCPs, indemnified repo for P2P and P2P repo without indemnification. These have useful benefits for both cash and collateral providers and can supplement each other for the specific needs of the repo community.

Bilateral (dealer)

Bilateral repo settlement with a repo dealer is the traditional means to enter into a repo transaction. Trades can be settled directly by internal teams, using a triparty agent or on the Fixed Income Clearing Corporation’s (FICC) DvP platform, subject to membership. The result remains bilateral exposure for the dealer; the choice of operational platforms for settlement does not change the firm’s balance sheet assessments for counterparty or asset type. As a result, bilateral repo is costly from a dealer’s perspective. Clients trust the dealer’s capital and strong operating procedures to successfully unwind the transaction at expiration.

CCP sponsored repo

CCPs have introduced new models over the last decade that allow repo dealers to sponsor buy-side clients to clear transactions. There are multiple versions of sponsored clearing; a February 2021 Finadium report found six types of CCP models for clients.

CCPs do not have balance sheet costs themselves, but rather rely on the mutualization of risk across members. CCPs collect default fund contributions and/or margin to create a “risk waterfall” of capital to ensure repayment in the event that a member defaults on the obligation. CCPs are obligated by national regulations and the Basel Committee on Banking Supervision (BCBS)/ International Organization of Securities Commissions (IOSCO) Principles of Financial Market Infrastructures (PFMI) to hold or have ready access to enough capital to cover the loss of their top one or two clearing members at any one time.

In sponsored repo, an on-leg of the trade occurs between the dealer and the client, akin to the bilateral model. The dealer then sends both sides of the trade to the CCP, which breaks the trade and creates two new ones, one for each side with the CCP as the counterparty for both. This process is called novation and ensures that the CCP is the legal counterparty in the event of a member or client default. Sponsoring dealers must provide capital related to their sponsored activity and guarantee to the CCP.

Although costs remain, the benefit of engaging with a CCP is twofold: first, CCPs offer reduced capital costs through a lower Risk-Weighted Assets (RWA) figure than dealers can get with most bilateral counterparties. The BCBS has designated CCPs to have a RWA of 2%, compared to the 100% that may be required for many clients. Second, CCPs offer the opportunity for dealers to net their exposure down following accepted netting rules. Instead of multiple individual transactions with different clients that prohibit netting, the dealer now has one counterparty (the CCP) and can reduce its balance sheet exposures to the extent that transactions share the same maturity date.

In order to offer sponsored repo to clients, dealers must adhere to the CCP’s governing rulebook and operating model. CCPs dictate permissible transaction terms, collateral types, and sponsored client types (e.g., entity type and or jurisdiction of domicile) that are eligible for their programs. As a result, only a certain subset of a dealer’s client-facing repo book may be eligible to be migrated to the sponsored model.

Indemnified P2P Repo

The P2P model of repo offers clients direct exposure to one another without a repo dealer as an intermediary. In the indemnified model, the dealer provides insurance in the form of counterparty default indemnification guaranteeing that clients receive their original cash or collateral in case of counterparty default. A dealer or non-dealer institution provides credit backing in the transaction but the legal exposure is between the two client counterparties.

Typically, neither of the counterparties in an indemnified P2P repo transaction will be dealers themselves. Notwithstanding a fee that may be charged by the dealer in connection with the indemnity, trade economics may be relatively better than bilateral or sponsored repo in the P2P model as neither client has a balance sheet cost to consider when entering the trade. Business, risk and legal teams at each counterparty can turn this to their advantage with a combination of credit analysis and dealer indemnification. Third-party credit rating reviews can help develop institutional comfort with this model.

The business of indemnification has a long and successful history for banks in agency securities lending programs and has become a must-have for many institutions. When offering indemnification, securities lending agents must be confident that their loans to counterparties will be returned. If not, they are responsible for making up the difference for clients in the form of cash or securities. In practice, agent lenders have rarely needed to use their indemnifications: securities lending, like repo, uses the overcollateralization of loaned assets as a first line of protection and the credit risk evaluation of counterparties as a backup. Indemnified repo is based on the same principle of overcollateralization.

