The Financial Stability Board (FSB) issued a press release outlining what they discussed at their Sept. 25th meeting in London. Leverage and liquidity is still on their mind. Securities lending is also a hot topic, and while the FSB has been writing about this for years, it seems like they are starting to focus more attention on wrapping up some longstanding business.

The FSB is taking a close look at asset managers and embedded leverage. From the press release:

[The FSB] “…reviewed the initial findings from the longer-term work on asset management structural vulnerabilities and identified areas for further analysis, including:

- Mismatch between liquidity of fund investments and redemption terms and conditions for fund units;

- Leverage within investment funds;

- Operational risk and challenges in transferring investment mandates in a stressed condition;

- Securities lending activities of asset managers and funds; and

- Potential vulnerabilities of pension funds and sovereign wealth funds…”

Coincidentally, the SEC just came out with proposed rules for characterizing the liquidity of mutual funds and ETFs. We wrote about it on Sept. 24th in a post “The SEC wants to make sure mutual funds and ETFs are liquid for investors. This isn’t going to be as simple as it sounds.” The SEC wants funds to figure out what bonds are liquid over various timeframes.

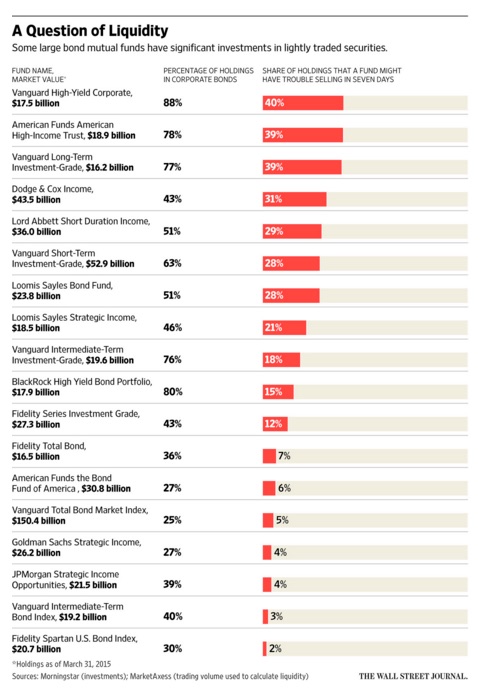

The Wall Street Journal had an article on bond funds last week by Matt Wirz and Tom McGinty, “The New Bond Market: Some Funds Are Not as Liquid as They Appear, Investment firms test SEC guidelines on securities that are seldom traded” (sorry, behind the pay wall). They wrote,

“…By the Journal’s measure, 10 of the 18 largest funds that invest meaningfully in corporate debt have significant holdings of seldom traded bonds. All the funds in the analysis said they are compliant with SEC liquidity guidelines…The crux of the problem is that mutual funds own more bonds that seldom trade than ever before, but they still promise to pay out investors within seven days of redemption of their shares…”

And they had an interesting graphic:

It is no surprise that investment managers are pushing back. If fund managers were required to hold bank-style capital and manage liquidity to LCR, etc., it would put a serious dent into the industry. From a Sept 28th Reuters article by Leigh Thomas “Central bankers warn against extending bank regulations to shadow banks”:

“…Philipp Hildebrand, a former Swiss central banker now a vice chairman at U.S. asset manager Blackrock, stressed that asset managers were vastly different to banks, with small balance sheets and little leverage…”Capital … would hardly be the appropriate answer for asset mangers given that there is not really much of a balance sheet there,” he said…”

The FSB specifically called out securities lending by funds. It begs the question: does securities lending add leverage to funds? The simple answer is: yes, sort of. Funds lend out securities and receive cash, mimicking borrowing money and reinvesting in other assets. If they reinvest the cash in ultra-safe assets, it is hard to characterize that as leverage, hedge fund style. But memories of abusive cash reinvestment don’t die easily. While the argument about leverage may be a tempest in a teapot, some collateral transformation practices of fund managers are not a transparent as they could be.

And the FSB hasn’t forgotten about mandated haircuts on securities financing trades. From the press release:

“…The Plenary agreed the approach for applying the FSB framework of numerical haircut floors to non-bank-to-non-bank securities financing transactions. The final framework will be published shortly with an implementation date by the end of 2018…”

While the FSB isn’t always the fastest moving actor in the market, they are persistent.