It is now part of financial textbook wisdom that collateralization is a favored tool to reduce unsecured exposures in financial systems and thereby promote systemic stability. However, in stark contrast, the main work horses that ensure that collateral is being enabled and allocated in the most efficient way, Securities Finance Transactions (SFTs), are still being distrustfully scrutinized by regulators who have yet to make up their minds on whether these instruments are good or bad for systemic stability of financial systems.

Ever after the outbreak of the financial crisis, SFTs have been in the limelight of regulatory action because of their potential role in the run up to the financial crisis. According to that conventional wisdom, SFTs facilitated the build-up of excessive leverage and allowed financial institutions to generate irreconcilable funding mismatches. It is true that in the regular course of business, financial institutions to some extent build up wrong-way risk positions: transactions where counterparty and collateral are strongly correlated but where the economic, regulatory capital and funding requirements would work on the basis that they are uncorrelated. In the same way, SFTs were instrumental in the funding of shadow banking entities like hedge funds but also in the funding of other non- or under-regulated financial institutions like repo conduits, special purpose vehicles and small banks, among others.

Repos were blamed for the demise of Lehman Brothers, with responsibility being placed at the feet of many hedge funds and repo-based funding businesses like Sigma, Gordian Knot and K2. Along this vein, it is also argued that repos played a role in non-domestic funding for Icelandic banks prior to the country’s default. Moreover, after contributing to the build-up of overall systemic fragility, SFT transactions worked as a fire accelerant when – in line with other market segments – SFT markets seized and eventually deleveraged sharply. This is the “run on repo” story: an interpretation that has led regulators across the globe to propose and implement all manner of regulations for an already highly regulated market. It’s a situation that may, at some point, trigger the kind of demise of the collateral market that we have already seen with unsecured money markets.

The layering of regulatory costs on European SFT markets

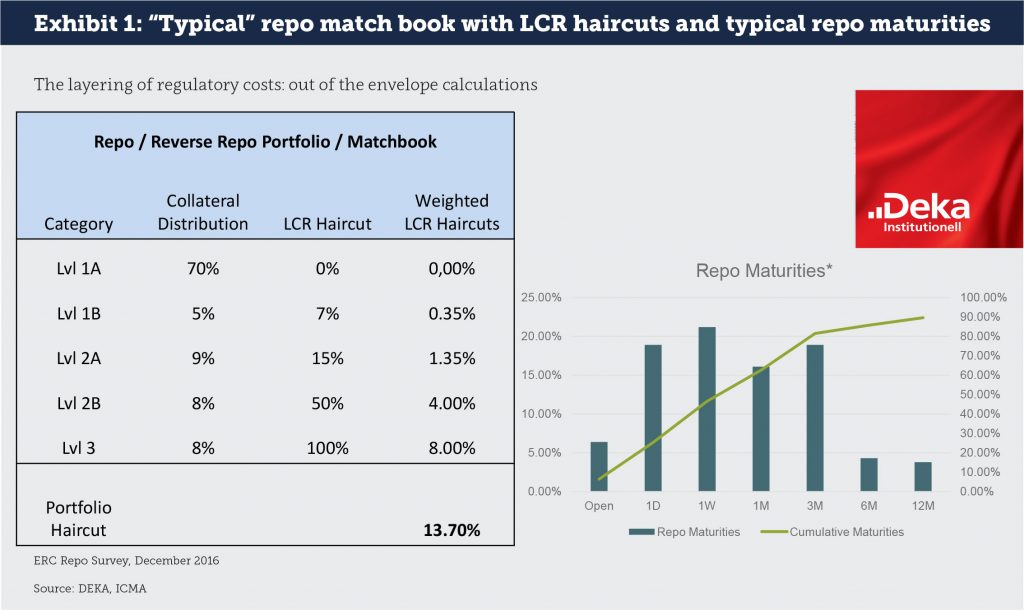

Part of the heated attention regarding regulation of SFT markets is that they are short-term (see Exhibit 1). Regulators hate “short-termism” in financial markets and have come up with numerous regulatory initiatives to reduce short-term exposures on the balance sheet of banks. However, in doing so, they ignored the fact that most SFT markets usually operate in highly liquid markets. In those markets, the liquidity of the underlying collateral offsets the risks of the short-term maturity. It could safely be argued that in a repo with Bunds as collateral, you exchange one kind of cash against another kind of cash. Hence, economic risk exposures are limited. Even in the case of equity related SFTs, collateral is mainly out of leading index equity markets in which the underlying is extremely liquid.

