The transparency afforded by ETFs provides for unique analysis on the time-varying preferences of passive investors. Hamish Seegopaul, global head of Index Product Innovation at STOXX, takes on the objective of deciphering those preferences by analyzing ETF flows but also looking through to the underlying holdings.

The exercise presents a view of investors’ granular preferences, ex-post, and can be a valuable source of information that comes closer to investors’ revealed preferences, as opposed to broad ETF categories, which may be closer to their stated preferences.

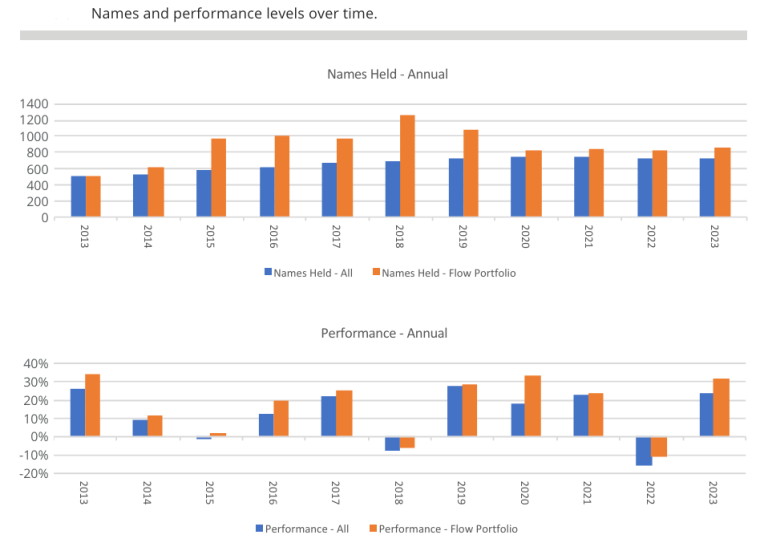

The study looks at US ETFs and employs a taxonomy of preferences across style, industry and regional factors. The author creates a ‘Flow Portfolio,’ which is comprised of securities that were theoretically bought or sold each year to facilitate ETF’s net flows.

Key findings in the study of Flow Portfolios are:

- There has been a high degree of year-on-year variability in style, industry and regional exposures

- There is evidence of ongoing appetite for broad-based exposure

- Over longer time horizons, there is little clear preference for specific exposures

- No matter the time frame examined, investors favored ETFs with strong in-year performances

- Performance rules all preferences

Some trends are persistent over time, Seegopaul writes. For example, across years the Flow Portfolios show a preference for ‘more’ – more holdings and more performance – compared to the entire ETF universe. The preference for higher returns is probably of little surprise, and the paper does not imply that investors were able to capture it.

This finding relates to a common investor issue of the “returns gap”, dating back to the heyday of mutual funds. Returns reported on, for example, fact sheets reflect a “buy and hold” strategy over a full time period, (e.g. 1 year, 5 years, since inception, etc.), whereas in reality, investors make contributions and withdrawals to funds over time.

Using dollar-weighted averaging (reflecting contributions/withdrawals), as opposed to standard time-weighted averaging (reflecting buy/hold), researchers have found that the returns achieved by investors tend to lag the returns of the funds they are invested in, on average. This is attributable to the challenge of market timing, and the risk of selling dips and buying tops. A preference to allocate to ETFs with strong in-year performance can exacerbate this challenge.

That preference also coincides with a relatively constant preference for Momentum. The factor remains somewhat of an outlier, as all other styles show a degree of variability year after year (although that variability mostly disappears when measured over time). Sectors and regions exposures preferences, too, change over time but are fairly neutral over the long run.

“In the short run, preferences can be highly variable,” Hamish writes. “In the long run, there is one preference to rule them all – and that is performance.”

One other notable shift in aggregate exposure over time is the move away from Americas-based holdings and towards EMEA and Asia/Pacific ones, the report says, a sign of diversification preference.

“These findings support a rich product landscape, however, pose challenges for the industry,” the author adds. “Some challenges – such as the ‘returns gap’ – have been sticky. Others, such as understanding preferences prior to investment decisions, will lead to further innovation.”