The 2015 ISDA Margin Survey was just released. It is always a treasure trove of information and this year is no exception. We take a look.

The report is largely divided into cleared and non-cleared derivative collateral practices. The data used in the 2015 Margin Survey is sampled as of December 31, 2014.

Collateral for cleared derivatives jumped, reflecting the continued shift toward cleared trading from non-cleared. From the report:

“…Total reported collateral for cleared derivatives transactions (received and delivered for house andclient cleared trades) rose 54%, from $295 billion to $455 billion between 2013 and 20144. Total collateral (received and delivered) related to client clearing more than quadrupled, increasing by 262.5%. All collateral types contributed to the rise, with the use of cash, government securities and ‘other’ securities increasing by more than 250% per category…”

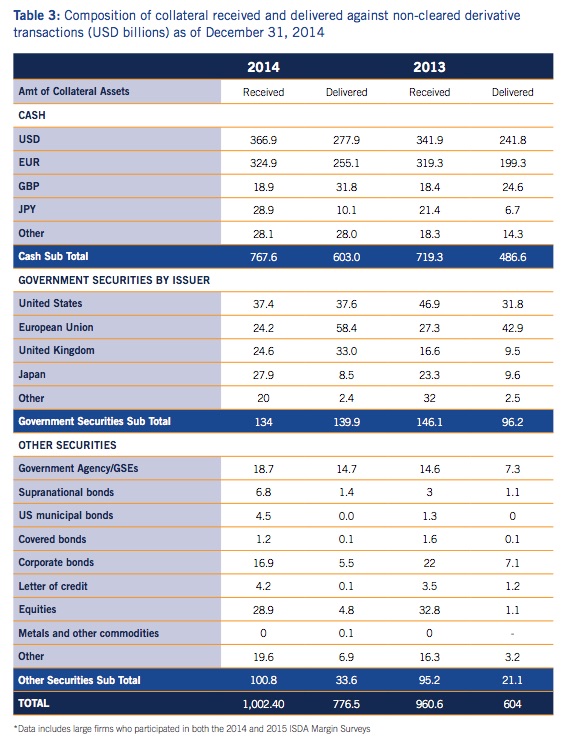

Cash is still king when it comes to margin:

“…The use of delivered cash for non-cleared derivatives rose by 23.9%, and represented 77.7% of collateral usage by asset type…”

and

“…The collateral-received [for non-cleared derivatives] figure was driven by a 6.7% increase in cash, which represented 76.6% of collateral used…”

Similar story on cleared derivatives. From the report:

“…[for Cleared Derivatives] Cash was the most commonly used collateral type as a percentage of the total, but declined from 66.6% to 59.3% as received collateral to meet initial margin. Conversely, cash delivered to meet initial margin rose from 51.7% to 60.1% over the year. Government securities received to meet initial margin increased from 30.8% to 38.6%, but the amounts delivered to meet initial margin fell from 48.2% to 38.3%. Other securities received and delivered were largely unchanged…”

So if cash is the most common form of collateral, does that mean firms are not optimizing? Well, no….

“…The efficient and effective use of collateral, known as collateral optimization, has become more important to market participants. As collateralization becomes more commoditized through process improvement and automation, there is an increasing trend to introduce business rules that maximize the efficiency and minimize the cost of collateral. The practice of collateral optimization is particularly important in the event high-quality collateral becomes scarce. Over 83% of large firms optimize collateral and 70.0% of these do it systematically…Medium-sized firms are not far behind, as 65.0% optimize collateral. Of this group, 53.8% do it systematically. Most of this systematic optimization occurs when needed (61.5%). Small firms optimize collateral roughly one third of the time. When they do this, they employ systematic optimization 100% of the time, half of which is done daily and half of which is done when needed…”

So, if 83% of the large firms optimize collateral, and cash is the most common form of collateral, we have to ask ourselves the same question we asked about last year’s report: could it be that cash is, for many, an optimal asset to use? What about all those state-of-the-art collateral management systems that manage cheapest to deliver securities? Is anyone using them?

The survey asks where the collateral is being managed: front office, back office, credit? For big and medium sized firms, it is generally a front office responsibility. Yet for ¼ of the respondents, the back-office is still handling the work. The survey explained this:

“…One reason for the front-office focus could be that the optimization strategy is based on liquidity risk, funding costs, capital costs and other economic factors that are a part of everyday life on the trading desk. Meanwhile, rules-based methods for optimization may fall within the sphere of the operations group…”

The ISDA collateral survey illustrates the continued expansion of cleared derivatives as well as the stickiness of cash as collateral. There are other interesting results that we did not look at and we suggest anyone interested to take a read.