Non-indemnified P2P

Counterparties may also elect to transact in repo directly without indemnification. The counterparty and risk exposure to the borrower or lender change. However, in the event of default, there is no insurance to protect the initial cash or securities. This is the model that most firms think of when considering P2P.

On the positive side, counterparties can avoid the cost of bank or non-bank insurance. They can still protect themselves by conducting robust credit reviews and asking for extra collateral in case of default. On the negative side, cash lenders must conduct their own credit analysis for which data may be lacking and traditionally, dealers have taken on the counterparty credit exposure. Lenders have also shown themselves to be more conservative in their selection of counterparties, which reduces their utilization options and revenue generation opportunities.

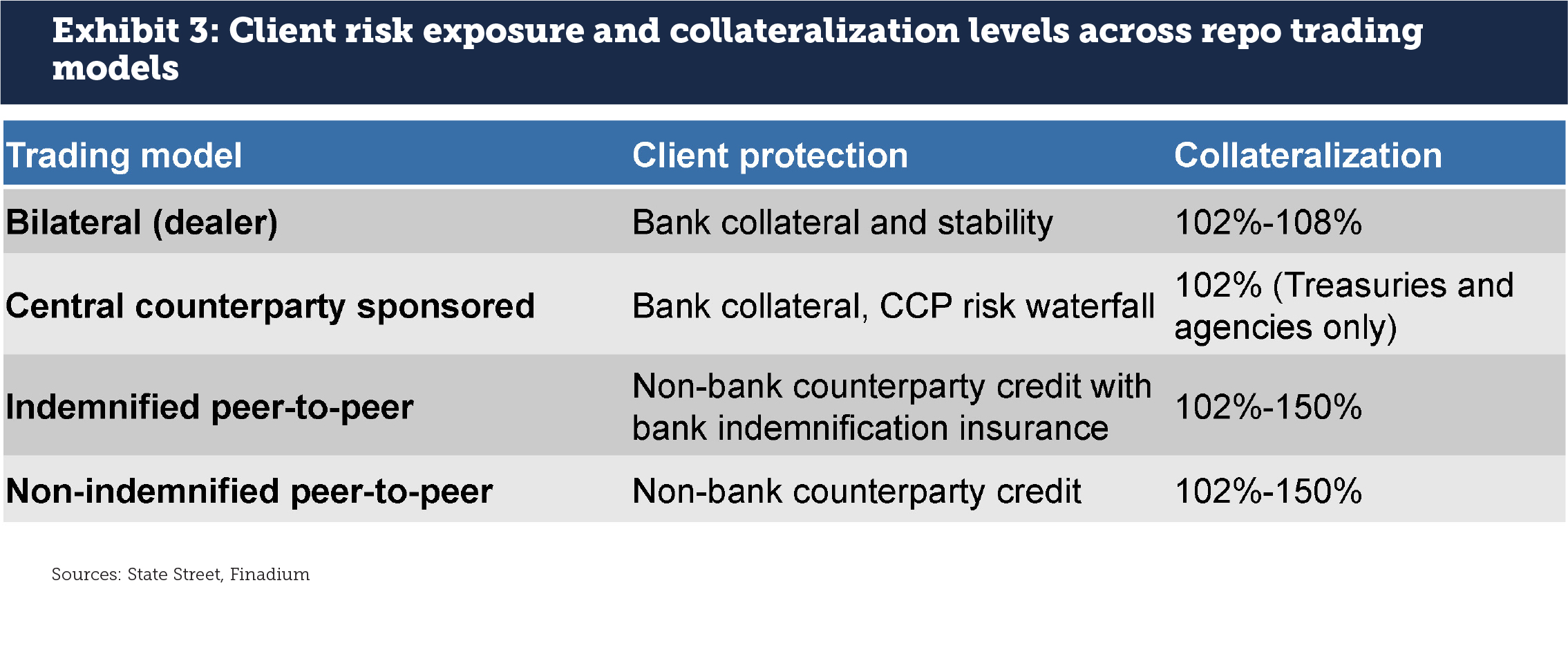

Each model above offers benefits and costs in risk exposure and collateralization levels (see Exhibit 3). For some clients, the stability of a dealer is preferred when transacting in repo due to simplicity and confidence, especially when outsourcing operations to a triparty agent. Cash and collateral utilization opportunities expand on CCPs, where dealers have more balance sheet capacity to engage in the same trade. Collateralization levels are typically the same whether the trade is with a dealer on a bilateral basis or a dealer using a CCP. Non-indemnified P2P is the least expensive option but may not suit every firm’s risk tolerance.

Repo pricing is based on counterparty costs

A selection of repo service models leads to different outcomes in pricing for both dealers and clients. The balance sheet, CCP and indemnification costs of repo can be quantified with results that show why dealers and non-dealer counterparties may prefer one model over the other from a revenue perspective.