One of the most prohibitive and notorious proposals in this regard was the Financial Transaction Tax (FTT), which would have extinguished SFT markets immediately. In its most simplistic version, the FTT would have sent costs for overnight government repos soaring over 200%. And though the regulation has been sidelined for now, other regulatory proposals work in a simlar vein.

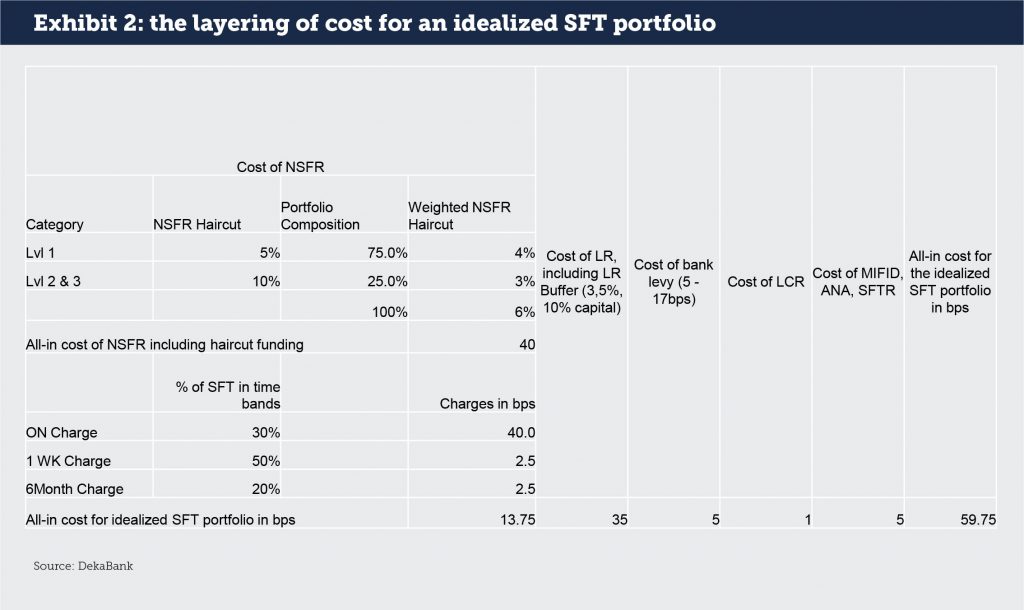

The Leverage Ratio (LR), for instance, does not discriminate between highly liquid and less liquid exposures. Basel regulators wanted to have a measure for gross exposures and immediately shied away from derivatives because after hedging, the net risk exposure is extremely small as compared to the notional amounts. SFTs are hedged instruments by nature, as cash and collateral are tied together at inception contractually, including daily margining and marking to market, so the same logic should apply. However, repos got caught up in the LR with their notional amounts. Assuming a leverage ratio of 3%, with an additional buffer of 0.5% to ensure that the leverage ratio is not breached, and a cost of capital of 10%, the additional charge for repo related balance sheet utilization comes in at 35 bps ([3% + 0.5%] x 10%). Regulators are quick to point out that the LR concept is not a specific repo related charge. However, after internal funds transfer pricing (also a regulatory requirement), costs will certainly be allocated to the repo desk and subtracted from the repo/collateral trading desk’s P&L.

The same holds true for the balance sheet charge, which is levied in Germany, among other countries. Banks pay into a stabilization fund to ensure that in case of a new banking crisis they will have to pay for potential restructurings themselves. The charge is linked to the size of the balance sheet of a bank at year end and is averaged out against the balance sheet size of all other participating banks to raise a fixed amount of money. It is difficult to put an exact number on the balance sheet levy, but it is safe to assume that the charge lies somewhere between 5-17 bps. This charge is – in line with the LR and FTT – completely ignorant about underlying risk exposures and hence, results in undue charges placed on short-term and low-risk exposures as compared to long-term and high-risk exposures.

And then there is the Net Stable Funding Ratio (NSFR), which is still a mystery in terms of exactly what implementation will look like, when or even if it will happen. Under the current specifications, an asymmetry in the treatment of assets and liabilities is envisaged. In other words: a repo matchbook would lead to a haircut application even in a totally balanced portfolio. The NSFR charges for a 1-week or 6-month SFT are 40 bps x 6% = 2.5 bps. [1] However, the regulatory zest for short-term transactions would translate into a 100% haircut for overnight SFTs with Level II and III collaterals and hence, cost 40 bps in the ultra-short-term of the curve.

