We have been working out what the new model of securities finance looks like within a bank enterprise. We documented and diagramed a number of these concepts in our June 2015 research report, “A New Look at Securities Lending Operations and Technology.” At this point we have some additional thoughts to share with our clients.

There is no doubt that securities finance has changed. Almost all large banks have moved to a model where securities lending is no longer an independent silo but instead relies on a raft of shared services offered from a core bank infrastructure. Transparency is making fast inroads both from voluntary client reporting and UCITS disclosures, and soon Trade Repositories and mandatory US asset manager publications of all securities on loan. These two forces – securities finance becoming a spoke to a bank’s hub of services, and transparency (along with massive government regulation, of course) – embody creative destruction of an industry that has thrived from independence of its business model and opacity of prices.

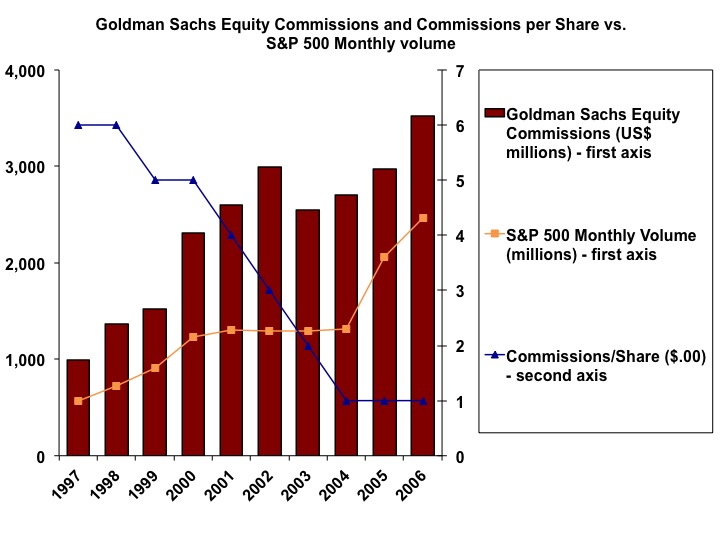

We’ve seen a version of this story before in equities. Sharp drops in equity trading commissions worldwide were met with grave concerns that businesses would shrink and disappear with terrible consequences for the market. In fact, some of that did happen, but those businesses were replaced by new entities and technologies that enabled a huge growth in equity commission revenues. Many years ago we created the chart below that shows Goldman Sachs’ equity commissions per share dropping from 6 cents to 1 cent while revenues rose from US$989 million in 1997 to US$3.5 billion in 2006. Meanwhile, S&P 500 market volume rose 336%. We’re not suggesting that anything this radical would happen now in securities finance, but the idea that transparency and lower per share fees = market disaster is not supported. In fact, the ability to focus on building new business models with a revised tool set could be a great benefit.

Sources: Goldman Sachs, Yahoo Finance, Finadium analysis

In a market where pricing is known and fees are standardized, commodity services work well for the largest players that can invest heavily in technology. This is the “gorilla of order flow” model where the firm with the most clients, and able to push the most transactions down its technology pipes, wins. This is in part what led the big banks to get even bigger in the years before 2008 and through today.

Being big is not the only winning model though. We only need to look at the many, many creative brokerage firms that grew only after equity commissions started to fall to see the success stories. Merlin Securities (sold to Wells Fargo) and Fox River (sold to SunGard) are two examples. Liquidnet launched in 2001 when equity commissions had already fallen to 4 cents a share, and now operates in 43 markets worldwide. A fair equivalent in securities finance is CloudMargin’s disruptive and low cost approach towards collateral management.

Sometimes change sucks, especially when the old model was been a winner for so long. We just don’t see it working going forward through. Some firms (BNY Mellon and JP Morgan, for example) have, in our opinion, done the hard work of figuring out what the new path looks like and made the right investments. Turning a big ship is hard but a few firms are on their way.

On the other hand, building and turning a small ship is easy. The next step is figuring out what the new ship should look like.