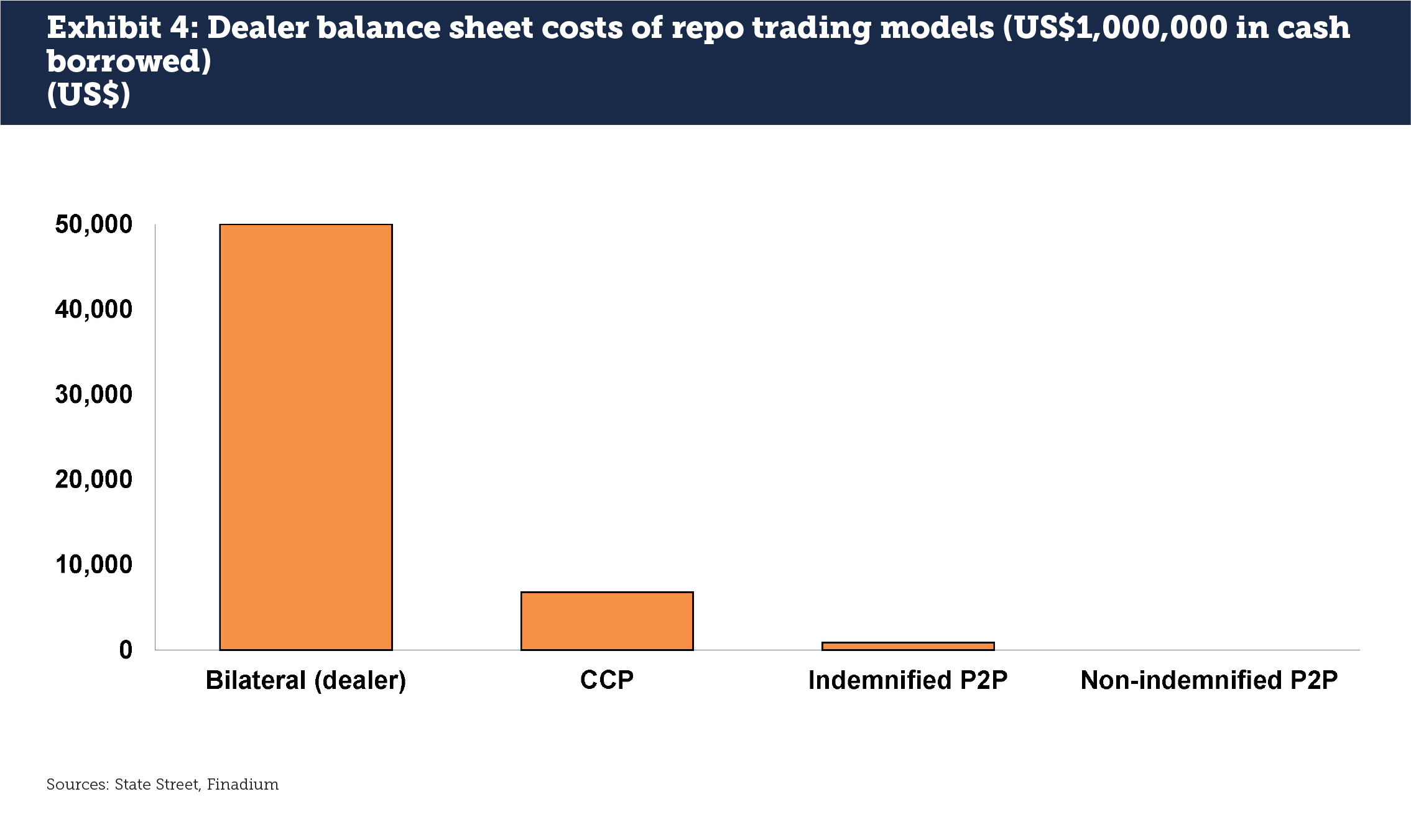

Our model results show that balance sheet usage is highest in bilateral client transactions and descends through CCP sponsored, indemnified P2P and lastly non-indemnified P2P (see Exhibit 4).

The two factors that influence repo dealer balance sheets the most are impacts to LR, whether the Basel III version or the US Supplementary Leverage Ratio, and risk-based capital requirements. As dealer capital can oftentimes be utilized to cover multiple balance sheet obligations, dealers will look to the greater capital requirement as the constraining factor. As long as a dealer faces counterparty exposure at some level of the transaction, there will be an associated LR or risk-based capital cost. Additionally, each institution has its own resource allocation constraints based on regulatory regime and balance sheet structure.

A simple model of US$1,000,000 in repo cash borrowed and US$1,020,000 collateral lent (102 percent margin) shows that costs are highest for on balance sheet, bilateral settlement. At a 5% Tier 1 LR, the dealer will need to retain US$50,000 in capital to support the transactions. This is greater than the risk-based capital required of US$5,770 when using a regulatory haircut approach to calculating exposure-at-default (EAD), making the LR the binding constraint.

The use of a CCP drops the LR capital to zero (to the extent sponsored trades are netted off-balance sheet), at which point risk-based capital requirements become the binding constraint. The inputs to calculating risk capital include: the dealer’s EAD to the initial client counterparties, the default fund contribution to the CCP and margin required. Our model shows that the total capital requirement for using a CCP for 100% of transactional activity falls to US$6,790.