In addition, there is the cost of the Liquidity Coverage Ratio (LCR), which does consider the short-term nature of SFTs and the quality of collateral. This means there is only a minor charge for 6-months SFT transactions, which is further mitigated by rules that ensure LCR funding requirement is not double-counted after the NSFR.

There is also the cost of MiFID II, originally planned to protect retail clients and now applicable to SFT markets, the introduction of the SFTR, ANA credit and many more. All these costs are fixed and independent of the size of the SFT book. They are assumed to add a further 2.5 to 5 bps. The all-in additional regulatory cost for an idealized collateral/SFT portfolio as outlined above would come in at around 60 bps (see Exhibit 2).

Inefficiencies in the regulatory landscape that lead to bad data, increased costs and general complexity

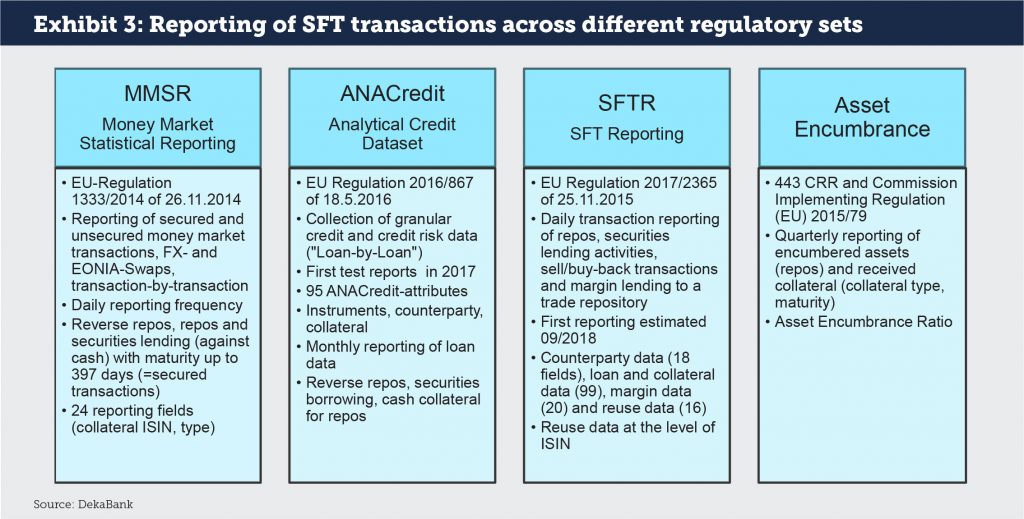

After the eruption of the financial crisis and continuing with the onset of the European government debt crisis, there were numerous regulatory departments and bodies in Europe coming up with proposals for the regulation of European SFT markets. It is probably safe to assume that by now there is some overlap and, correspondingly, some inefficiencies. This is particularly true with respect to the reporting of SFTs (see Exhibit 3).

As the table makes clear, there is now reporting of SFTs in the Money Market Statistical Reporting (MMSR), in ANACredit (ANA), in SFTR and as part of Asset Encumbrance, to name a few. Many of the reports are being consumed by different regulatory departments that do not speak to each other. They must be submitted in different time intervals, e.g. daily, monthly, quarterly, etc. Furthermore, they all differ with respect to the level of detail. While some of them cover most SFT types like the SFTR, others include just subsets like the MMSR or ANA. As each of the different receiving regulatory bodies is constantly refining its methodology and increasing the sophistication of its required data fields to suit specific and differing needs, reconciliation and comparison of the data is increasingly impossible. Put simply, the numbers do not add up. Moreover, all of the different regulators are talking to the same people in the banks who are producing these diverse data sets, which has led to a constant overload lacking in any additional value.

To use the data in a meaningful way, some of the statistics would have to be interpreted together, meaning the data should be pooled. If you want to understand liquidity mismatches in banks, you would have to pool the data from the SFTR with the data from the MMSR and from ANACredit. Judging legal or economic mismatches just from the data of the SFTR without considering money markets, and medium and long-term funding of a bank does not make a lot of sense. The same is true the other way around. The LCR as an example covers these aspects in a holistic fashion. However, calculating a relatively simple number like the LCR from the diverse data items and packages regulators receive would be a challenge, if not outright impossible – at least with respect to the data packages indicated above. And statistical reports like ANA should not demand their own set of SFT activity, but rather should refer to MMSR or SFTR.