Costs fall further if the dealer provides counterparty default indemnification to the cash investor against a borrower default in a P2P trade. Indemnification is a guarantee, which makes it an off balance sheet credit exposure. There is no default fund contribution or leverage exposure and the capital cost is derived solely from the counterparty credit risk arising from the guarantee. The total capital required for P2P with dealer indemnification is US$885 in our model.

The least punitive model from a repo dealer’s perspective is supporting P2P trades without indemnification, bilateral capital exposure or CCP sponsorship: the balance sheet cost would be US$0. However, only a small percentage of clients is interested in this option due to concerns, or mandates, about credit exposure and the newness of the business. It is therefore unrealistic to think that a repo dealer could convert their entire book to non-indemnified P2P.

The choice of repo service model has a corresponding impact on the pricing that clients receive. The more that a dealer’s balance sheet is employed, the more costs dealers will have to pass back to their clients to support the trade. Fully baked-in dealer costs may never cover the cost of a US treasury repo transaction, implying that the dealer expects client business with higher-spread activities in order to justify the cost of the repo trade. Repo then becomes an essential part of the entire relationship but must be financially supported elsewhere.

Dealer revenues improve when looking at non-government asset classes but this is still not enough to cover all bilateral costs. Spreads in US treasury repo in 2021 were often under 1 basis point, reflecting the very low interest rate environment. Spreads in equity repo that trade 35-50 basis points higher than US treasuries may allow for 5-10 basis points earnings, but dealer balance sheet costs may be closer to 80 basis points at a leverage-constrained bank.

Margin impacts the amount of collateral that dealers must post to their counterparties; different repo asset classes require dealers to post different amounts of margin to cover their counterparty’s potential exposure in the event of default. Data from the Federal Reserve shows the median haircut in triparty for US treasuries is at 2%, while equity repo requires 7% to 8% margin. Swings in collateral margin levels related to a specific asset class can also translate to improved or punitive pricing given that the balance sheet cost to dealers can be mitigated or increased.

For dealers with 100% of their trading on balance sheet, a combination of increased margin and a higher volatility factor in risk calculations for equity repo results in higher risk-based capital requirements but no change in the LR exposure: the LR is still the gating factor. CCP costs more than triple from US$6,790 to US$27,230, a significant increase but still much lower than the US$50,000 LR cost; the CCP remains the better option (see Exhibit 5). Indemnified repo capital costs increase from US$885 to US$3,455 while the increased margin does not impact dealer costs for non-indemnified P2P trades as the dealer does not post margin.

Client preferences determine repo revenue outcomes

Clients should be aware that dealers have tangible costs that must be recaptured either at some point in a trade or in the broader dealer/ client relationship. A client may say they prefer exposure to a dealer’s balance sheet, however this implies that pricing will be structured to help the dealer recoup its cost base. On the other extreme, P2P non-indemnified repo trades provide greater price flexibility between cash and collateral providers, albeit with no dealer guarantees or protection.

CCP sponsored repo and indemnified P2P repo offer a middle ground for clients of avoiding the punitive costs of dealer balance sheet requirements while receiving external protection against the counterparty exposure risk of another client entity. These choices offer the greatest compromises between price improvement due to lower dealer cost and the greatest counterparty exposure protection. These preferences translate back into the pricing that clients receive in repo transactions and ultimately to the bottom line revenues.

About the Authors

Travis Keltner is head of Repo Trading and Financing Solutions at State Street Global Markets. Travis provides oversight of all principal secured funding trading activities, with a primary focus on client activities related to sponsored member and P2P repo programs. Travis also oversees the client collateral trading, analytics and optimization platform as well as the strategy and implementation of global financing solutions. He can be reached at tkeltner@statestreet.com.

Ingvar Sigurjonsson is head of Analytics and Optimization for Financing and Collateral Solutions at State Street Global Markets. Ingvar provides oversight of measurement and management of financial resource utilization across collateral and financing products, and leads optimization products for clients. He can be reached at isigurjonsson@statestreet.com.

Josh Galper is managing principal of Finadium and heads its research and consulting advisory practice in securities finance, collateral and derivatives. He can be reached at jgalper@finadium.com.

About State Street

State Street Corporation (NYSE: STT) is one of the world’s leading providers of financial services to institutional investors including investment servicing, investment management and investment research and trading. With US$43.7 trillion in assets under custody and/or administration and US$4.1 trillion* in assets under management as of December 31, 2021, State Street operates globally in more than 100 geographic markets and employs approximately 39,000 worldwide. For more information, visit State Street’s website at www.statestreet.com.

*Assets under management as of December 31, 2021 includes approximately US$61 billion of assets with respect to SPDR® products for which State Street Global Advisors Funds Distributors, LLC (SSGA FD) acts solely as the marketing agent. SSGA FD and State Street Global Advisors are affiliated.

About Finadium

Finadium is a research and consulting firm focused on securities finance, collateral and derivatives. In its research practice, the firm assists plan sponsors, asset managers, brokers, custodians, hedge funds and technology firms with understanding the market and in maximizing the effectiveness of their resources. Finadium research is available on a subscription basis. Finadium also conducts consulting assignments on vendor selection, marketing and product development. For more information, please visit their website at www.finadium.com and on Twitter @Finadium. Finadium publishes the daily news and opinion site Securities Finance Monitor.