It is worth reconsidering which data is meaningful to mine. Trying to measure “Collateral Chains” in a world where collateral is being moved in pools is probably not possible nor meaningful. Looking at some of the results from the Asset Encumbrance Ratio raises questions about exactly what kind of information is being produced, and how it should be interpreted.

A common-sense approach to balancing financial stability with transparency

While it is common sense that collateralization is good for systemic stability, regulators have made the utilization of collateral markets extremely expensive, sometimes with no additional stability or sustainability benefits. Quality collateral is scarce, and more collateral pools need to enter the market. At the same time, collateral velocity needs to be high to ensure efficient and smooth allocation. However, the huge cost associated with all kinds of regulatory actions in an already highly regulated market is making efficient collateral allocation more and more difficult, is discouraging new market participants from entering and preventing new collateral pools from being originated in an already dried-up market. By increasing fixed cost elements, regulatory action is promoting economies of scale to an extent that smaller counterparties are barred from entry because of the high fixed costs associated with using it. This is the opposite of what was intended as part of “too big to fail” initiatives.

Regulators should embrace SFTs as a tool to ensure that collateralized markets can function efficiently. While transparency and regulation is important, it is equally imperative to strike a balance between a market that is transparent and promotes financial stability with a market that works efficiently with no undue cost of utilization. Against this background, it may be argued that:

- Government bond SFTs, for which the collateral fulfils some minimum standards, should be out of scope for Leverage Ratio or balance sheet levy purposes, or be treated similarly like derivatives in the case of the leverage ratio.

- The regulatory benchmark for managing liquidity in the short-term end (up to one month) is the LCR. Applying additional haircuts for ultra-short term products in the NSFR leads to double charging and does not make much sense if one agrees that the LCR is the benchmark for a relatively simple, yet efficient regulatory measure. Correspondingly, the NSFR should only cover exposures starting after one or three months. From a competitive standpoint with the US, it is arguable that the NSFR should be delayed indefinitely anyhow.

- There should be no asymmetries between assets and liabilities in the NSFR calculation but proper and strict application of maturities and liquidity as exemplified in the LCR.

- Instead of reporting SFTs in multiple, different reports to various regulators, there should be one golden source that could be used by all regulators. SFTR could be this golden source, from where ANA, MMSR and other reports could retrieve data.

- Only the administrators of the golden source would establish contacts to banks when they change data inputs to keep the process as simple and efficient as possible.

- Once it has become clear that certain data is not needed, reporting of this data should be stopped: measuring collateral chains does not make sense in a market based on collateral pools. Also, Asset Encumbrance Ratios could be revisited to evaluate the value of what they measure.

- Data should be mined in a way that regulators would be able to model important regulatory measures like the LCR out of the data they receive, which does not seem to be the case at the moment. Otherwise, if regulators are not even able to populate simple regulatory measures like the LCR with the data heap they mine, then why originate these data in the first place?

These common sense measures would in no way reduce financial market stability, but they would go a long way to make markets more efficient and ensure that the overall goal of a collateralized market infrastructure that promotes financial stability and sustainability could be achieved at an economically justifiable cost.

[1] Based on calculations using the portfolio structure in Figure 1: The 40 bps assume that a matched repo book is fully funded and, consequently, all NSFR induced haircut funding would create surplus liquidity on the balance sheet of the bank, which would be deposited with the ECB at the ECB depo rate. We assume that NSFR induced unsecured funding would be raised as two-year funding. Furthermore, all Level II and Level III collaterals (25% of each maturity bucket) will have to be funded according to the NSFR haircuts. We apply 5% for Level I and 10% for Level II and III collaterals.

Michael Cyrus is Head of Collateral Trading at DekaBank, including Fixed Income Repo, Securities Lending, Equity Finance, Structured Collateralised Solutions and FX. Prior to this current role, he was head of Short Term Products at Deka. He joined DekaBank from RBS London, where he was global Co-Head of Short Term Markets and Financing responsible for Repo, collateralised Funding, FX and Interest Rate Prime and ETD. Before RBS, Michael was Head of Credit Financing and Collateral Trading (CFCT) at Dresdner Bank in London focusing on Emerging Market Repo, Equity Finance, Tri-Party Repo and synthetic financing in fixed income and credit markets. He started his career at Dresdner Bank in Frankfurt. Michael has a wealth of experience in the short term money-, repo- and securities lending and financing markets as well as in treasury operations. He holds a degree in economics from the University of Hamburg.